E.J. Dionne writes today about inflation. But I would like to dissent in part and concur in part. Here's what he says:

I was among those who did underestimate the immediate threat of inflation in early 2021, so I salute those (notably former treasury secretary Lawrence H. Summers) who warned us about what was coming....[But] at the risk of oversimplifying, inflation hawks examine our situation and see something approaching the situation of the 1970s: inflation roaring out of control and in danger of becoming embedded in the economy.

....But it’s not the 1970s anymore. Jared Bernstein, a longtime adviser to President Biden and a member of the White House Council of Economic Advisers, points to three big differences. First, the inflation of the ’70s was driven by big oil price shocks....Second, unlike now, unions were still strong in the 1970s.

....The third difference: The Federal Reserve has a much better understanding than in earlier years of the “underlying mechanisms of inflation.”

I concur with Dionne's basic thesis: Inflation hawks have spent the past 40 years warning over and over that liberal policies would send inflation spiraling, just like the 1970s, and for 40 years they've been wrong. But eventually we were bound to get a bout of inflation. Even if they were right this time, they're more like a stopped clock than a Swiss watch.

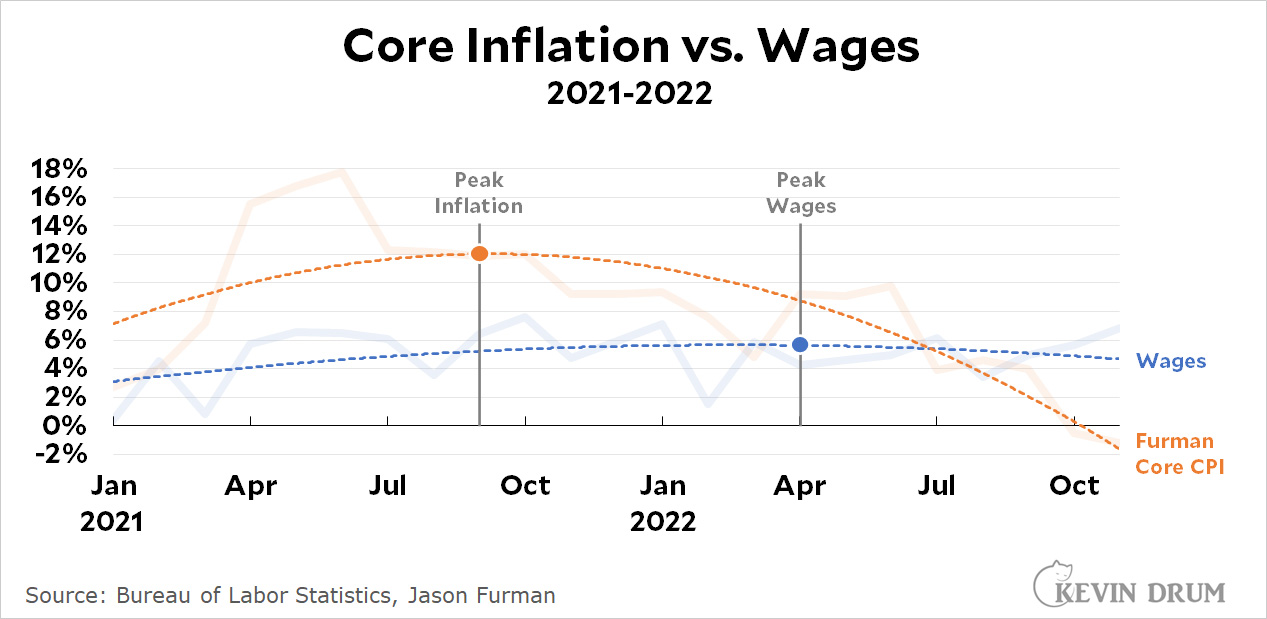

But I dissent from the rest. They weren't right. As time goes by and we get more data and a better sense of what that data means, inflation has started to look very different than we thought. Take a look at this chart:

It's a little complicated. Sorry about that. But the orange line shows Jason Furman's revised measurement of core inflation using actual rents instead of official BLS rent measurements that are six months out of date. What we now know is that rents skyrocketed in mid-2021 and core inflation was even higher than we thought. It hit 18% month-over-month in June of 2021!

It's a little complicated. Sorry about that. But the orange line shows Jason Furman's revised measurement of core inflation using actual rents instead of official BLS rent measurements that are six months out of date. What we now know is that rents skyrocketed in mid-2021 and core inflation was even higher than we thought. It hit 18% month-over-month in June of 2021!

