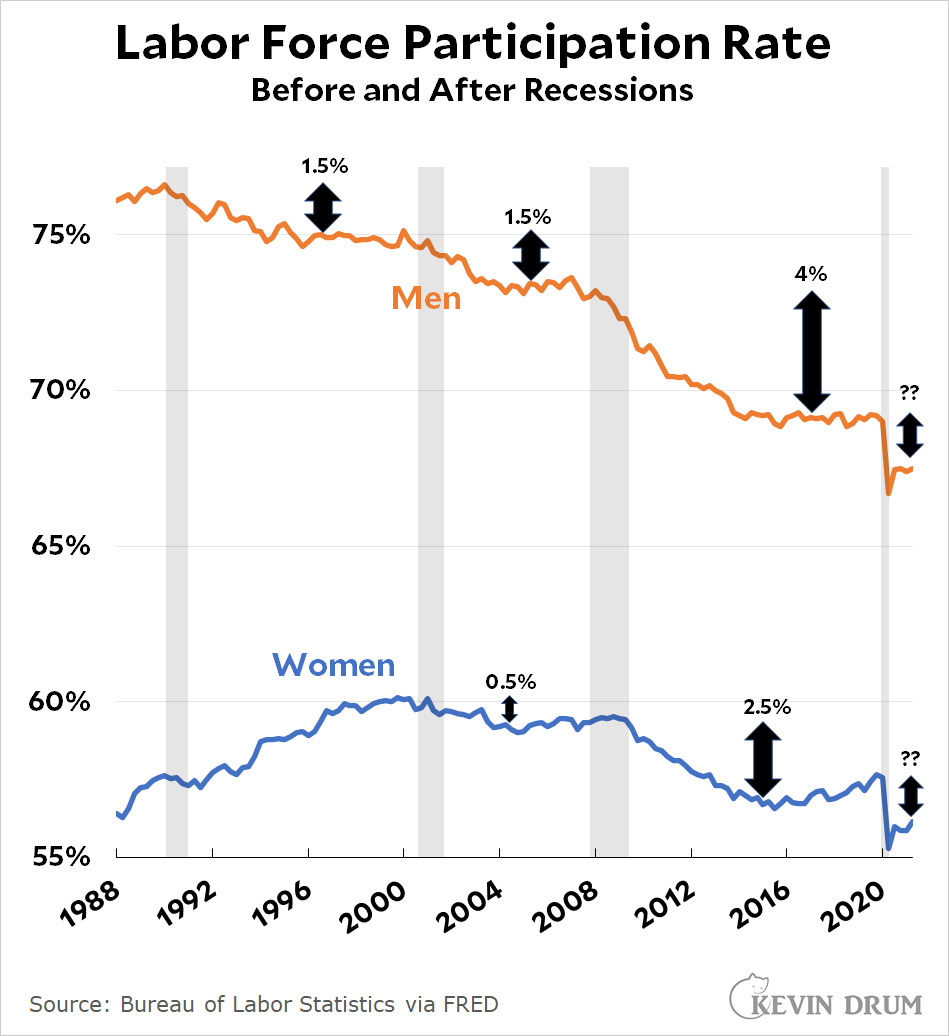

Behold this chart showing the Labor Force Participation Rate over the past few decades:

The LFPR is exactly what it sounds like: it's the percentage of the adult population that's either employed or looking for employment. Let's take a look at men first.

After the 1990 recession, the LFPR for men dropped by about 1.5 percentage points and then flattened out. After the 2000 recession, ditto. After the 2008 recession, the loss was about 4 percentage points. In other words, after every recession the LFPR ends up at a permanently lower level.

This has now happened often enough that we should expect something similar to happen this time around: the LFPR will end up dropping about one point or so and then flattening out at around 68%. This is only about 0.5 points above where we are right now, which equates to less than one million people.

Among women we see a similar thing, though it's smaller and didn't start until the 2000 recession. At a rough guess, we should expect the LFPR for women to end up about one point from where it is now, which equates to two million people.

