Larry Summers makes the case on Twitter that inflation is stubbornly here to stay unless the Fed takes aggressive action. He has six arguments:

- Inflation expectations may still be anchored, but this is largely based on the belief that we're headed toward a recession.

- Core inflation is robust and the labor market is tight.

- The economy is overheated.

- Historically, it's been impossible to produce a "soft landing."

- Risk management suggests that inflation is our biggest problem. If anything, we should err on the side of aggressive action to bring it down.

- Nobody really understands inflation anyway.

Let's take these one by one.

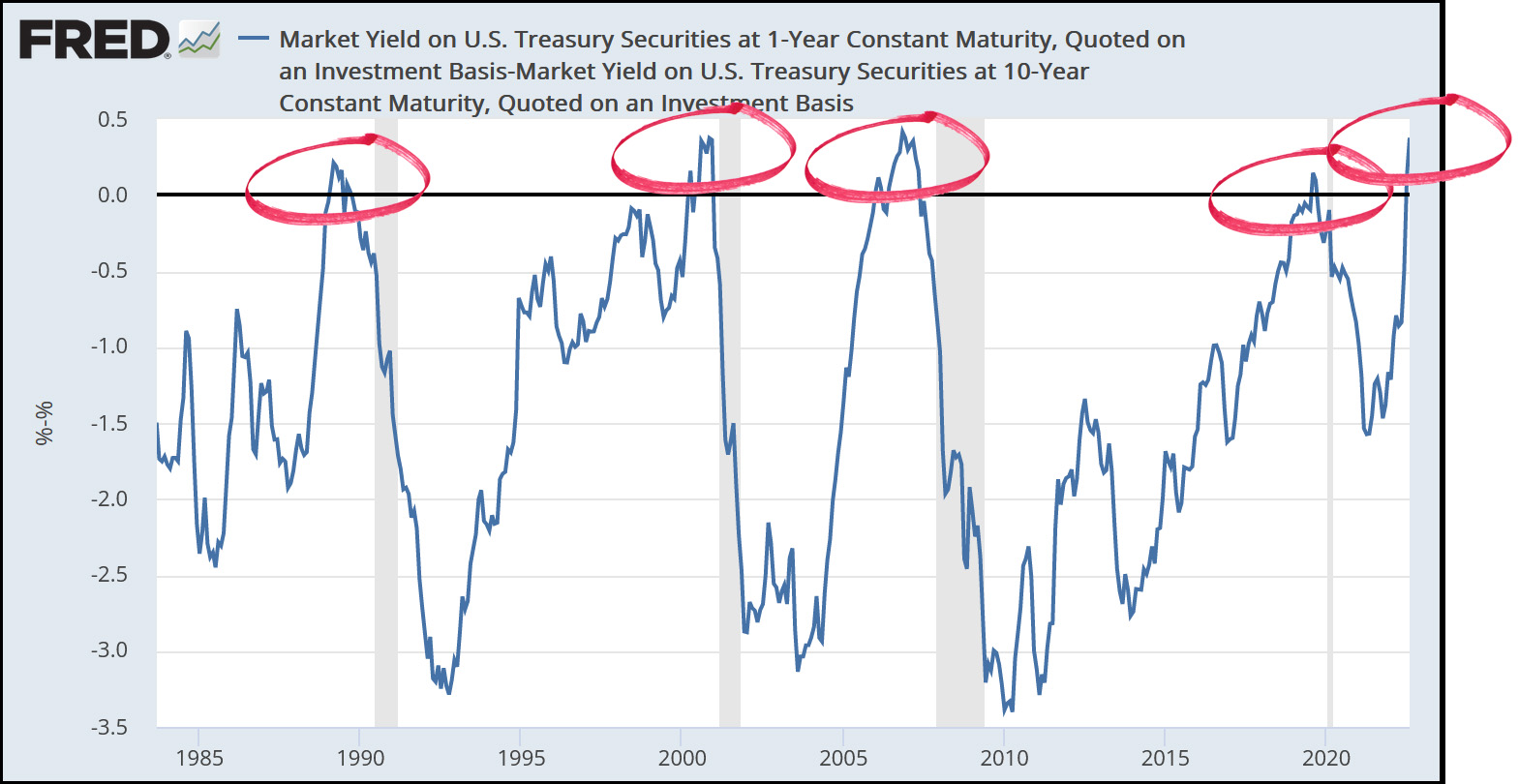

1. Maybe! There aren't very many good recession predictors, but the good ol' inverted yield curve seems to do the best job. Here it is:

The inverted yield curve has correctly predicted the past four recessions, and right now it's predicting another one in the early part of next year.

