As usual, if it's CPI day it's also earnings day. Both weekly and hourly earnings for blue-collar workers were up at an annual rate of 4.7% from June to May. With headline inflation running at 2.2%, this means that worker pay went up about 2.5% in real terms. Not too bad.

Hourly wages for all workers were up only 4.4%, or 2.2% in real terms. However, the number of hours worked ticked up a bit, so the increase in weekly wages was 8.1%, or 5.8% in real terms. That's good news for workers, who are getting a bit more work than before, and probably not a problem for the Fed since the increase is mostly due to longer hours worked, not underlying pay rises.

As usual, it's worth noting that real weekly earnings have gone up a grand total of 0.99% since the beginning of 2020. It's a mystery why the Fed is apparently so worried about spiraling pay worming its way into inflation.

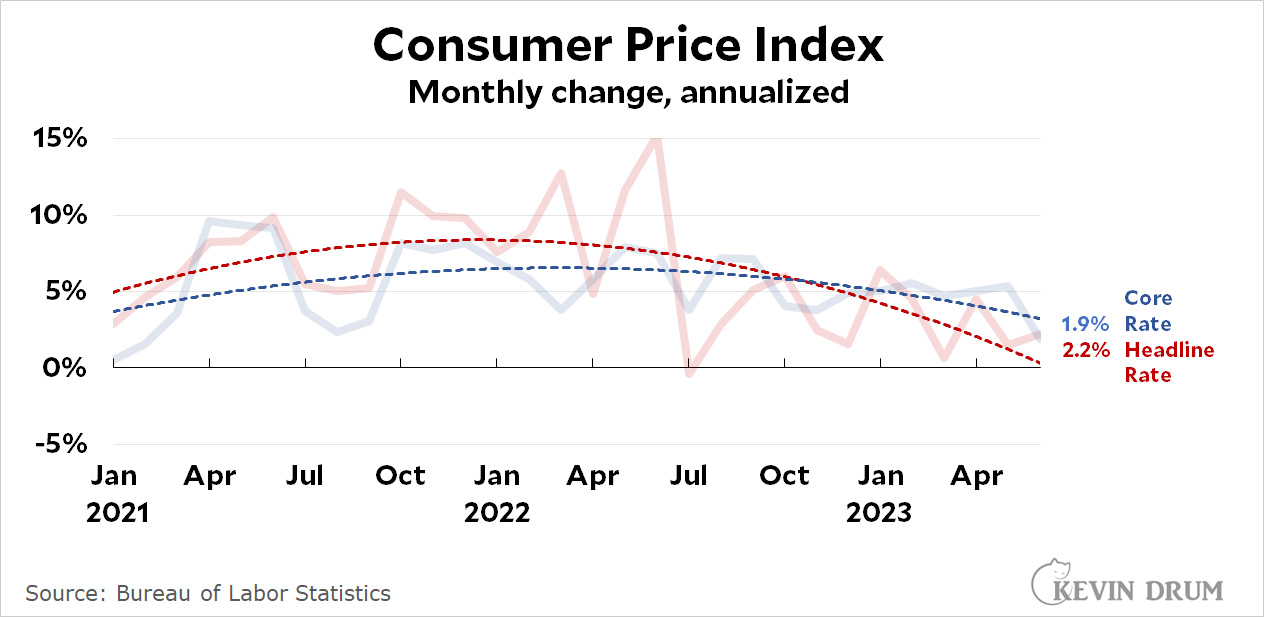

The CPI report for June was released this morning and it's nothing but good news.

Headline inflation is at 2.2% and dropping, while core inflation finally cracked and is now down to 1.9%. Inflation is literally running at the rate the Fed wants it to.

If you insist on wanting to know the conventional year-over-year figures, they were 3.1% for headine CPI and 4.9% for core CPI. But all this does is incorporate high inflation from the second half of last year into this year's lower figures, so why would you do that?

