Asked by NBC News' Lester Holt whether he considered Trump "responsible" for the violence at the Capitol, Barr said: "I do think he was responsible in the broad sense of that word, in that it appears that part of the plan was to send this group up to the Hill. I think the whole idea was to intimidate Congress. And I think that that was wrong."

....But asked if he would vote for Trump if he wins the party nomination in 2024, Barr suggested he would. “Because I believe that the greatest threat to the country is the progressive agenda being pushed by the Democratic Party, it’s inconceivable to me that I wouldn’t vote for the Republican nominee,” he said.

Barr has spent the past couple of decades swirling down the rabbit hole of conservative paranoia, but he's still emblematic of a real problem: Republicans who are genuinely disgusted by Trump but aren't willing to do the one meaningful thing that would weaken his hold on the Republican Party. They aren't willing to vote against him.

I've come across this often enough that it strikes me as a genuinely widespread phenomenon.¹ The upshot is that it's not enough to go after Trump. Plenty of center-righties already understand perfectly well that the man is a disaster in human skin. The problem is that many (most?) of them don't feel like they have any reasonable alternative. This is partly because of Fox News & Co. and partly because of the leftward migration of the Democratic Party.

But whatever the cause, it's a problem. And fair or not, we need to do something about it.

¹If there's some kind of survey data that says otherwise, let me know.

Axios is a news site founded by the founder of Politico, and it's famous for presenting the news in a short, bullet-pointed, and easily mockable format. However, I know all about that, so I wasn't very interested in today's New York Times feature about Axios. But I read it anyway, and I'm glad I did. It turns out that there are a lot of people who wish they could write more like Axios, and now there's software that does just that:

Axios HQ, which promises to teach corporate America how to trim the jargon, is separate from the newsroom. Companies pay about $10,000 for an annual contract and use the software to write team updates and sales notes, Mr. Zaslav said.

The software uses artificial intelligence to suggest editing and formatting to distill blocks of texts into shorter bullet points. Axios HQ also has analytics that show the clients whether employees opened the messages.

A year after its start, Axios HQ has 210 clients, from major companies like Delta Air Lines to state school systems to small start-ups, Mr. Zaslav said. He said it was aiming for 600 clients by the end of this year. The company has about 60 people working exclusively on Axios HQ.

Shazam! Software that teaches people to write more like a PowerPoint deck! I'm so old I can remember when PowerPoint-ese was considered the gravest degradation of the English language since garbage collectors became sanitation engineers.

But it makes sense. In the past few decades we've gone from magazines to blogs to Facebook posts to Twitter tweets. And all along, the technology behind this change has been driven by Silicon Valley true believers who pretend to hate PowerPoint decks but in fact can barely live without them. So why not just admit defeat and adopt the PowerPoint esthetic for all human communication?

POSTSCRIPT: Just as an aside, it's worth noting that this is hardly a brand new phenomenon. We've been told forever to "keep memos to a single page." Reader's Digest made a fortune by abridging famous novels. Every college student loves Cliffs Notes. Even the sainted Elements of Style is mostly advice about how to write shorter, punchier, prose.

Today the New York Times published an op-ed by Emma Camp, a senior at the University of Virginia. The topic was stifling wokeness on campus, and as you can imagine it was not well received on lefty Twitter.

But it provides an interesting object lesson. David Roberts tweeted that the op-ed wasn't just bad, but practically a parody. I asked what was parodic about it:

"This one time, a friend of mine said something in class & a bunch of people disagreed with her" ... offered as evidence (the ONLY evidence offered) of some dark nationwide epidemic of self-censorship ... is the kind of thing I would write were I to parody this genre.

But this is just wrong. Camp offered loads of evidence. You'll have to read the piece for yourself to get the context, but here's an abbreviated bullet list:

Hushed conversations with philosophy prof.

Friend lowers voice.

Another friend fears a defense of Thomas Jefferson.

Survey says 80% of students self censor.

Feminist theory class about criticizing suttee. Eventually class discussions "became monotonous echo chambers."