The inverted yield curve has correctly predicted the past four recessions, and right now it's predicting another one in the early part of next year.

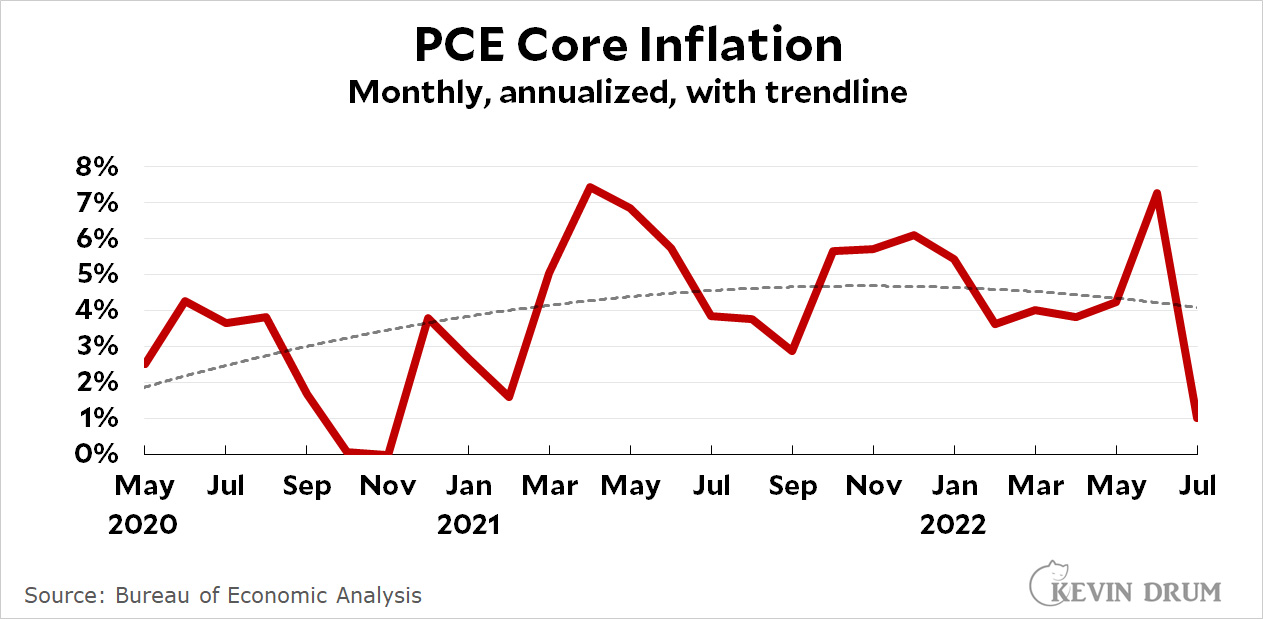

2. Here is core inflation:

It seems to have peaked at the beginning of 2022 and is now slowly receding.

It seems to have peaked at the beginning of 2022 and is now slowly receding.

As for the labor market, the data is inconclusive. Unemployment is at 3.7%, which suggests tightness. On the other hand, the labor force participation rate is still below its pre-pandemic level; weekly hours have been declining; and real wages have been falling for two years. This all suggests a little bit of looseness. Overall, the labor market appears to be close to full employment, but perhaps not quite there.

