For some reason, this question has suddenly become the new hotness among economists. But why? Paul Krugman notes that bond yields were pretty steady for a while in late 2022 and early 2023:

Over the past few months, however, the bond market has, in effect, capitulated, sending the signal that investors expect rates to stay high for a long time. Long-term interest rates are now higher than they have been since the 2008 financial crisis.

Well sure, but this is hardly surprising since Fed rates are now at 5.33% compared to zero during most of the Great Recession. Plus there's this:

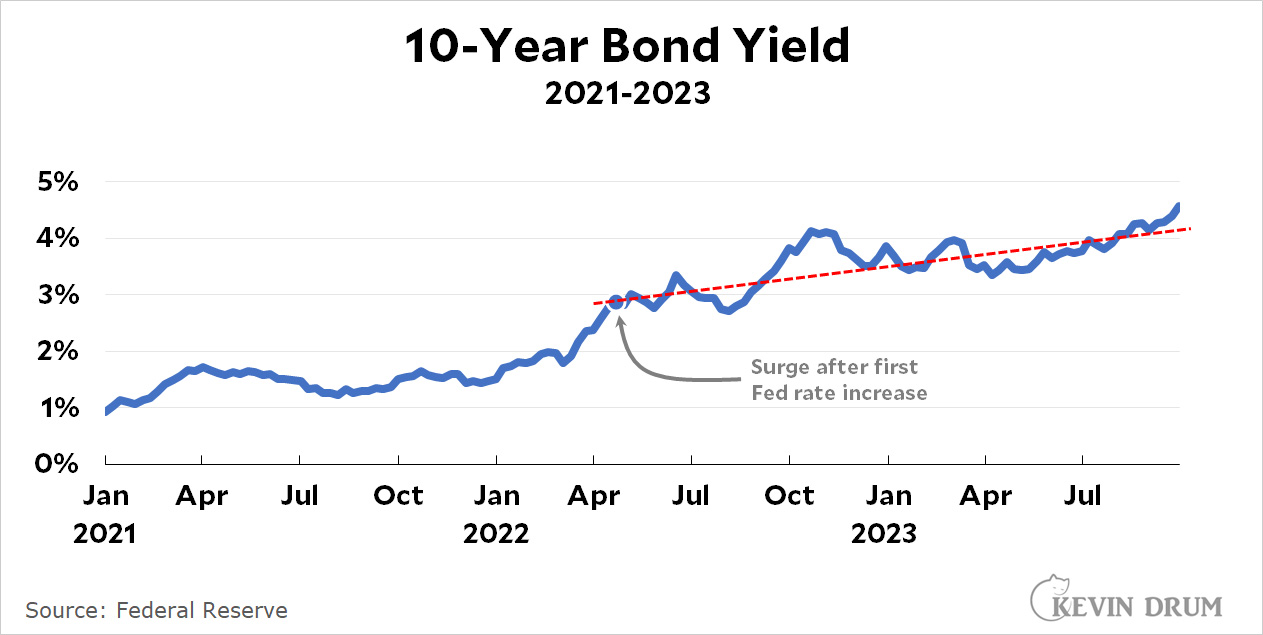

Long-term yields spiked right after the first Fed hike in March 2022. Since then they've increased at a pretty steady rate as the Fed has continued to hike short-term rates. 10-year yields are now above their trendline, but only barely and only for the past couple of weeks. This doesn't strike me as something to panic about. And there's this:

Long-term yields spiked right after the first Fed hike in March 2022. Since then they've increased at a pretty steady rate as the Fed has continued to hike short-term rates. 10-year yields are now above their trendline, but only barely and only for the past couple of weeks. This doesn't strike me as something to panic about. And there's this:

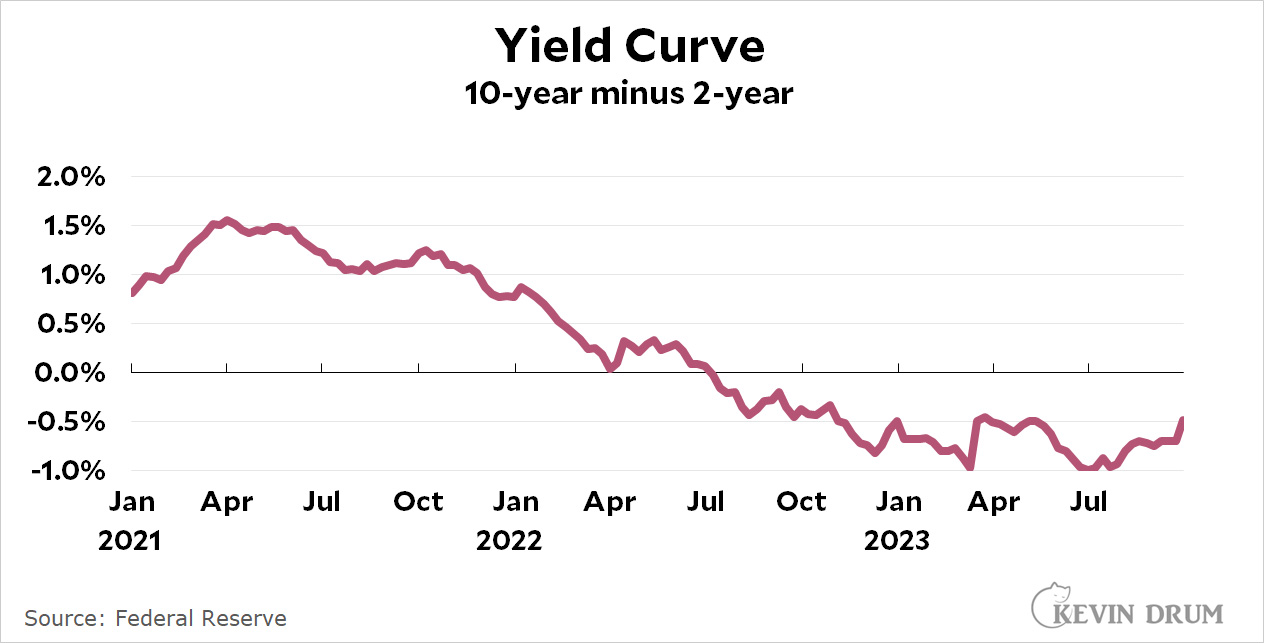

The yield curve remains inverted, a sign that bond markets still expect a recession that will lower interest rates. It's true that the yield curve isn't quite as inverted as it used to be, but that doesn't mean much.

The yield curve remains inverted, a sign that bond markets still expect a recession that will lower interest rates. It's true that the yield curve isn't quite as inverted as it used to be, but that doesn't mean much.

Krugman says: "My instinct is to say that the bond market is overreacting to recent data and that high interest rates, like high inflation, will be transitory." I'd go further: I'm not sure the bond market is really telling us very much in the first place. But yes, to the extent that it is, it's overreacting.

Unlike Krugman, I don't have an economic argument to make for believing this—aside from the fact that I suspect a recession is on the horizon. Mainly, my argument is that everyone, everywhere, at all times overreacts to everything that's new, and this goes double for financial markets. Fed rates have been above 4% for—hold onto your hats!—ten whole months. That exhausts our patience and must mean it's time to give up and assume that rates will be high forever.

Spare me.

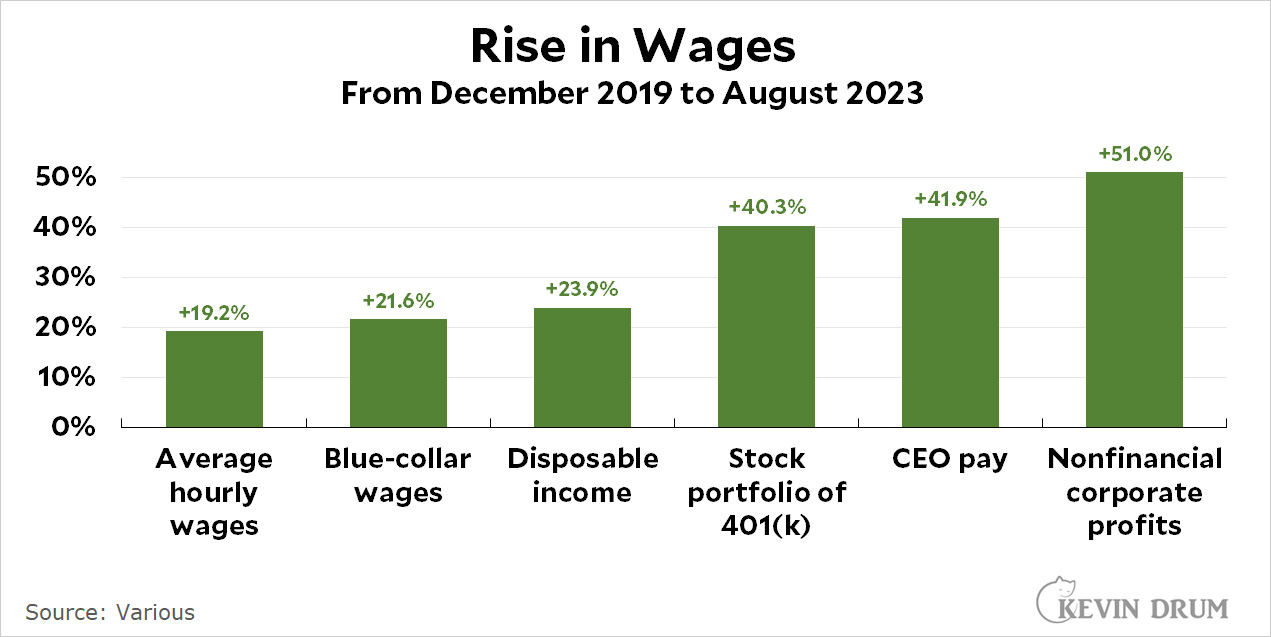

If you cherry pick and don't account for wage growth, you can make anything look terrible. In reality, overall prices have increased 18.4% since the end of 2019¹ while overall wages have increased 19-23%. That's no great shakes for American workers, but for most people the relative cost of things has barely changed at all over the past four years.

If you cherry pick and don't account for wage growth, you can make anything look terrible. In reality, overall prices have increased 18.4% since the end of 2019¹ while overall wages have increased 19-23%. That's no great shakes for American workers, but for most people the relative cost of things has barely changed at all over the past four years.