Sunset behind a rock formation at Joshua Tree National Park.

Cats, charts, and politics

Sunset behind a rock formation at Joshua Tree National Park.

According to the Census Bureau, the average household income of the poorest quintile is roughly $23,000.

According to the Congressional Budget Office, that increases to $49,000 after you account for taxes and government benefits. This compares to about $80,000 for the average middle-class household.

![]()

Along with CPI, we also got September readings for real wages today. Hourly wages were up slightly, but because hours worked dropped there was a fall in weekly wages:

All employees in September (adjusted for inflation)

Blue-collar workers in September (adjusted for inflation)

A quick note on inflation: my favorite measure happens to be quarterly CPI, which smooths out a bit of the monthly volatility but still provides a more current measure than the usual year-over-year reading. The downside, of course, is that you only get a quarterly update every three months—although there are times when I think we'd all be better off with this less frenetic frequency.

In any case, three months have gone by and we now have CPI for Q3 of 2024:

It doesn't get much better than that, does it?

It doesn't get much better than that, does it?

CPI inflation fell slightly in September to 2.2%:

Core CPI increased a bit to 3.8%. On a year-over-year basis, CPI came in at 2.4% and core CPI at 3.3%.

Core CPI increased a bit to 3.8%. On a year-over-year basis, CPI came in at 2.4% and core CPI at 3.3%.

Back in the day—i.e., 2022—crypto in politics was all about Sam Bankman-Fried, who lavished his millions on politicians under the guise of altruistic giving. It was a lie, of course, but everyone pretended to accept it for a while.

Bankman-Fried is warming a prison cell these days and the crypto industry has moved on. Alexander Sammon explains:

This time, there’s no grand political theorizing. No time to waste on utopian futures or societal aspirations. In fact, Coinbase’s billionaire CEO Brian Armstrong, the closest thing to a leader of this political formation, has openly declared that the United States is a society in “decline” and that “backup” options for existing nation states must be pursued. No, the 2024 crypto money machine has been reborn out of a cold, hard determination to do one thing and one thing only: put politicians in power who will stay out of crypto’s way.

And the crypto money machine is huge beyond imagining. Here's an estimate of corporate political contributions by sector for 2024:

Crypto is massively outspending everyone else combined, and this money is being wielded for one specific purpose: to gain passage of a bill that would only lightly regulate crypto. And it is being wielded ruthlessly:

Crypto is massively outspending everyone else combined, and this money is being wielded for one specific purpose: to gain passage of a bill that would only lightly regulate crypto. And it is being wielded ruthlessly:

Ohio Democratic Sen. Sherrod Brown, who has advocated for stricter regulation of the crypto industry in the past, is firmly in the lobby’s crosshairs. The group is spending an astronomical $40 million to oppose Brown, the chair of the Senate Banking committee.... That wild spending makes his victory look much more difficult. (“Money moves the needle,” Armstrong told Axios. “For better or worse, that’s how our system works.”)

Now, there's a lot more to the political world than direct corporate contributions. In fact, it's a fairly small share of the billions of dollars in total political spending this cycle. Nevertheless, this is a very impressive figure for an industry that contributed approximate zero in 2022. They want to be left alone to continue scamming the American public, and they're willing to spend eye-watering amounts to insure that.

So if you're wondering why practically everybody is either friendly or at least not hostile to crypto these days, this is it. They're facing too big a war chest to risk saying anything directly about regulating crypto. The $40 million flame thrower aimed at Sherrod Brown is all the warning they need.

Apparently the latest hotness is to air minor differences with people you normally agree with. I'm in! Noah Smith argues today that our current economy is the best in a very long time, and overall I think he's right. But there's one thing I think he's wrong about: wage growth.

Unfortunately, it's been pretty lousy over the past three years:

This is wage growth for nonsupervisory workers, but it doesn't really matter. Every measure of wages shows roughly the same thing.

This is wage growth for nonsupervisory workers, but it doesn't really matter. Every measure of wages shows roughly the same thing.

This is all bound up with inflation. Wages have kept up with inflation over the past three years, so there's been no drop in living standards. But there's been virtually no gain, either. This kind of sluggish real wage growth is great for the Fed, since it means there's little chance of a persistent wage-price spiral, but not so good for workers, who are just treading water.