Brad Wilcox.

Stephen Wiecek.

Abby Sacks.

Samuel Abrams.

Despite this, David's tweet immediately garnered hundreds of likes from people who obviously hadn't read the op-ed. They just saw something that seemed like a great dunk and added their enthusiastic support to it.

This is typical of Twitter, which is why we should all ignore it more than we do. Most Twitter pile-ons (of which this is only a teensy example) start with one person and are then amplified into tsunamis by vast crowds who know nothing about it aside from what that first person said. In other words, they're meaningless.

What's especially ironic about this one, however, is that the Twitter mob is doing exactly what Camp says she's experienced: they are dragging her so furiously that it makes her afraid to open her mouth in the future. And you can add to that a substantial number of people who are outraged that the New York Times would even publish this, which is also the kind of thing Camp is warning about.

None of this is to say that Camp is right. Maybe she's overdramatizing things. Maybe she's cherry picking survey data. Who knows? Maybe she's outright lying about some of the events she describes. If any of that is true, then have at her. But bring receipts.

Now, obviously Camp has not, in fact, been cowed by her treatment at UVa. She's writing about it in the biggest newspaper in the country! But that doesn't mean the dynamic she's describing doesn't exist. People who have never been the target of a woke mob can confidently proclaim that this is all just a myth, but those who have been in the crosshairs know perfectly well that it's very real. That's especially true for people who are less self-assured than the average blogger or Twitter user, both of whom famously love to mix it up in verbal arenas. Less contentious—or less verbal—folks are far more vulnerable to feelings of intimidation and far less likely to ever talk about it.

It's easy to nonchalantly dismiss the experiences of others. This is nothing more than asking people to be tactful. It's called "growing up." It's just people disagreeing with you. Self-censorship is a good thing. Maybe. It's certainly true that conservatives exaggerate wokeism for political reasons. But too many liberalish folks talk about this phenomenon—both in and out of the university context—to casually dismiss it as something that's entirely made up. It isn't, and it's a problem. The first step in fixing it is to at least admit that it exists.

This is the Hollywood/Vine subway station on the LA metro's Red Line, aka the B Line. The top photo is the . . . foyer? Lobby? Whatever. It's a large space with a couple of old-timey movie projectors and some art deco palm trees. The bottom photo provides a closer look at the walls as you approach the escalator to the platform.