But don't look at that. Look at the trendline. It's just a simple least-squares regression, so it's not rocket science. But it does a good job of smoothing the monthly data, and we now have figures for nearly two years to look at. Here's what it shows us: the trendline for modified core inflation peaked in September 2021 and then started declining.

Team Transitory was right all along. When you look at a better measure of core inflation, it peaked higher than we thought and sooner than we thought. It's been declining pretty steadily for the past 15 months.

As for wages, the blue line shows nominal hourly wage growth over the past two years. As you'd expect, it took a while for inflation to sink in and motivate people to demand higher wages. Its peak is seven months after the inflation peak. Wages are also more stable than inflation, so they're probably going to stay a little high for several more months, especially as workers want to make up for their losses of the past couple of years. But the trendline is still downward, and before very long it will follow the inflation numbers and drop even more.

So I dissent from the view that the inflation hawks were right. Thanks to the pandemic and its artificial rent controls, rents were a way bigger deal in our current bout of inflation than they were in the past.

By deliberately ignoring this—Larry Summers knew the rent data was wrong but pretended it meant the opposite of what it did¹—and by focusing on dumb metrics like year-over-year inflation that are practically designed to mislead in situations like this, we've spent the past year panicking over a delusive view of what's going on.

By deliberately ignoring this—Larry Summers knew the rent data was wrong but pretended it meant the opposite of what it did¹—and by focusing on dumb metrics like year-over-year inflation that are practically designed to mislead in situations like this, we've spent the past year panicking over a delusive view of what's going on.

And in case you think I forgot, there's a second phrase I highlighted from Dionne's column: namely that the modern Fed has a better understanding of "the underlying mechanisms of inflation." Am I permitted a small guffaw? As near as I can tell, literally nobody seems to understand the underlying mechanisms of inflation right now. Oh, there's lots of vague talk about supply chains and government spending and so forth, but nobody can supply a firm explanation of what really happened. So I will:

- Yes, the pandemic artificially reduced supply.

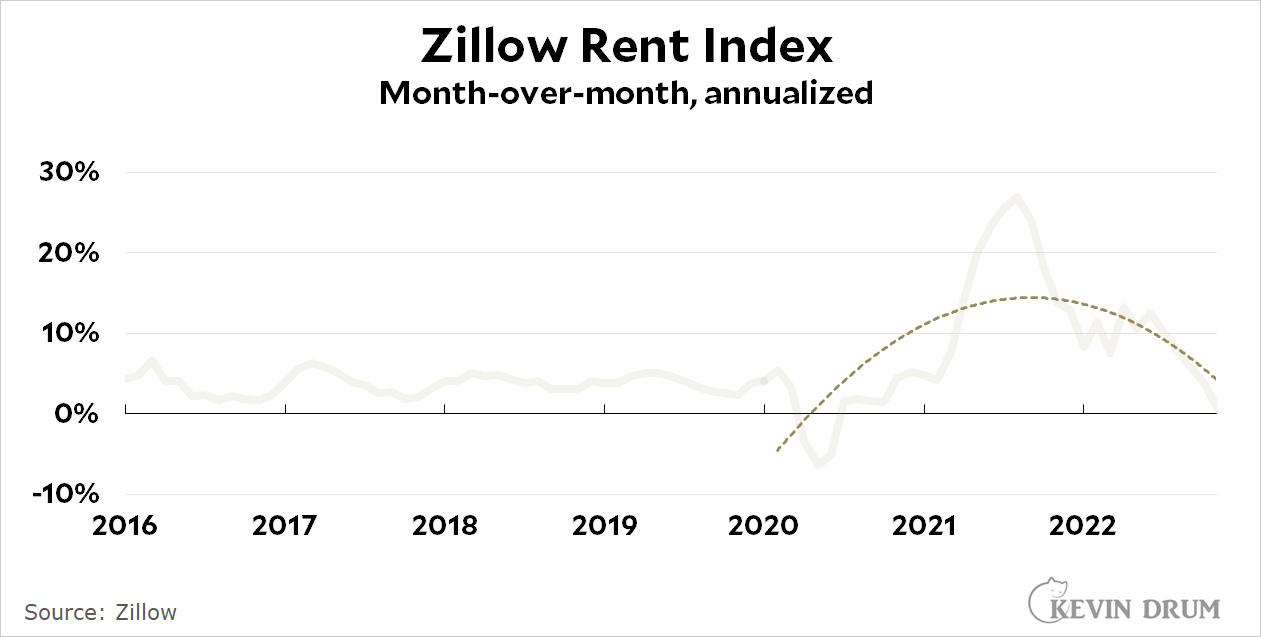

- Rents dropped at the start of the pandemic and eviction moratoriums were put in place. Rental markets overreacted to this, and in 2021 rents spiked enormously for six months before subsiding.

