Paul Krugman says that signs are good for a soft landing even though the Fed has hiked short-term interest rates sharply and long-term rates have followed right along:

If you had told me two years ago that interest rates would soar like this, I would have predicted a nasty recession with spiking unemployment. But in fact job growth, and probably G.D.P. growth, have just kept chugging along.

The problem for economic analysts is that there are two possible reasons the recession dog hasn’t barked. One is that we’re seeing fundamental economic change — that new investment opportunities have increased r-star, so that the economy can handle high interest rates indefinitely. The other is that there are, as Milton Friedman claimed, “long and variable lags” in the effects of monetary policy, and high rates will eventually break something major.

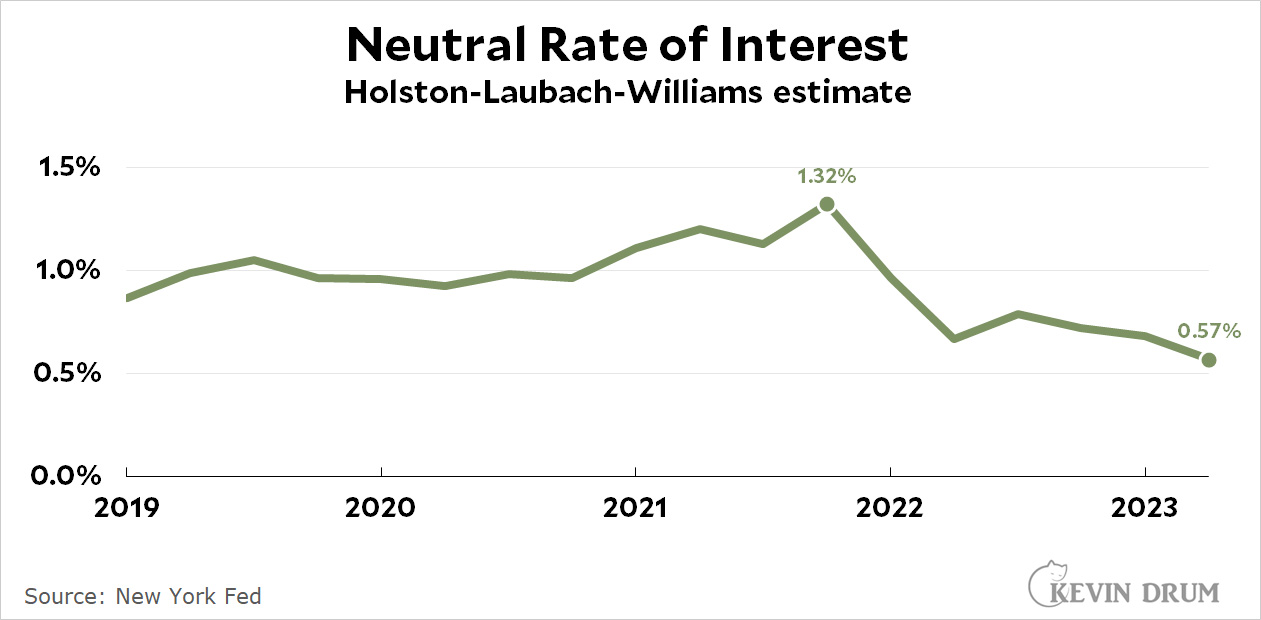

R-star is the "neutral" rate of interest, an estimate of what interest rates would be at full employment if the Fed left things alone. Here's an estimate of r-star over the past few years:

It sure doesn't look like r-star has gone up lately. The Fed is holding interest rates above 5% right now, which continues to look extremely contractionary. For now, count me as team long and variable lags. I hope to be wrong since a recession could easily hand the presidency to Donald Trump, but I suspect a recession is coming.

It sure doesn't look like r-star has gone up lately. The Fed is holding interest rates above 5% right now, which continues to look extremely contractionary. For now, count me as team long and variable lags. I hope to be wrong since a recession could easily hand the presidency to Donald Trump, but I suspect a recession is coming.

Isn't it that a lot of people no longer think China looks like such a good investment, and that Europe is stuck with Russia?

R* is a derived estimative figure that in financial economics none of us feel is particularly robust. But faute de mieux....

The NY Fed estimative derivation if some fundamental underlying change is emerging does not robustly you tell that it hasn't changed (thus Krugman's writing).

I was thinking about buying a new car in August, but even small loans were running over 6%… so I didn’t buy a new car.

The recession is now Justins fault.

You'll have to tell how R* is calculated. I think it is a meaningless concept (since the idea of "what interest rates would be if the Fed did nothing" is in the modern world to me complete nonsense - what is the supply and demand that this R* is supposed to equalize?) It would make sense in the old world where the Fed tried to control the supply of money - but these days it only tries to affect the demand for money by influencing the interest rate. The Fed must control one or the other for the market to be determined.

IDK if "long and variable lags" is what you think it means, given that you've already cited Romer's work and used that to form your basis of when to expect a recession.

Scenario = 3Q 2024 recession

KD: "See! I was right!"

Scenario = 4Q 2024 recession

KD: "See! I was right!"

Scenario = 1Q 2025 recession

KD: "See! I was right!"

[...]

Scenario = 1Q 2030 recession

KD: "See! I was right!"

It didn't seem to slow down the sale of the house two doors down from us - it went in less than a week.

I'd buy a new car at these rates, if Honda had their new Civic Hatchback Hybrid on the market. Looks like I'm stuck with Prius, timing for December but not at all thinking about interest rates.

In that Krugman piece, he suggests that, even if we do get a recession, it will be mild and brief, because, I gather, of the unnecessary nature (and presumably easily reversable) of the rate rise.