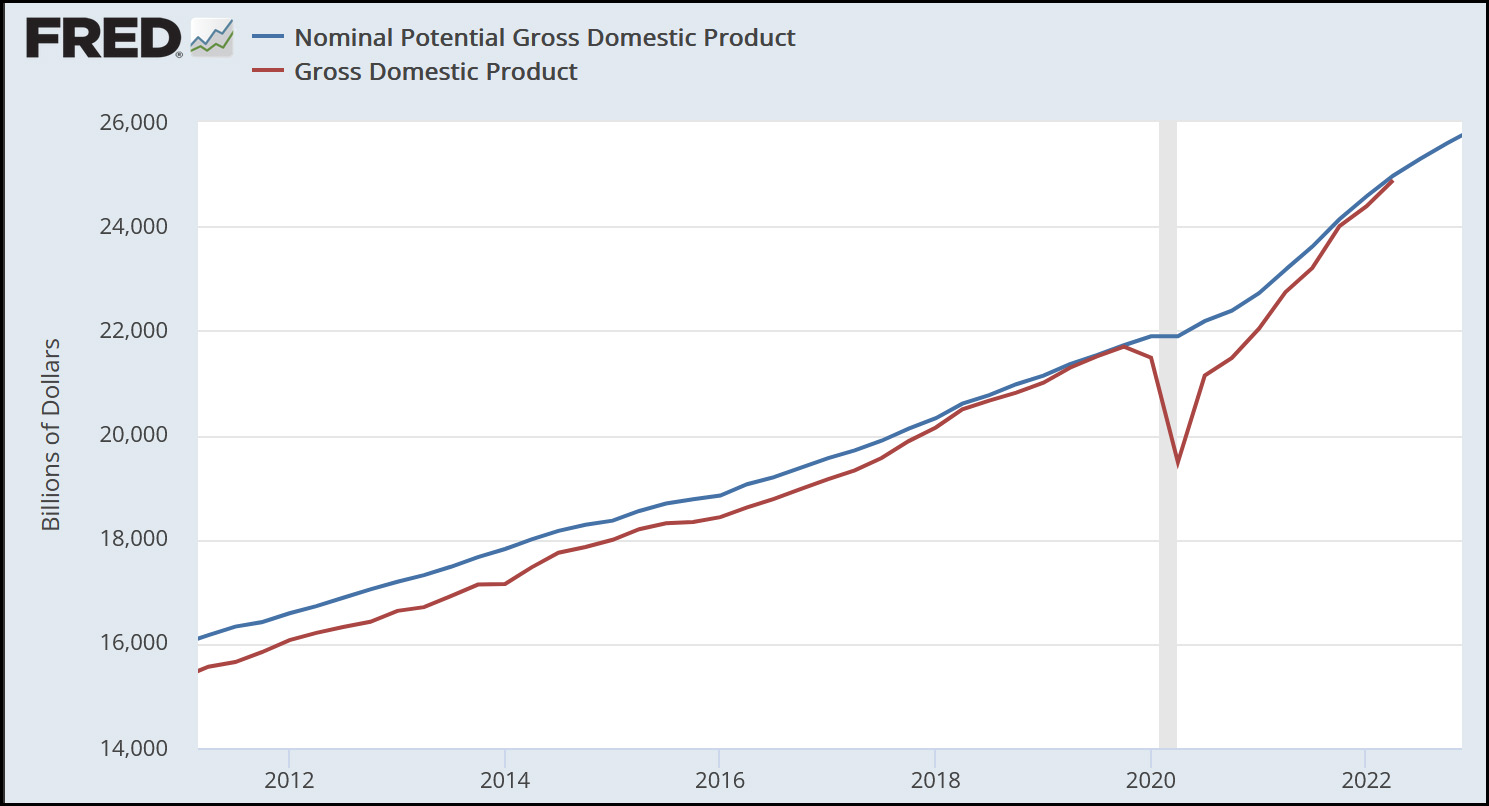

3. Here is GDP vs. potential GDP:

We have not yet hit potential GDP, let alone crossed it. This suggests the economy isn't overheated. On the other hand, we're pretty close. And inflation is high, which is the other classic sign of an overheated economy.

