I've seen a number of people express astonishment about how we decide when recessions start. It turns out that the answer has nothing to do with two consecutive quarters of GDP decline and it never has. Rather, a group of gnomes who work for the National Bureau of Economic Research stir a bunch of stuff into a pot and eventually pick a date.

This raises a question: What the hell is going on? Who decided on this squirrely procedure? And why does this NBER outfit get to do it?

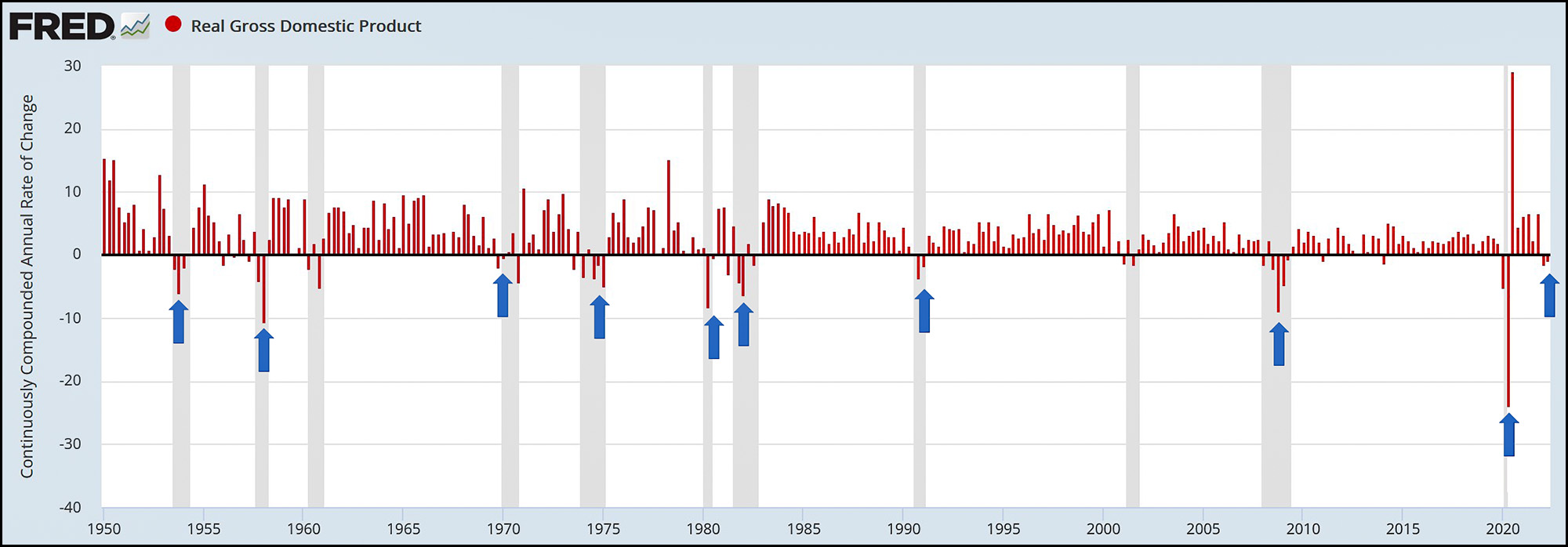

That's an interesting story, and I'll get to it shortly. First, though, here's a chart of the US economy over the past 70 years:

The blue arrows indicate all ten times that we've had two consecutive quarters of GDP decline. In every single one of those cases, NBER eventually declared a recession. This makes it highly likely that NBER will do the same this time.

The blue arrows indicate all ten times that we've had two consecutive quarters of GDP decline. In every single one of those cases, NBER eventually declared a recession. This makes it highly likely that NBER will do the same this time.

Or does it? One thing you'll also notice is that our current GDP decline is the smallest of the ten. So . . . maybe it's not a recession? How do we know? This is where our story starts.

Back in the early 20th century an economist named Wesley Clair Mitchell decided to devote his life to the empirical study of business cycles. Mitchell believed that modern industrial economies ran in irregular cycles of expansion and contraction, and these cycles affected nearly all economic activity. This was an important insight, and of course he turned out to be right—not just about the existence of the business cycle, but its importance.

Mitchell built on this insight by trying to precisely define and date business cycles. To do this he set out to gather time series of anything he could. He didn't have the BLS or the BEA or FRED, so he had to make do with whatever he was able to come up with at the time: pig iron production, bank clearing volumes, freight receipts, unemployment numbers, anecdotal evidence from business barons, dodgy business activity indexes, and anything else that might be a good indicator of economic health. Two things resulted from this: (a) a big ol' book on business cycles and (b) the creation of NBER.

Mitchell was a founder of NBER in 1920 (see Christina Romer's paper here, video version here) and its initial director of research. In that position he continued his search for data and turned NBER into a bustling hub of research into business cycles. In 1929 he published, almost as an aside, his first comprehensive dating of business cycles from 1855 to 1921.

Now, pig iron and freight receipts are all very fine, but why didn't Mitchell use GDP as one of his measures of the business cycle? The answer is simple: Simon Kuznetz, a student of Mitchell's and an economist working at NBER, hadn't invented it yet. It wouldn't be until after World War II that GDP was refined into a useful measure of economic activity.