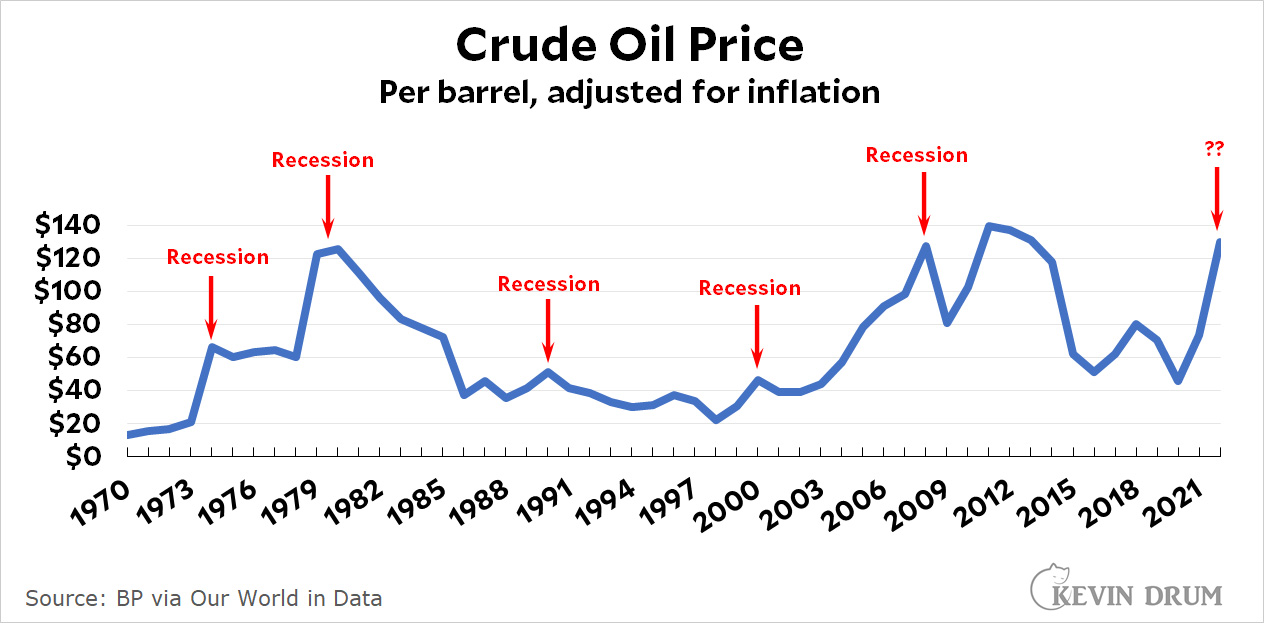

For the past 50 years, spikes in the price of crude oil have been associated with economic recessions. Big spikes are followed by big recessions and small spikes are followed by small recessions:

We are now approaching a very large spike in oil prices thanks to the Ukraine war. If this is merely a short-term response that settles down in a few weeks, it will probably have little effect. But if prices stay high for a while, we should probably brace ourselves for an economic downturn.

The Fed has signaled that it plans to raise interest rates at its next meeting in order to fight inflation. It's possible they might want to rethink that in light of current events.