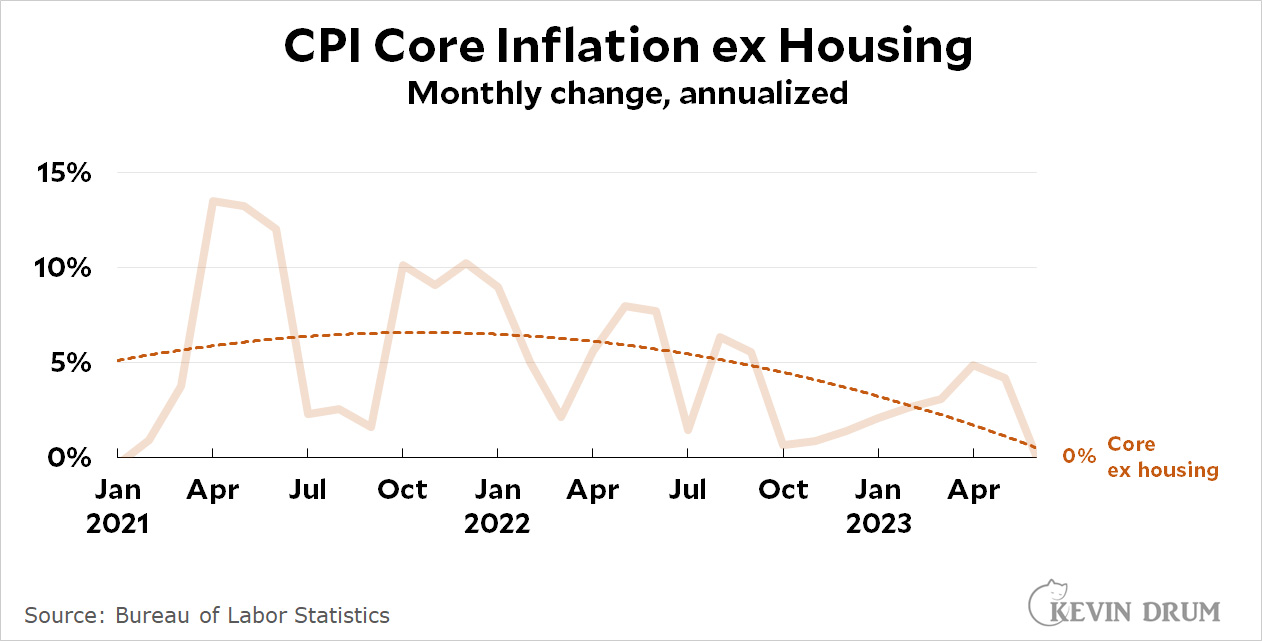

In other news, as foreshadowed last night, if you remove shelter from core inflation then CPI is literally zero:

Inflation news is spectacular this month. We just needed a little patience, that's all.

Over at the Wall Street Journal, James Mackintosh gets some surprising front-page treatment for a dovish take on inflation:

If core inflation came in just below 3%, the Federal Reserve would breathe a huge sigh of relief....It isn’t merely a dream: Measure U.S. price changes the way Europe does, and inflation was already there in May.

....U.S. core inflation—which excludes volatile food and energy—measured using the standard consumer-price index was 2.3 percentage points higher than the European-style inflation, known as the harmonized index of consumer prices. It is the biggest gap there has ever been.

It's actually much more dramatic than that. Mackintosh is using conventional year-over-year figures, which aren't very useful when inflation is changing quickly—as it is now. If, instead, you measure monthly inflation to get a better sense of where things are right now, then core HICP is an astonishing 5.1% lower than core CPI:

Why is US inflation so much lower if you calculate it the European way?

The main reason is that Europe’s measure, known as HICP, doesn’t include the imaginary cost of what a homeowner would pay to rent their house....Exclude something that no one actually pays, and which is calculated from guesses by homeowners of the rental value of their house, and core inflation’s looking basically fine.

The BLS will have new inflation figures for us Wednesday morning, although I don't know how quickly their HICP estimate gets updated. Stay tuned.

Philip Tetlock's Forecasting Research Institute conducted an exercise last year on the topic of human extinction events. Why? Who knows. Their report was released yesterday and, long story short, a group of various experts predicted a roughly 10-20% chance of catastrophe by 2100 (10% of human race dies) and a 1-6% chance of total extinction (fewer than 5,000 humans left). This is the total sum of the risk from five possible scenarios:

Artificial intelligence

Nuclear

Engineered virus

Natural virus

Meteor, sun going nova, etc.

Let me say from the start that I think this is kind of nuts. I'd personally put the overall risk of extinction from everything combined at about 0.1% or so. But that's just me. I'm an eternal optimist, I guess.