- Artificial fiscal stimulus kept consumers solvent and able to buy at normal levels. However, this was a minor part of core inflation (the best estimates range around two percentage points) and its influence ended quickly when the stimulus ran out.

- Savings also accumulated thanks to the stimulus. Inflation was always bound to decline as those savings were used up.

- Outside of core inflation, the Ukraine war caused energy prices to spike.

- Also outside of core inflation, food prices went up for entirely prosaic reasons: bad harvests, higher fertilizer prices, the Ukraine war, droughts overseas, and pandemic driven labor shortages. It was mostly just an unfortunate coincidence that this happened at the same time as everything else.

The bottom line is that practically everything about this inflationary episode was caused by an unprecedented pandemic that we reacted to quickly. And good for us! It's what we should have done even if we couldn't quite tune it perfectly and we ended up with perhaps a year of heightened inflation.

But it also means that it was all artificial. It wasn't due to underlying monetary policy or out-of-control spending or unions demanding higher wages. It has no analogs in the past and no lessons for the future—unless we encounter another huge pandemic. In that case it does provide a lesson: we mostly did everything right. We'll do a bit better in the future if we respond faster and more competently to the pandemic itself; adopt the same enormous fiscal response we did this time with possibly some tweaks; and maybe go easier on the eviction moratoriums, which aren't really necessary as long as we get the stimulus stuff right. That's probably about it, though I'm open to other suggestions.

MORAL OF THE STORY: We have been fooled all along because we surrendered to fears of the past and didn't look at the inflation data properly. Perhaps that was inevitable early on when data was thin, but today we have plenty of data and we know how to look at it. So now we need to do what John Maynard Keynes allegedly recommended, and change our minds when the facts change. Or, in this case, when the facts become clearer.

Our current bout of inflation was (a) completely artificial, (b) fairly short, and (c) will be completely gone within half a year. Unfortunately, monetary policy has lags, and we're still likely to pay a price next year for the higher interest rates of this year. We can only hope the damage isn't too great.

MY BIG CAVEAT: I don't know what's going to happen in China now that they've eased their COVID rules. In the worst case, they will have massive outbreaks and business shutdowns, which will either raise inflation by causing supply shortages or spur a massive recession that might reduce inflation. Or maybe neither. I have no idea.

¹Earlier this year Summers warned that the BLS rent figures were out of date, which meant official inflation figures for rent and housing were likely to go up this year because they were measuring year-old rents that had already gone up.

Think about this. He was explicitly telling us that inflation figures were going to rise because they were based partly on defective data. This should be a reason to tell us that we should calm down a bit because the official BLS figures were artificially and wrongly too high. Instead he simply said that because of the defect the official figures were going to rise and left it at that.

I would think it was a victory for Team Targeted Trendline.

I think most of what Kevin says is right, but inflation was not totally artificial. Even with different rent estimates it has still been higher than anything since the 80's. But the main causes, apart from rents, were obvious and hopefully transitory - pandemic distruptions and oil price. Many economists and the Fed directors insist on blaming inflation on the fantasy of workers demanding excessive wage increases, but this has not happened (it did not happen in the 70's either). These economists have essentially always been wrong about the causes of inflation and wrong in their predictions and there is no reason to give them credit when inflation did kick up - for predictable reasons, but not the ones they emphasized. The main key to inflation since 1972 has been oil price. When it has gone up there has been inflation and when the price rises stopped inflation fell. If oil price goes up again, so will inflation.

Taking the inflation figures from https://www.usinflationcalculator.com/inflation/historical-inflation-rates/ given that the inflation we might attribute to the oil embargo of ‘73 had bottomed out by the start of ‘77, what was the force behind the rise stating January of that year? The Iranian replacement of one dictator for another was still almost two years away.

> Am I permitted a small guffaw?

As far as I'm concerned, a large belly-laugh is quite appropriate.

For Team Powell, I have two questions: On what date did they believe the trendline would drop below 2%, and on what date did they come to that conclusion?

Inflation is caused by spending, in particular on goods and services where there is a production constraint.

David Hume wrote a couple of centuries ago ("On Money"); "If the coin be locked up in chests its effect on prices is the same as if it had been annihilated."