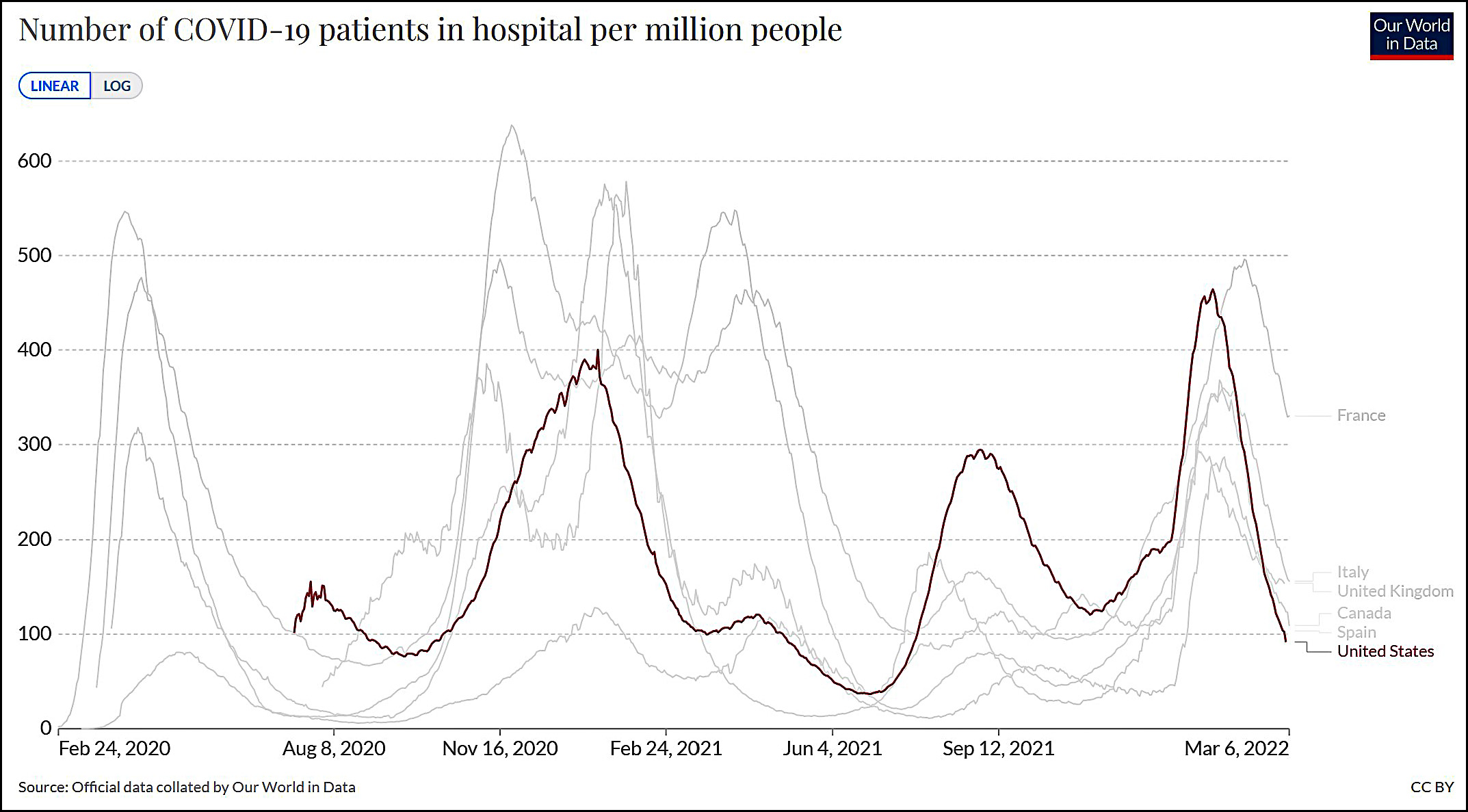

COVID hospitalizations are continuing to plummet everywhere:

I'm not sure why France is such a laggard, but even their hospitalization rate is declining rapidly. Within a couple of weeks, the US hospitalization rate should be at an all-time low.

Trump mused to donors that we should take our F-22 planes, "put the Chinese flag on them and bomb the shit out" out of Russia. "And then we say, China did it, we didn't do, China did it, and then they start fighting with each other and we sit back and watch."

I would like to take this opportunity to remind you that this man used to be president of the United States. For four years. And there are many people who would like him to be president for another four. We cannot allow this to happen.