The proximate motivation for the study, of course, was the recent surge of interest in the possibility of some future AI going nuts and killing everyone. AI experts overall predicted a 13% chance of AIs causing an extinction level event, and I found this breakdown instructive:

Apparently there's a group of AI experts who are absolutely obsessed with extinction and have spent more than 1,000 hours thinking about it. These people seem to have thought themselves into a frenzy and they're obviously driving up the average a lot. The median extinction forecast, which eliminates the influence of the extreme outliers, is only 3%. Still too high, I think, but not completely crazy.

Unlike some things, this is not a case where thinking harder does you any good. There's really no concrete evidence one way or the other about the chances of AI-caused extinction, just speculation, and going down an extinction rabbit hole is little more than a fast path to the booby hatch. Just keep in mind that any possible super-threat—AI or otherwise—will almost certainly be met by a countervailing super-defense. COVID-19 was a dangerous pathogen, but advancing technology allowed us to create a vaccine in record time. Nuclear weapons are being met with missile defense systems. Climate change is being met by renewables and, maybe someday, geoengineering. AIs will be met by other AIs. So chill.

Four troopers had collectively entered at least 636 fake tickets into the state police computer system over a nine-month stretch to make it appear they were more productive than they actually were. The troopers, who worked for Troop E based in Montville, did so for their own personal benefit — to curry favor and perks from supervisors, internal investigators concluded.

Huh. But it gets weirder. A recent audit discovered that upwards of a quarter of the the entire Connecticut state police had been doing the same thing over the past decade. But why? Surely not for personal perks if they were all doing it. The answer, it turns out, is that police in Connecticut are required to report every traffic stop they make to the Connecticut Racial Profiling Prohibition Project, a state-funded group that analyzes police citations to determine racial profiling trends:

The project, which is contracted by the state to analyze the records, including race, ethnicity, gender, age and other demographic information about drivers stopped, to identify patterns of potential racial profiling by officers.

....The audit found with “a high degree of confidence” troopers submitted at least 25,966 tickets to the racial profiling database that did not match records in the judicial database between 2014 and 2021.

....Overreported records were more likely to be reported as white drivers and less likely to be reported as Black or Hispanic drivers, the auditors found.

There had been patterns reported previously that state police were more likely to stop Hispanic motorists during daylight hours and more likely to search drivers of color. Troopers probably found these allegations annoying and wanted investigators to get off their back, so—apparently—they cooked up a scheme to issue fake tickets that had the overall effect of boosting the number of white drivers in the database. This made it look less likely that troopers were engaged in racial profiling. The whole thing went on for years and involved nearly a thousand state police.

Or maybe it was all just a big mistake. Governor Ned Lamont urged caution:

“I wouldn't jump to conclusions,” said Lamont, who became governor in 2019, a few months after state police found four troopers had been fabricating tickets. "There's no indication that was purposeful. A lot of it may have been inadvertent. We've got to look into that.”

The City Council voted in October 2021 to study the viability of forming a city-owned bank and to create a business plan for doing so. With new political leadership and support from a number of community organizations, the city is now preparing to devote $460,000 toward the study’s first phase.

A public bank’s decisions would be driven by the needs of Los Angeles communities rather than private shareholders, advocates say, leading to investments in projects and people normally disregarded by Wall Street.

This is not like postal banking, where ordinary people can keep small savings accounts and make small loans. This is a commercial bank that would fund worthy projects that big corporate banks won't touch.

And it sure sounds like a bad idea to me. If the City Council wants to hand out money based on politics instead of creditworthiness, well, they already do that. It's their whole job. Who needs a bank for that?

The only thing that comes to mind is that they think it will stretch their spending capacity. Instead of giving $1 million to an affordable housing project, they can capitalize a bank for $1 million and then loan out $10 million. Hooray! In addition, of course, the city-owned bank can, if it wishes, make riskier construction loans than private banks; perform faster underwriting; aid in faster land acquisition; and just generally charge everyone less than a Wall Street Bank would.

But is that wise? Are commercial banks really ripping off Los Angeles? Or are they being normally prudent in their decisions? If they are, LA would be ill-advised to be less prudent.