Kevin, you make more sense writing about inflation than most, even some whose job it is to understand it. Why does the Federal Reserve see things so differently?

Powell actually seemed to understand what was going on, but couldn't stand up to the pressure being put on him to raise interest rates primarily, I think, by the banking industry. In March, banks were earning 0.15% on reserves. Today they're earning 4.25-4.50%. (That's about $200 billion a year of more free money into the banking system.)

In addition to the observation about bank pressure, I think this touches on Powell's essential dilemma pretty well. He's the guy who bent over backwards throwing free money at everybody and everything early in the pandemic, right? But he's the Fed chair, after all, and he has to convince bankers, politicians, bond and stock traders that -now- he's really dead effing serious about doing the Fed chair's job of being Cerberus at the cash spigot. A 180. So he has to work extra hard at sounding and looking like a hardass.

And looking at today's market, he might actually be getting there now. Then over the next few meetings he can reluctantly stop hiking and later on even loosen up in quarter-point increments grumbling like he's giving away the family jewels without having everybody think it's free money time again.

I do think a longer-term and not completely indefensible goal the Fed as a whole has had for a very long time is to get long-term rates back up to their historical level around 5 or 6%. It's what was normal when these people were getting started on their careers and what has been normal through the period of European expansion going back several centuries. Whether it's realistic in this era of capital over-surplus, when holders can't seem to find productive investments to make, is something that could set them thinking about fundamentals. But that may not be in their bailiwick.

Historically, the Government sold (non-convertible) interest-bearing bonds in order to take convertible currency out of circulation temporarily. This was done to protect the Government's gold supply. The Government was, in effect, paying people not to convert their currency. Since we abandoned the gold standard, this motivation for selling bonds is obsolete. But as of yesterday, we're paying banks 4.25% to park money at the Fed, presumably for the purpose of taking (now non-convertible) currency out of circulation. The Government is paying banks something like $200B (!) a year to park money at the Fed. Why, because 5-6% interest is something we did back in the gold standard era? The bankers would love 5-6%, but what is the public purpose? Maybe we should be taking money away from them instead.

You're right, as of today the Fed is officially paying 4.4% to banks that keep their cash reserves parked in an FRB. Before 2008 it wasn't allowed to pay a penny in interest on reserves, but according to the St Louis Fed, at that time it needed to draw in as much money as possible from banks in order to do the massive bond-buying it committed to (to save the bond markets) without having too much cash flooding the economy so Congress allowed it to pay interest on the reserves-- that's what I'm getting, at least.

Anyway, seeing that the member banks get 4.4% for the idle money they're required to set aside, they're obviously going to demand something more for the overnight reserve lending they do for each other on the federal funds market.

Seeing that they got nothing on reserves before 2008, I'm not sure why they should be getting interest now, unless there's still an overriding need to keep liquidity down. Mainly I think it's both a guaranteed income to member banks, as you say, and a tool to entice or force them to raise lending rates all around.

The standard of 5 or 6% goes back, as I understand it, at least to the early days of Western commercial banking in the 15C and 16C and was arrived at because it was easy to compute and seemed "just." That wasn't a technocratic determination, of course, since they didn't inhabit the frame of mind or use the kind of money theory or tools that our technocrats use now.

What I think is a non-trivial argument for non-zero rates might be that the Fed will need to lower rates when bad times come again so they have to reach a level that would allow meaningful reductions. I don't know what that level would have to be, but 2% sounds like it's probably not where they want to be.

A seemingly trivial argument that I'm serious about is that these people came of age in a world where 5% or so was normal, actually a floor for what's normal. Something doesn't feel right, they just don't sleep right, when rates are much below that. That's just how people are.

However, we've been living for several decades now in a world awash in capital that can't find a productive return. Whether that's temporary or permanent is well beyond my pay grade. But it seems to me that while that's the case, it should affect interest rates somehow, and not toward the upside.

Correct Creigh.

Remember the 24/7 complaints that the Fed was late. the summers of this world were up in arms.

Regarding monetary inflation, I must say that real estate has been the main beneficiary of low interest rates. But this is history now.

If you want to see the impact of the Hawks, look at the ECB. Largarde under the pressure of the Germans is on track to destroy the economy, like Trichet, by raising rates agressively, pumping billions out of the systems, and all this in the middle of war/economic crisis. German savers can sleep well.