We have not yet hit potential GDP, let alone crossed it. This suggests the economy isn't overheated. On the other hand, we're pretty close. And inflation is high, which is the other classic sign of an overheated economy.

4. Soft landings are indeed difficult to pull off. On the other hand, it's not clear how hard we've ever tried to engineer one. The Fed tends to respond to inflation and only inflation. That's always likely to produce a hard landing.

5 & 6. Which side we should err on depends a lot on which side of the economic divide you're on. If you're old and rich, then yes, we should kill inflation wherever it appears. But if you're young and in danger of losing your job, maybe you think inflation is not the worst thing in the world.

FINAL SCORE: Really, Summers only made testable statements in 1, 2, and 3. And they're close calls. #1 supports his guess about anchored inflation expectations. #2 doesn't support his statement about core PCE being robust, and is half right about the tight labor market. #3 doesn't yet support his belief that the economy is overheated, but it's close. #4 is hard to argue with, but why not try anyway?

So it looks to me like we're on a knife edge. We probably are headed for a recession, but it's not clear to me that the rest of the data supports the notion that the Fed needs to engineer a deeper recession than we're already going to have anyway. They should pull back a bit and let the economy lose steam on its own.

Inverted yield curve flopped before.

Raise taxes on the rich to decrease inflation, ease house prices without increasing unemployment.

Inflation is already collapsing. Follow money supply % change of M2. It's as low as it was in the 10's. The morons who don't get this will be left on the dust bin of history.

Raise taxes on the rich to decrease inflation,

Low propensity to spend. You need to make taxes bite broadly if you want to go that route.

Lots of high-income high-income households with a high marginal propensity to spend - https://equitablegrowth.org/wealth-inequality-marginal-propensity-consume/

I'm with Boronx, and Willie Sutton - the taxman, like the bank robber, needs to go where the money is.

Yes. Fortunately, the part of the Iflation Reduction Act that provides substantial resources to the IRS is following the Willie Sutton principle.

Let's not confuse our policy predilections ("It's bad to reduce the living standards of the non-rich!"—as it happens I agree with that one) with what is likely to be effective.

In any event we're discussing a hypothetical, as we're not going to see Congress pass a tax to cut inflation.

What is likely to be effective, if one thinks that the answer to supply disruption is limiting aggregate demand, is to reduce discretionary spending in the aggregate. The wealthy may have a lower propensity to spend, but they have much more disposable income.

To people like Summers the only way to fight inflation is to inflict pain and suffering on workers. The rich should never be negatively impacted or they'll take their job creating ball and go home.

Larry Summers is a brilliant economist. He also is the principal member of Team Permanent. The two identities tend to work against each other.

And if guys like him as well as the mainstream media keep telling the public that inflation will last them of course people will expect it to. It’s is likely to become a classic self-fulfilling prophecy.

If he's that brilliant, why is he wrong so often? His record is terrible. He just says the right things to the right people.

He says the things The People That Matter want to hear.

As long as the yield curve remains inverted the risk of recession is real (though how that happens with full employment is a mystery), the point being that the best course of action for the Fed is to wait and see since Inflation does not look like a threat to the economy.

Summers is right on his last point that nobody really understands inflation anyway - at least to the point of being able to predict it. Many economists, including Summers, have repeatedly predicted inflation before since the 80's on the basis of their understanding of "theory" but have always been wrong. Inflation does kick up from time to time, but that does not mean they have gotten it right that time.

If Summers is right on this last point, then that makes his claims in the previous points worthless - like others, he doesn't understand inflation so why should anyone believe his predictions?

What does often control inflation, as I have often pointed out before, is large changes in oil price, and that this is subject to various geopolitical factors, especially war. In Europe natural gas price is obviously also controlling. Can Summers - or anybody - predict what oil and gas prices will be doing?

".... like others, he doesn't understand inflation so why should anyone beleve his preddictions?"

Because he is confused at a higher level than us, mere mortals.

Clearly the economy is suffering from an imbalance of humours, oops, supply and demand, and bloodletting is the only remedy! Theodoric of York approves.