There are limited occasions when markets are distorted enough that government funding is a better bet. Health care is an example. So is highway building. But I'm not so sure about banks. At most we might want to increase lending by providing loan guarantees, and even that's questionable unless the city is awfully sure their credit judgment is better than JP Morgan's. Beyond that, there are lots of banks and lots of competition in the private sector. We should probably leave the banking to them.

In hindsight, a lot of people overestimate how many schools were closed during the pandemic. In reality, about half were fully open for the 2020-21 school year and upwards of 90% for the 2021-22 school year. And yet, the evidence so far suggests that kids fell behind considerably anyway and haven't made up any ground this year.

I'm not familiar with NWEA, but they take a fresh crack at this topic using the results of the MAP Growth reading and math test given to 6.7 million students. Here's the basic result:

Elementary school students are about 2-3 months behind their pre-COVID selves, while middle-school kids are more like 4-6 months behind. What's even worse is that in the current school year they appear to be falling even further behind:

The authors are pessimistic:

Addressing these gaps will take sizable and sustained effort....While many districts are offering academic programs this summer, these programs are typically offered to a small share of students and do not include enough additional instruction to catch up the average student....As such, it will be next to impossible for districts to build in the additional schooling time necessary to allow for student recovery before the expiration of ESSER funds next year

Research suggests that high-dosage tutoring — which pairs a trained tutor with one to four students, at least three times a week, for a full year — can produce gains equivalent to about four months of learning. But it is expensive and difficult to scale. A federal survey in December found that just 37 percent of public schools reported offering such tutoring.

I really seem to have guessed wrong about this. I believed, basically, that kids are resilient and would make up any lost learning in pretty short time. That may still happen, but it sure hasn't happened yet. The NWEA research is consistent with the most recent NAEP test scores, which make it clear that students have sustained substantial and persistent declines in learning thanks to COVID.

The Biden administration said it intends to move forward with the long-promised sale of F-16 jet fighters to Turkey, hours after that country’s president withdrew his objections to extending membership of the North Atlantic Treaty Organization to Sweden.

National-security adviser Jake Sullivan rejected suggestions that advancing the sale to Ankara was directly linked to President Recep Tayyip Erdogan’s decision to let Stockholm into the alliance, saying there was no such quid quo pro.

Translation from diplo-speak: We could hold out as long as those bastards could. It's been planes for Sweden all along, and they bloody well knew it.

Alternative: Turkey never really cared about barring Sweden from NATO. It was just performative bullshit for the home crowd. And the US never cared about the F-16s. It's just an ancient design for the export market anyway. So Blinken and Erdogen finally got together, breathed a collective "Meh," and that was that.

I've noticed lately an odd mythology building up about how scientists were all wet about the COVID vaccine stopping transmission of the virus. There's an element of truth to this, but it's far from the whole story:

What's true is that although the vaccine was effective against transmission early on, that's not the case with the Delta and Omicron variants. Today, if you get COVID even after being vaccinated, you can still shed the virus and infect others. The odds of transmission are lower, but not by a lot.

However, the vaccine does have a protective effect. If you've had the standard 2-dose series of one of the mRNA vaccines, it cuts down your chances of getting the virus by upwards of 30-50% (though the effect wanes over time). This is why, after vaccination rates got high enough, we started to see a sustained drop in population test positivity: .

So: although it's technically true that the COVID vaccine has only a very modest effect on transmission, in practice it does a great deal to slow the spread of the virus.

I don't want to overstate things. The primary effect of the vaccine is still the same: it strongly reduces the odds of getting a serious case of COVID, and with it, long COVID. However, it also does a reasonable job of protecting against infection entirely, which obviously lowers the overall transmission rate of the virus.

The bad news about the COVID vaccine is less that it's ineffective and more that its effectiveness wanes considerably over time. If we want to keep COVID at bay, it's pretty clear that boosters are going to have to become an annual event, just like the flu shot.

As usual, it's worth noting that real weekly earnings have gone up a grand total of 0.99% since the beginning of 2020. It's a mystery why the Fed is apparently so worried about spiraling pay worming its way into inflation.

As usual, it's worth noting that real weekly earnings have gone up a grand total of 0.99% since the beginning of 2020. It's a mystery why the Fed is apparently so worried about spiraling pay worming its way into inflation.