Everything in KD’s bullet list is plausible, but there is an enormous gap between a plausible, after-the-fact story and a quantitative, falsifiable model. This morning’s paper reports that the Fed OMC forecasts that inflation will be more persistent than it thought previously. There wasn’t even a vague suggestion of an empirical basis for this.

So, I strongly agree that “literally nobody seems to understand the underlying mechanisms of inflation right now.” There isn’t even a single phenomenon of inflation - there are clearly many factors that can drive a broad spectrum of price increases. We would do well to understand the problem better before applying drastic ‘solutions’.

For starters, would it kill anyone (except the usual politicians) to stop with the 'inflation' moniker? At the very least, use it as the second part of a hyphenation to signify that you're at least trying to do a differential diagnosis. As it is, 'inflation' is about as useful a term as 'consumption' was back in the day when it comes to specifying causes rather than symptoms.

Yes, I know, Scentofviolets you think I am a Trumpy (or something equally untrue).

I must ask, when a person goes to the store and at item is materially more expensive than their recent memory, why is inflation not the correct term?

When a person is updating a household budget, thinking about their work compensation etc how is inflation not useful?

Of course a price increase of “an item” is not inflation, it’s just a higher price for one item. Inflation is a decline in value of a currency, evidenced when ‘all’ prices rise. Besides which, we weren’t talking about how the man on the street should think about general increases in prices, but about how economists and policy-makers should think about such episodes.

KenSchulz - while I generally agree with your stated (explanation on inflation) I was responding to ScentOfViolets: the average person does not think of the supply of currency and its relative buying power.

Rather, for most individuals, they see the items they normally purchase. They recall that an item, or basket of items, used to cost X and now is much higher than X. So they don't focus in on 1) quality improvements 2) items they don't consume 3) prices in different parts of the country.

For a different point of view, I found this interview with Mohamed El-Erian (PIMCO) interesting, On the short, team transitory assume regression to the mean: El-Erian holds that is an error...

https://podcasts.apple.com/us/podcast/the-ezra-klein-show/id1548604447?i=1000589571549

Oh, damn, you pushed me into pedant mode again. ‘Regression to the mean’ is a purely statistical observation. Measurements of economic variables generally include lots of Gaussian noise; large absolute values of noise are less likely than small absolute values. Extreme measurements likely have an unusually large component of noise, but, if a subsequent measure is taken, it is unlikely to also have a large error, so will fall closer to the mean.

What El-Erian is talking about is a reversion to long-term trend, not because of statistical artifacts, but because disturbances that forced deviations from trend abate.

Ugh. A couple of years ago we got a variable rate HELOC with an initial rate of 2.25%. We were going to to some home renovations but took almost two years to get three prices from contractors. This all started pre-covid so we assumed the risk of a variable rate was minimal.

The rate is now 6.3% (not counting yesterday's increase) so we are going to be putting this work on hold for the foreseeable future. For once I am happy with the insanely slow response time of contractors.

Happy we dodged the bullet. But come the new year it is back to weekly Home Depot runs for me and vacations spent doing work my geezer knees can no longer handle.

Whose this 'we' you speak of, Kemosobe?

I have been critical of Kevin's views on inflation for a while, but this post is incredibly well-argued, with real data to back it up, and without the frankly ridiculous suggestion that Jay Powell is trying to hurt Joe Biden for political reasons which has made much of Kevin's prior arguments on inflation hard to swallow.

Some questions I still have:

* Do you really think it was the eviction moratoria and not the generally state of the housing market in general that caused rents to spike? People were spending way more time at home and thus wanted more space. People who used to have roommates or live with their parents were finding they wanted their own place. I know you generally don't think that supply and demand has anything to do with housing prices, but in this case, isn't that at least part of the cause?

* Why is non-housing core services inflation still high? When it will come down?

* It looks to my eyes like Furman's measure had leveled out from Fall '21 - Spring '22, but then took a dramatic downward turn during Summer and Fall '22. Are you still sticking to your story that Fed policy hasn't had any impact yet?

One data point on wages... my employer announced yesterday a one time $2500 inflation bonus for all OTE. Good for them! I'm salaried so not eligible, but this is awesome.

The rental market is changing.

Investors are buying up single family homes, driving up prices and first time buyers out--to rent them to those who could no longer buy.

AirBnB type renting gets people in favorite places much more return on investment than renting yearly to locals. So more units go up on AirBnB and fewer available tor residents.

The "work from home" trend has lowered the business tax base in many areas, raising the property tax on home owners.

These pressures are pushing lower and even middle class away from home ownership.