Altogether, then, this makes it look like we'll add about 3 million workers before the LFPR flattens out again. Looking at the unemployment rate provides a similar number. This is a lot less than the 10 million people who are supposedly looking for jobs.

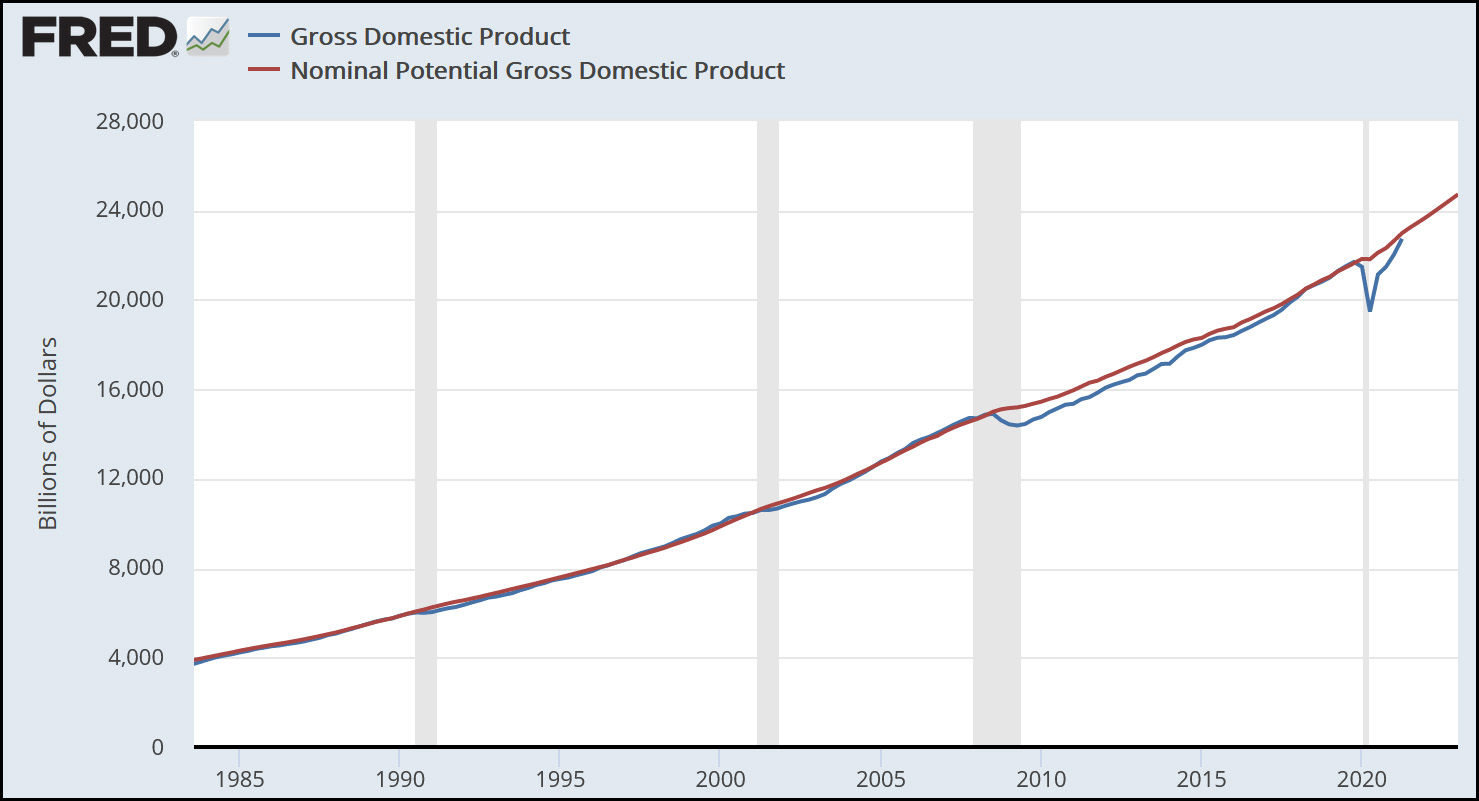

There are no sure things here, but numbers like these are why I continue to think there are fewer people looking for jobs than we think. I'd put it at 3-5 million, at which point the unemployment rate is 3-4% and the economy is operating at 100% of its potential:

Can we boost the LFPR? Yes indeed. We just have to pay people more to lure them into the job market. Can we raise potential GDP? Also yes, in theory, but that's a slower, more complicated process and no one is entirely sure if we can do it—or what risks it involves. It's currently a matter of some controversy.