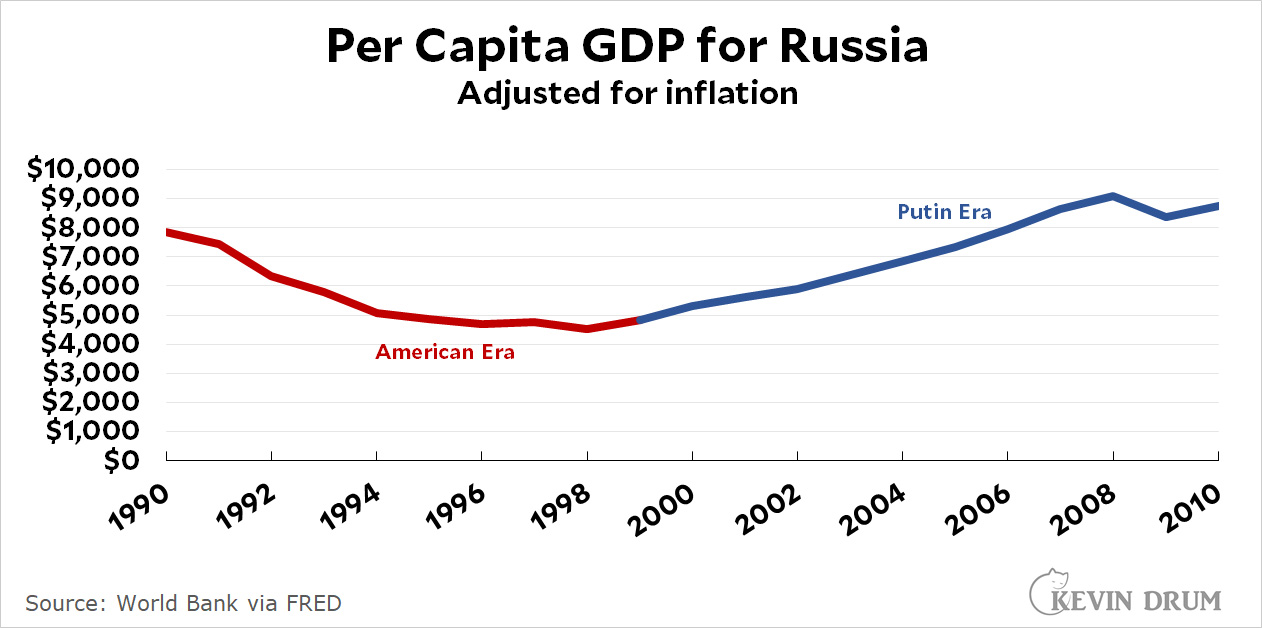

Do ordinary Russians support the Ukraine war? No one can say for sure, but a best guess is that most of them do. Why is this?

It's not so hard to figure out. First off, as background, Russians spent centuries resenting the cultural and economic dominance of the West. They especially resented it because it was true. Then they fought two world wars against Germany, followed by 40 years fighting a Cold War in which the broader West was their enemy.

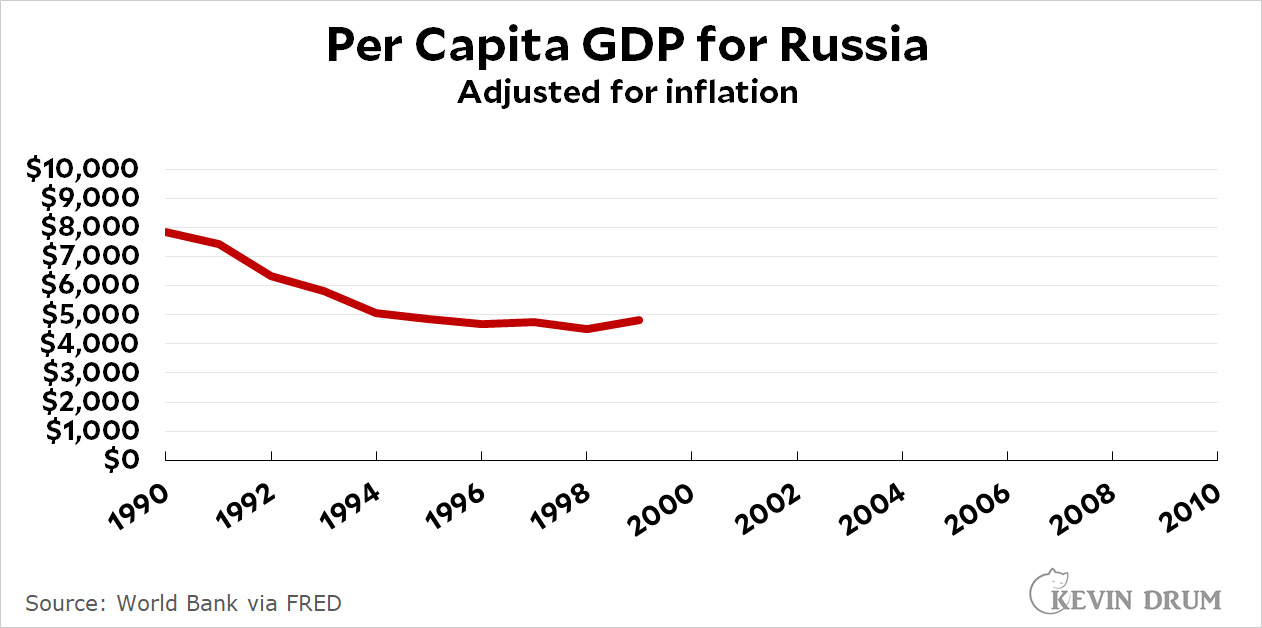

Then, thanks to Western pressure, their country disintegrated in 1991. This is not an easy thing to take. And what happens next?

The Americans send in teams of economists to make Russia a nice, capitalist country. The result is disastrous. Per capita GDP falls by half and the economy collapses. Huge companies are all but given away to oligarchs. The West takes advantage of Russia's momentary weakness to expand NATO right up to their borders, which looks like a permanent threat to Russian sovereignty and its legitimate sphere of influence.