Thanks for this overview Kevin. Unless the Russian invasion of Ukraine is resolved very soon, I don't see how Europe avoids a Winter energy crisis that pushes the continent into a fairly severe recession. The spillover will ikely halt US GDP growth and increase joblessness which to me means that the FED has done its work and they can pause rate hikes until there's clarity on how badly the US catches the European flu.

Dude, Russian exports can be replaced. Your point is dead. Matter of fact, it's creating a production bubble in all lng production and large overbuild to come.

No expert I have read or heard believes that Russian natural gas exports can be replaced quickly enough for Europe to get through this winter. The way to do that is to import Liquid Natural Gas from countries like the US but there are not enough facilities at the European port that have the capacity to handle a lot of LNG and getting there can’t be done overnight. And there are no other energy sources that can be ramped up quickly enough to meet the upcoming winter needs.

Right now European countries are working to keep energy companies from bankrupting average people but that will do nothing to help meet energy demands.

No one expects 100% replacement, but there are other LNG supplies, and they are already putting systems in place for unloading the gas. Bloomberg had an article on one in Holland that is already in use. It is supposedly capable of unloading enough gas in a month to supply Holland for a year. There is already a pipeline network in Europe, so this gas will be widely distributed, as will gas brought in at other points.

(If Russia and China strike a deal, that will free up gas that otherwise would have been sold to China.)

The spillover will likely halt US GDP growth and increase joblessness

Unlikely to have much effect. Europe only buy about 2-3% of US output, and even a fairly sharp recession there isn't going to decrease their imports from the US all the way down to zero. Plus, the additional downward pressure on oil prices flowing from a European recession will help US consumers.

A European recession is going to exert downward pressure on global growth next year, true, but the effects on the US will be modest.

The PCE inflation rate has been above the Fed's 2% target for 17 of the last 18 months, and for most of those months it's been at 4% annualized or higher. I'd agree with Summers that this is robust. I don't think there's any theoretical or empirical basis for believing the trend line's slight downturn is predictive.

PCE core inflation, I meant to say.

Dude, things change. I mean, what brain impulse are you using?????

In his column today Paul Krugman cites factors like significantly decreased shipping costs that help keep inflation down and aren’t likely to be temporary.

What might be predictive is not trend lines, but the return to normal of some things which have been out of whack because of the pandemic. This includes supply chain problems, catch-up consumer spending, stimulus money, computer-chip factory problem, etc. The oil/gas supply problem does not stem from the pandemic, but from Putin. This is not predictable.

All year I've been inclined to think that inflation was going to ease up soon, and I hope it's starting to. I guess the Ukraine war has been a big factor.

Drum, the Fed doesn't engineer nothing. It was arguably the 99-00 rate hikes which help spur the housing bubble. A increase of leverage with higher rates is a historical norm.

The price of TIPS vs the price of regular Treasuries show that the market expects inflation to be just less than 2.5% over the next 5 years and then drop a little to below 2.4% for the following 5 years.

I don't know what will happen but I know that the market is smarter than you or I or even Larry Summers.

I too was taught to use the TIPS spread to calculate the market's expectations for inflation. Then again, I was also taught that the market has perfect information and acts rationally...lol

Whether TIPS buyers are smarter than Summers or not, they are among the people who determine expectations in the economy, and those expectations are themselves considered by economists to be major influences on inflation. Consumer expectations in the University of Michigan survey are also not very high, as Krugman has pointed out.

Lots of uncertainty in the current data, guesstimates of the near future and in our understanding of what forces influence the data.....and given that uncertainty it's safe to say that we should try throwing millions out of work and check back after 18 months. If we are wrong, we can always cut taxes to stimulate the economy and try to do better next time.

I hope this is snark ...

" .... throwing millions out of work .... check back after 18 months .... if we were wrong we can always cut taxes ...."

Heads labor loses, tails capital wins - sounds like business as usual.

+1

Let us never agree to tax cuts or programs to create “good paying” jobs ever again. We wouldn’t want the economy to overheat and cause inflation. This is a ridiculous argument.