I would love to be wrong about this, but I'm not sure I see any reason to think that the US economy is on track to suddenly explode above its potential. The fast and massive stimulus spending did its job, but its job was to speed up our recovery, not to raise the economy to a permanently higher level.¹ The good news is that it did this marvelously. The bad news is that having done it, there's not much more we can expect it to do.

¹Its other job, of course, was to help people who were hard hit by the recession. That's not germane to a macroeconomic discussion, but it's certainly why massive stimulus is worthwhile regardless of its broader effects.

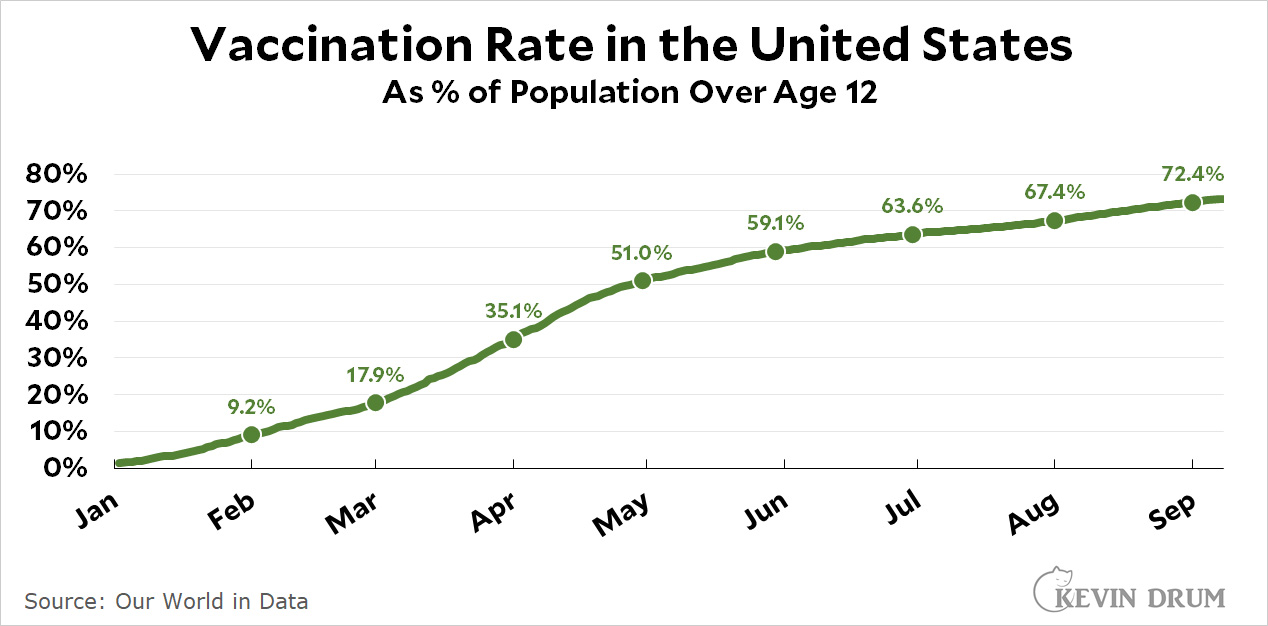

In any case, only about 27% of the adult population has yet to be vaccinated, and I'd guess that close to half of these people work for small companies and won't be affected by the mandate. So even if Biden wins in court, I figure this will get us up to maybe 85% or so. Not bad, but still not enough.

In any case, only about 27% of the adult population has yet to be vaccinated, and I'd guess that close to half of these people work for small companies and won't be affected by the mandate. So even if Biden wins in court, I figure this will get us up to maybe 85% or so. Not bad, but still not enough.