Is it any wonder that the average Russian, living through all this, would feel like they've been treated criminally by an implacable enemy determined to keep them small and helpless?

But then Vladimir Putin becomes president. Make Russia Great Again! he says, and people see a glimmer of hope. What's more, Putin presides over a return to economic growth:

That's more like it. It shows what can happen when a real Russian is in charge who refuses to kowtow to the Americans.

And many Russians, just like many Americans, are cultural conservatives and strong nationalists. They like Putin for those reasons. They like the fact that he showed the Georgians who's boss. They like the fact that of course he permanently annexed Crimea instead of paying a lease until Ukraine eventually decided to kick them out. There's no way Russia was ever going to lose such a strategic asset, especially when the population is heavily pro-Russian.

Finally, a few months ago the United States agreed to support Ukraine's eventual membership in NATO, something that Putin has long made clear was intolerable to Russia—and probably to most Russians. It was just one more way that the Americans were gratuitously insulting Russia in its own backyard.

These are all real things. Now toss in an increasingly controlled media that makes Fox News look tame and it's hardly a surprise that most Russians view the West—and the US in particular—as enemies who won't rest until Russia is fully under their thumb. Do they believe that Ukraine is committing genocide against ethnic Russians? Or that Ukraine was getting ready to attack Russia? Why wouldn't they? They're primed to believe exactly that, and it's what Putin is telling them. Why would he be lying? And anyway, the average Russian probably believes that Ukraine is historically part of Russia as much as Alaska is historically part of the US.

But naturally the West has taken this opportunity to crush Russia further. Putin calls our economic sanctions an act of war, and who can argue with that? If anyone did to us what we're doing to them, we'd sure consider it an act of war.

In any case, this is the nickel version of what's going on. Russians have plenty of real reasons to resent the West, and that makes them perfect vessels for propaganda that cranks the resentment up to 11. Most of them probably think the invasion of Ukraine is a righteous war indeed.