War and stupid globalization polices. If we need to make a change let’s at least stop pretending that Chinese junk and Russian gas are part of the answer.

Hey, I'm agreeing with Justin. And I never called him a troll. Dyspeptic misanthrope, maybe, but not a troll.

Thanks! You’re a fine human being!

When inflation spiked, the NYT and other publications listed factors driving it upwards. There were few if any that seemed likely to be affected by higher borrowing costs.

+1

It is amusing to watch the type of trend line shift to the version which supports the narrative of the day.

It's good that we have people like Larry Summers that are willing to make the "tough calls" and put other people out of work. Since nobody really understands inflation, I'm going to stay on team temporary; without wage increases, and they don't seem to be happening, the economy isn't over heated. In any event, there are good reasons for a 4% inflation target at full employment and I don't think we are far off from that.

Throughout 2021 Kevin asserted that inflation was not, or not going to be, a problem Lot's of cherries were picked.

I haven't read anything from Kevin explaining why he was so wrong. Until he can explain why his current analysis is different than before (and those charts he's put out today sure look familiar) I'm not going to be reassured. Gotta love the PCE Core trend line. What order polynomial is it this time?

I don’t recall KD saying that inflation wouldn’t be a problem; I recall him saying it would be a temporary problem. ‘Temporary’ doesn’t have a precise definition, though.

On inflation and inverted yields

Inverted yields are correlated to recessions but are signals of short-term uncertainty. Take a closer look at that FRED chart: https://fred.stlouisfed.org/graph/?g=TyNF

We're supposed to believe that because an inversion occurred anywhere between 6 months and 2 years prior to a recession, therefore, it is a great signal of an oncoming recession. Please. It's a signal of uncertainty. I included the 1-yr yield to make this point.

Naturally, with high inflation -- whether headline or core -- that we haven't seen since late-70s to early-80s, people are driven by uncertainty and the fears of inflation expectations anchored at an elevated level.

On labor tightness

With regards to labor tightness, it is not ambiguous: Labor is exceptionally tight. It is quantified by the Beveridge Curve and the UV ratio. This is stuff that Janet Yellen has cut her teeth on. This is what many economists are looking at, wondering why (real) wages haven't soared.

Whether or not a soft landing can be done might be less relevant than the economy's capacity to lower the ratio of vacancies to unemployed persons. Think of it as insurance against the possibility of elevated anchored inflation expectations and the fears of a wage-price spiral.

The people most flummoxed by mixed signals are those most attached to economic orthodoxy.

Wages haven't soared because the GOP's decades-long war against the unions has been highly successful. Workers have little bargaining power, even when the labor market is 'tight'. It isn't as tight as it appears, either, given the long-term decline in the LFPR. The reserve army of the unemployed may be small, but it is backed by the reserve army of workers on the sidelines.

Labor Unions do not need tight labor markets to have leverage, though. That is the point of unionizing, after all.

Wages have been held back for a different reason, I believe.

You don’t think maybe the 50% decline in union membership since the 1980s has something to do with it?

https://www.bls.gov/news.release/pdf/union2.pdf

Over the long haul, unions have strong effects on wages and benefits. In the short term, it's negligible.

Union wages will only experience growth only after a contract has expired and renegotiated. Since most contracts are multi-year (2-5, generally) you would not expect a strong effect on wages in the short-term.

In the Great Recession V/U = 0.18. People held onto their jobs by taking pay cuts while others were willing to take any work regardless of wage. For the last 6 months or so, V/U = 1.8. That's historically high, so there should be upward wage pressure.

Yeah, that’s why I cited data spanning forty years. Economists expect the ‘tight labor market’ to cause upward wage pressure; Kevin has posted a number of charts that don’t support that claim.

You are forgetting the most reliable predictor over the years: Larry Summers is always wrong. You can bank on it.

Isn't Larry Summers nursing a streak of wrong predictions rather long?

https://youtu.be/VAYPNF4aIf0

(Anytime Larry Summers is in the news, it's mandatory to post this.)