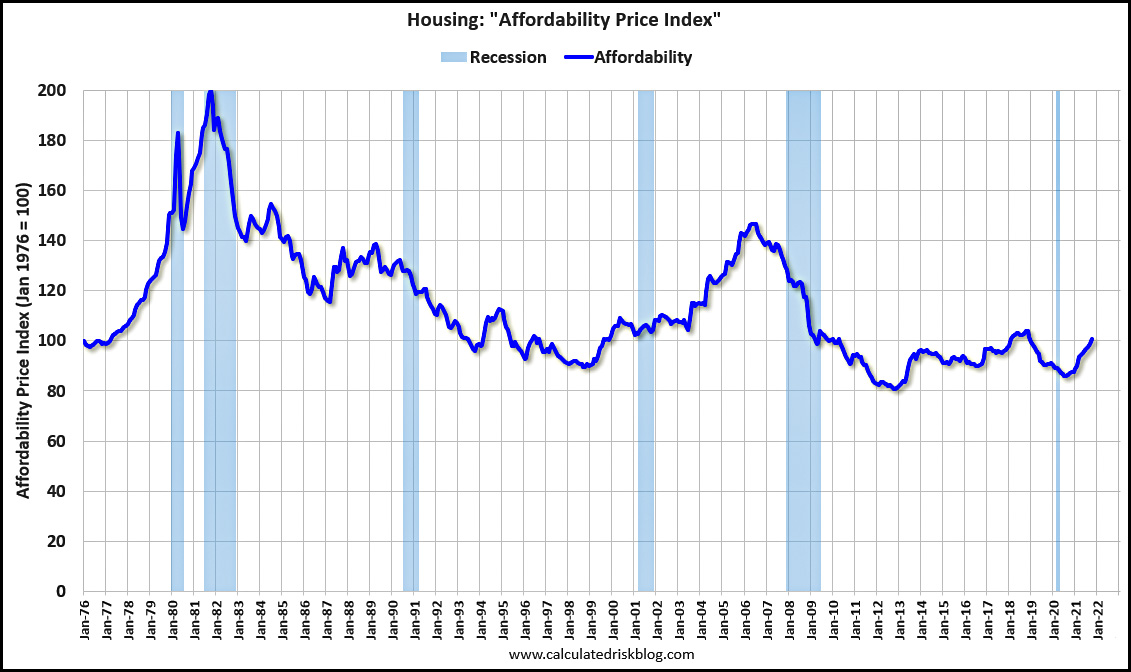

Are we in a new housing bubble? I'm generally a fan of ignoring the noise and instead looking at some of the simplest fundamentals, like the price-to-rent ratio and the basic affordability of housing. Right now the price-to-rent ratio is going up, but that may be an artifact of artificially low rents thanks to the pandemic. Even more fundamental is whether housing is eating up a bigger and bigger share of income, and according to the affordability index maintained by Calculated Risk it's not:

In 2006, housing was genuinely getting unaffordable, which explains the explosion of subprime and other dodgy products intended to make homes look cheaper to buyers who couldn't really afford them. Today, however, we see none of that. Looking at the actual cost of buying a house (which takes into account price, interest rates, etc.) nothing is happening at all. Housing affordability improved for a few years starting in 2018 and has now recovered to its usual level of the past decade.

In 2006, housing was genuinely getting unaffordable, which explains the explosion of subprime and other dodgy products intended to make homes look cheaper to buyers who couldn't really afford them. Today, however, we see none of that. Looking at the actual cost of buying a house (which takes into account price, interest rates, etc.) nothing is happening at all. Housing affordability improved for a few years starting in 2018 and has now recovered to its usual level of the past decade.

How accurate is this? I can't say for sure, but it seems pretty reasonable. Of course, if interest rates go up—and they will—houses will become less affordable and the home buying frenzy will probably dry up.

It's always tricky looking at national-level statistics on housing because there's such huge differences between areas. High demand metro areas could have rising housing prices, but it's swamped by limited to no price growth across large parts of the country.

I think everyone is aware that housing in some metros is much more expensive than others. But a national housing bubble—one that is capable of causing problems for the economy of the whole country—should show up in the numbers. And as Kevin points out, that doesn't appear to be the case (yet). So, it sure must suck being a renter in the Bay Area or SoCal, but their struggles aren't likely to cause a recession, given the limited number of households affected. (The country's handful of priciest housing regions—SoCal+SF Bay+Portland+Seattle+Hawaii+Boston+NYC+DC+Miami—are home to about a quarter of the country's population, and probably about 1/3rd of household spending power).

Although he has been warning of an imminent collapse of the US stock market for some time now (for which he has been widely derided as the indexes continue to climb ever higher), Jeremy Grantham is now doubling down, claiming the US is in a seldom-occurring superbubble that he calls a "3-sigma equity bubble." In addition to overpriced equities, bonds, and commodities, he claims the housing market is at an all-time high multiple of personal income. I have no idea why this claim is so at odds with the Affordability Price Index shown above (which seems like it would have to be somewhat correlated to Grantham's evaluatory standard), but he is clearly a smart guy and has been right about quite a number of these things in the past. Here is his analysis of the current economic situation:

https://www.gmo.com/europe/research-library/let-the-wild-rumpus-begin/

Things are bubbly--but maybe not has bad as he thinks.

The high end real estate market has been crazy....for...well....ever as far as I am concerned. Regular market--spotty and local. When London and Miami hit hard times--then that means the high end real estate market has dried up. That will hit some hard--but banks should be able to withstand it, unlike last time there was a problem in the real estate market. Grantham is looking at housing as sales price/income; affordability is monthly payments. The latter will change with interest rates, but is fine for now.

The stock market P/E has been high since Obama times then tax breaks for the wealthy really doesn't help the economy much--but that money has to go somewhere...--The P/E really shot up with stimulus packages/pandemic slow down. Looks like stocks need to drop another 10% to bring P/E ratios into high end of "normal" range--or there could be a 10% jump in earnings.

Commodities? Bubbly--but also still sorting itself out from pandemic swings. And now--the great Corned Beef shortage!!!

Bonds--I got nothing.

Grantham is looking at housing as sales price/income; affordability is monthly payments. The latter will change with interest rates, but is fine for now.

Most households in the US will be protected by their fixed rate mortgages. Of course, if borrowing costs rise enough, prices will have to come down. And so a lot of Americans will feel poorer. And that will affect their spending. On the other hand property prices will come down, which before long will compensate for the higher rates, thereby making real estate look more like a (relative) bargain. And the cycle begins anew.

To me the big question isn't so much economic but political: does the coming tightening translate into a soft landing (with maybe even a pickup in growth in 2024), or does a recession arrive and end Democrats' control of the executive branch?

I guess it sounds scarier if you add 3-sigma on the front.

More on Affordability Indexes by CR; https://calculatedrisk.substack.com/p/housing-a-look-at-affordability-indexes

In the highest cost areas I suspect price : stock market ratio is important.