Not so clear from the data yet. But data not "age adjusted"--demographics play a role:

https://fredblog.stlouisfed.org/2016/10/homeowners-slide-and-renters-rise/?utm_source=series_page&utm_medium=related_content&utm_term=related_resources&utm_campaign=fredblog

Great post as usual.

The one thing that remains mysterious to me: why exactly did rents spike in 2021? Was that an effect of eviction moratoriums? How did that work?

This is obviously a huge part of the inflation story but unlike most of the other pieces (food, fuel, etc) I don’t feel like anyone has really explained what caused it.

I'm a long way past statistics classes, but doesn't Least Squares Regression give a line, not a curve?

Least-squares fits can be made for any polynomial, the first-degree polynomial being the straight-line function; however, LS estimates for third-degree (cubic) equations are rare.

LS fits can also be done for other function families - exponential, e.g.

But which function family is Kevin Drum using for his fit? Has he said?

Least Squares Regression refers to the fact that the fit is a linear combination of the regressors, not that the regressors themselves are linear. You can regress on 1, x, x^2, and x^3, for example, and what you'll get as output is the polynomial a0*1+a1*x+a2*x^2+a3*x^3 ... which is linear on 1, x , x^2, and x^3. If you still don't believe me, check out the Vandermonde matrix and what its applications.

In the worst case, they will have massive outbreaks and business shutdowns, which will either raise inflation by causing supply shortages or spur a massive recession that might reduce inflation. Or maybe neither. I have no idea.

My observation here in China suggests there will be disruptions, but they'll be very brief. The country is absolutely engulfed in covid, if my circle of friends and acquaintances (mostly in Beijing, but some scattered in other cities such as Guangzhou and Chengdu) is anything to go by. We've gone from Fauciville to Sturgis in the space of ten days. Truly explosive. But that very rapidity to me suggests the recovery will swiftly follow. I wouldn't be surprised if Beijing reaches peak spread from this wave in the next few days. Also, this part is especially anecdotal as I don't have access to detailed data on mortality and hospitalizations*, but symptomatic covid appears here appears to be pretty mild. I've got it myself. Definitely less uncomfortable than any bout of the flu I've endured, and frankly milder than a lot of colds.

And the Chinese workforce is overwhelmingly vaccinated (old people not so much).

*Nobody does. Xi's not a big fan of transparency.

Summers was aware of what was going on...but would prefer not to have a month to month inflation rate (annualized) of 18%.... In part, that would scare people, but also because that kind of swing does not compute. That also means increased inflation hawkery. The question becomes, do you want to push inflation rate down, or do you want to push prices down to trend line. If it's the latter case, then you push for a recession.

Housing prices have gone up for a while, but not so many new units, especially for middle class and kids starting out. It's a bit of a dysfunctional market, with all the players going for the high end crowd. Part of the distortion has been the hot real estate markets in major cites funded by the uber wealthy who barely live there (if at all). Get rid of Trump's tax cuts to start...

If you preface inflation as both transitory and exogenous, it becomes clearer to others that to seriously change inflation, one has to address those exogenous events/effects.

Nonetheless, Fed Bank actions intrinsically affect inflation.

Their actions are less driven by the direction of inflation expectations and the direction of core PCE right now than the macro tools that indicate entrenched inflation: Phillips Curve and the Beveridge Curve.

IMO, if you want to influence Fed actions, you have to talk about the Phillips Curve and the Beveridge Curve. All other talk is fluff.

IMHO by far the most interesting explanation for inflation, at least this time round, is given by Steve Randy Waldman at

https://www.interfluidity.com/v2/9566.html

You left off corporations gratuitously increasing profits by raising prices.

Team Transitory, fall 2021: These few months of spiking prices are transitory. In a few months inflation will be back to normal.

Federal Reserve, December 2021: Looks like this high inflation is not abating, we'll have to move interest rates a lot higher in 2022.

Team Transitory: But no! You don't have to do that, please don't!

Inflation, through September 2022: [Rolls along well above 2%.]

Federal Reserve, throughout 2022: [Raises rates a lot.]

Inflation, late 2022: [Starts to look better.]

Federal Reserve, December 2022: We'll be raising rates a lot less next year.

Kevin Drum, December 2022: Inflation was very high for two years, but now it seems back to normal. Team Transitory was right! The Federal Reserve understands nothing!

Federal Reserve: Are you kidding me?

I mean, it's like Kevin Drum looked at the lessening covid death rates, and pronounced that the deniers, anti-maskers, and anti-vaxers were right all along. Silly CDC!