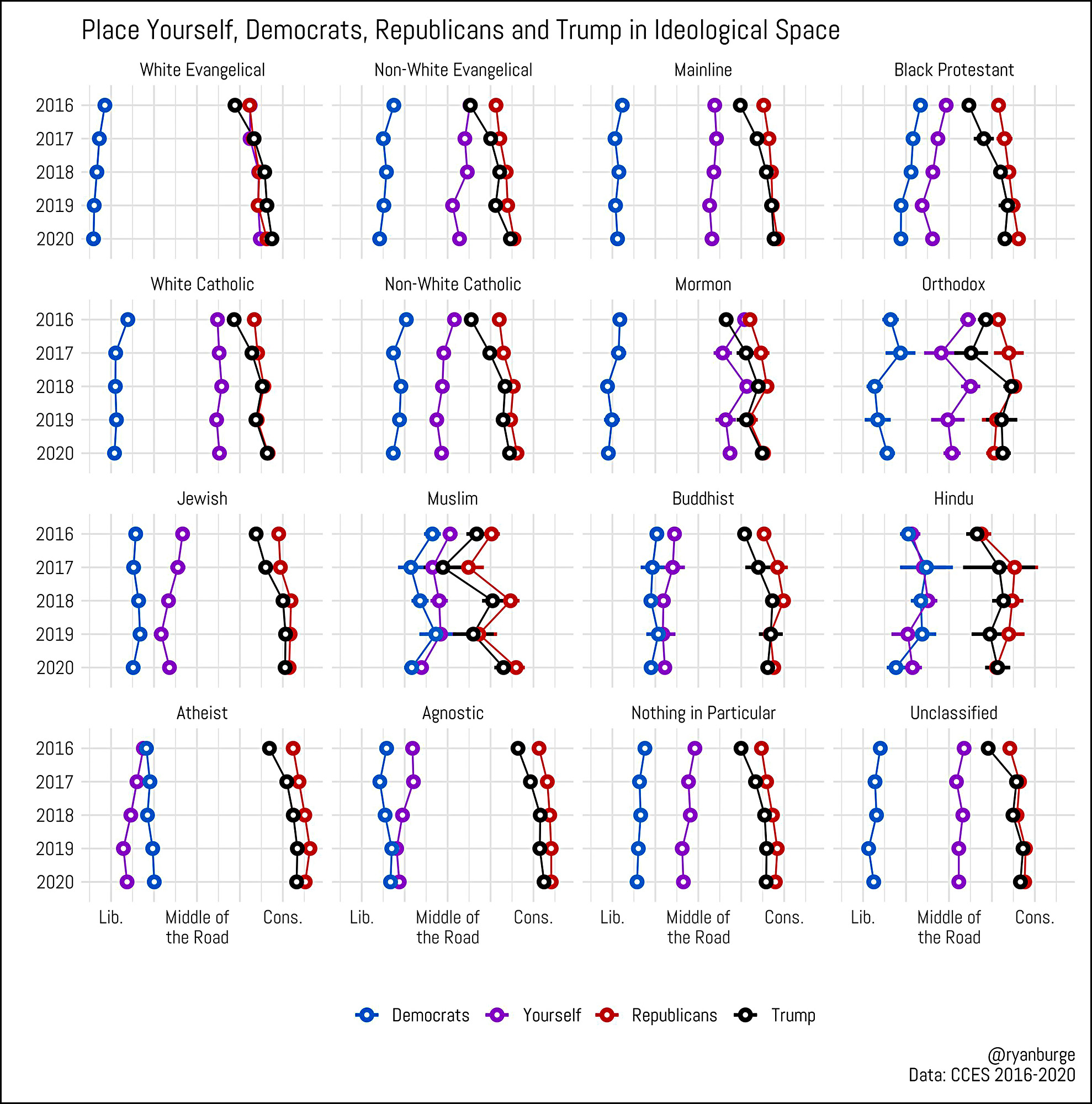

The most interesting part of this is that every single white Christian group feels closer to Republicans than Democrats. That includes not just white evangelicals, but white mainstream Protestants and white Catholics. It's only the white atheists and non-Christians who feel closer to Democrats.

Also interesting: Every white Christian group places Democrats farther to the left than they place Republicans to the right. Even the non-white groups score it as a tie. This include Black Protestants (which is most of them) who have a different view: They don't think Dems are all that far left, but they also don't think Republicans are all that far right. They prefer Dems because they view themselves as left of center.

Also of note: No one views Donald Trump as more conservative than the Republican Party—not by more than a hair, anyway. They correctly view him as basically just a standard issue Republican conservative these days. The era of Trump being a supposed rogue within the party are long gone.

According to the Washington Post, China's annual work report is a little more militant than usual about "resolving" the Taiwan issue. The change from previous annual reports is the addition of “in the new era,” which I interpret as "taking over Taiwan before Xi Jinping dies." But that's just a cynical guess from someone who knows nothing about this.

(But I do wonder what the US will do when China eventually invades Taiwan. My guess is nothing much, but again, I know nothing.)

Anyway, there's also this:

[The report] also said one of the goals this year would be to control coronavirus infections in a “targeted” way, suggesting an approaching loosening of the draconian policies that have kept China’s coronavirus infection count close to zero, but have weighed on the economy and upended daily life. “Occurrences of local cases must be handled in a scientific and targeted manner, and the normal order of work and life must be ensured,” Li said in the work report.

I dunno. China reports a very impressive vaccination rate, which doesn't surprise me since they have impressive ways of dealing with anti-vaxxers. Nonetheless, the efficacy of their vaccine is questionable and it seems like every country that eases up on pandemic restrictions eventually gets its turn in the barrel. If China does ease up—and I grant that they have to eventually—I won't be surprised if COVID-19 surges in their large and mostly naive population. There is, unfortunately, a price to be paid for being too effective in fighting COVID.