Now, some of this is a bit of an artifact, since a three-year span includes the big drop of early 2022 but not the corresponding big spike of early 2020. Still, even accounting for that doesn't change things much. There just hasn't been a lot of wage growth lately, and that's probably one factor in the overall sour feelings about the economy.¹

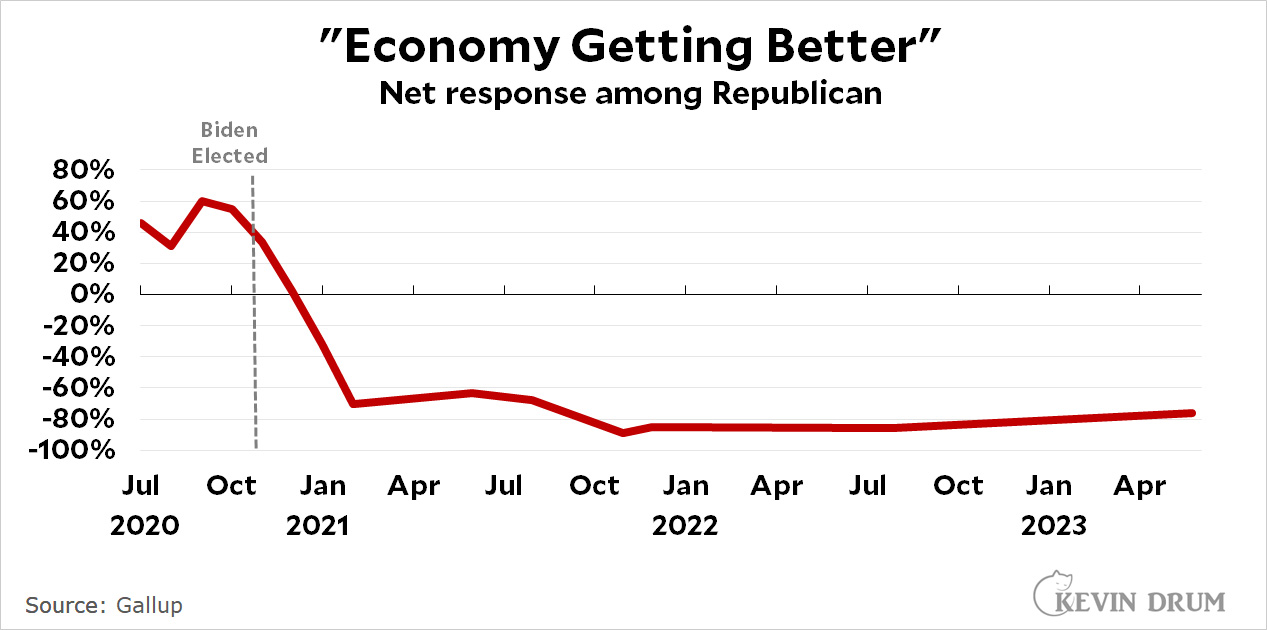

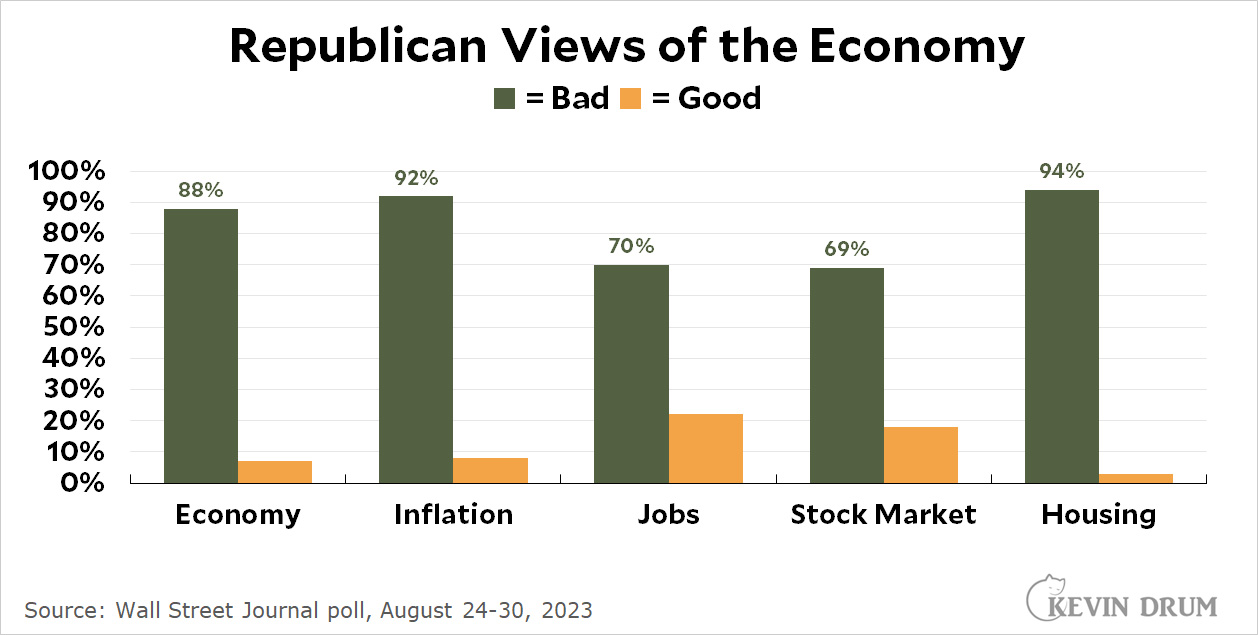

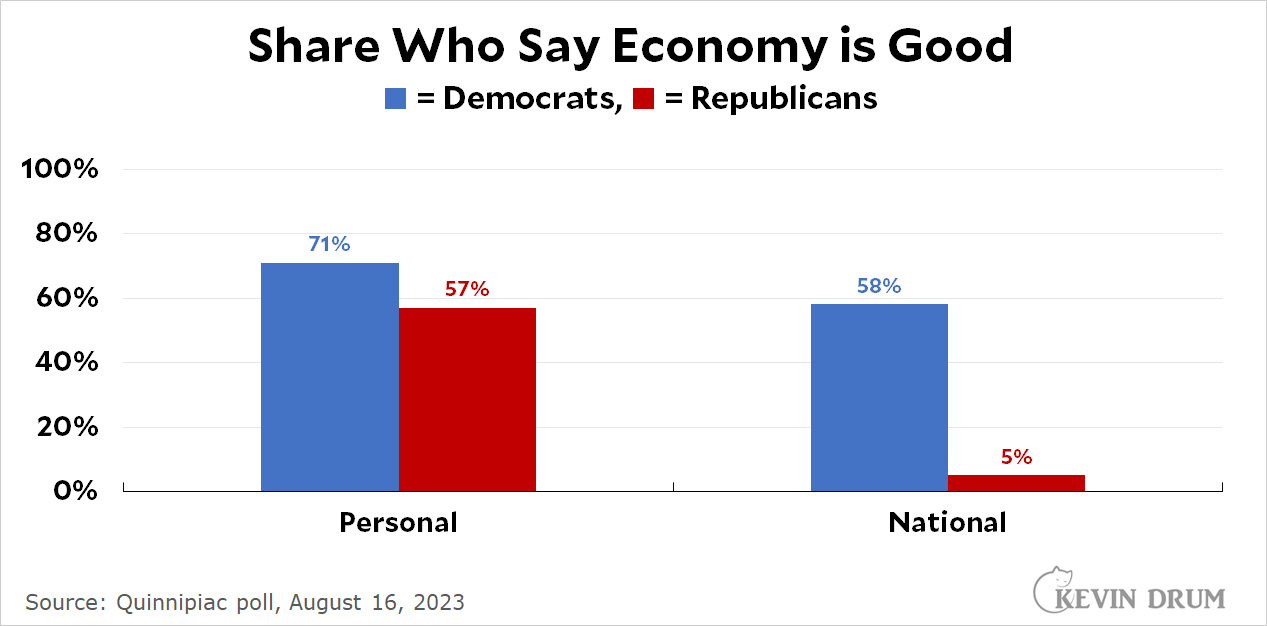

¹But not a big factor. As I've pointed out repeatedly, this is mostly a purely partisan effect: only Republicans think the economy is horrible, a view that took hold at nearly the instant Joe Biden won the election. Since then, both Fox News and Donald Trump have hammered away at this, and Republicans believe them.

This is a late afternoon view from Angeles Crest Highway up near Mt. Wilson.

In a new report, the International Energy Agency predicts that renewable electricity will grow considerably by 2030 but won't hit its goal of tripling worldwide. Among large users, only China and India are forecast to triple:

Virtually all of this growth is in solar, with about a quarter in wind. Everything else is a rounding error.

Virtually all of this growth is in solar, with about a quarter in wind. Everything else is a rounding error.

POSTSCRIPT: It's worth noting that the IEA is notoriously conservative in its forecasts, revising them upward nearly every year. So there's actually a pretty good chance that their projections are wrong and renewable electricity will meet its 3x growth goal.

The YouGov weekly tracking poll stubbornly sticks with a 3-point Harris lead this week:

Donald Trump is exactly where he was in July with 44% of the vote. It seems like this is pretty much his ceiling. But the undecided/other vote is still around 8%. Harris has made a bit of progress over the past couple of months but hasn't sealed the deal.

Donald Trump is exactly where he was in July with 44% of the vote. It seems like this is pretty much his ceiling. But the undecided/other vote is still around 8%. Harris has made a bit of progress over the past couple of months but hasn't sealed the deal.