So this is the story: business cycle dating was basically invented at NBER in the 1920s, and it didn't rely on GDP because GDP didn't exist back then. However, Mitchell was a pragmatist, and he was willing to adopt new economic measures if they turned out to be reliably correlated with other measures of business activity. If we now whisk ourselves to the present day, we'll find that after decades of changes NBER currently uses the following six metrics to date business cycles:

- Real personal income less transfers (PILT)

- Nonfarm payroll employment

- Real personal consumption expenditures

- Manufacturing (wholesale) and trade (retail) sales adjusted for price changes

- Employment as measured by the household survey

- Industrial production

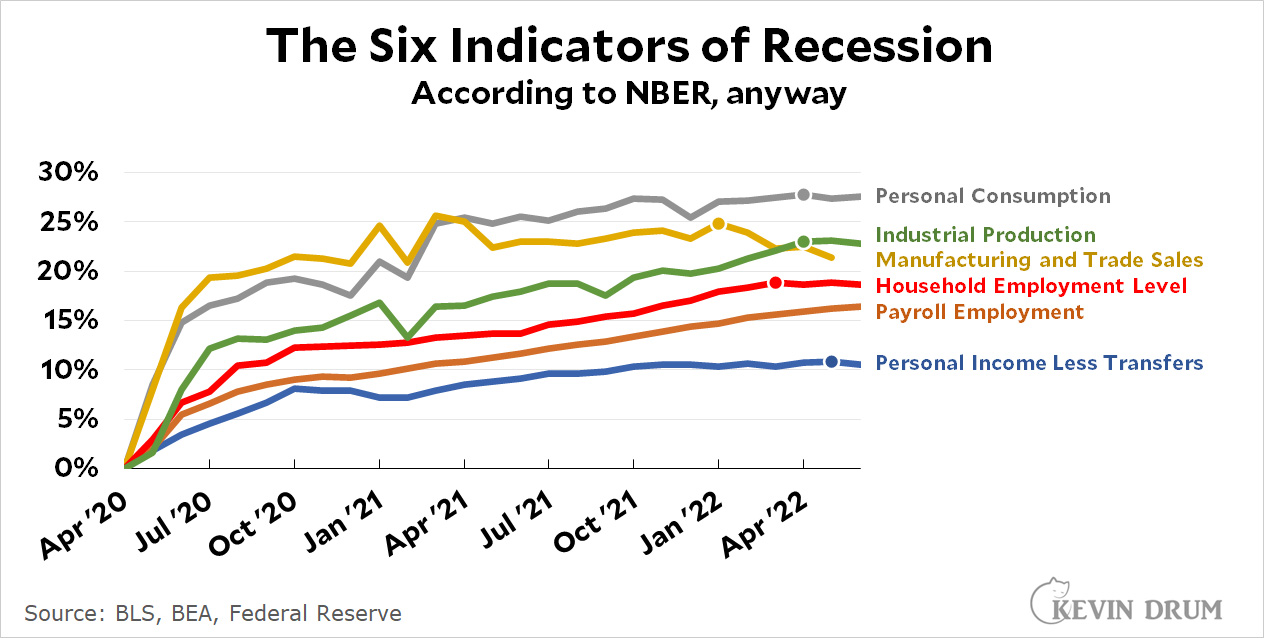

Here's what those six things look like over the past couple of years:

I've placed a marker on each line indicating its recent maximum. Those might also represent the peak of the current business cycle. But it's hard to say, isn't it? Personal consumption is basically flat. Manufacturing and trade sales are on a clear downslope, while industrial production and personal income are just slightly down. Will they tick back upward or keep going down? And payroll employment hasn't peaked at all. It's still heading steadily upward.¹

I've placed a marker on each line indicating its recent maximum. Those might also represent the peak of the current business cycle. But it's hard to say, isn't it? Personal consumption is basically flat. Manufacturing and trade sales are on a clear downslope, while industrial production and personal income are just slightly down. Will they tick back upward or keep going down? And payroll employment hasn't peaked at all. It's still heading steadily upward.¹

There's no reason you can't play this game at home. If you average out the markers, you'd probably figure that the economy peaked and then started to slow around April of this year. Are you willing to make that call? Or . . . maybe it doesn't look entirely clear?

This is why NBER often waits a while to announce when a recession has started. They don't care much about headlines in newspapers or even in recessions per se. This is just a technical exercise of dating business cycles.

And why do we let NBER do this? Because they got there first and developed a solid reputation for doing a good job. I suppose, also, that no one else really wanted to do it.

Nickel summary:

NBER decides on recession dating because they started doing it a long time ago and no one ever tried to take the job away from them.

They've never used GDP as one of their indicators of economic activity. One of the reasons, oddly enough, is that their dating is done by month and GDP is only produced every quarter.²

They currently use the basket of metrics listed above to decide when the economy has reached a peak (end of expansion and start of recession) and a trough (end of recession and start of next expansion).

It takes them a while to announce recession dates because they want to be sure. And the only way to be sure is to have plenty of hindsight to work with.

¹I should add that there's no formula here. The folks who sit on the dating committee are allowed to stare at the numbers until their eyes hurt and then make their own judgments based on whatever heuristic seems best to them.

²This is going to sound crazy, but NBER also dates turning points by quarter. For that, they add real GDP as one of their measures. Or more accurately, an average of GDP and GDI.

It seems truly bizarre to phrase "why do we let them do it" relative to a statistical and econometric excercise. Presumably you have political action objectives in mind - in which case rather simply if you have to have another designation entity.

Although other than bloggers and journos why anyone would particularly care about this from a politial point of view somewhat escapes.

There’s no algorithm. It’s not a ‘statistical and econometric excercise’, it’s judgment calls. Read the Jason Furman post (link courtesy D_Ohrk) if you don’t want to take Kevin’s word for it.

I quote myself 'relative to a statistical and econometric excercise'

The word algorithm does not occur there.

Statistical and econometric excercise =/= algorithm.

I’m on Alice’s side vs. Humpty Dumpty, and I think most readers of the phrase, ‘statistical and econometric excercise [sic]’ would take that to mean a procedure, which any person could follow and arrive at the same conclusion - that is exactly what an algorithm is, but the NBER process is in the end subjective: different analysts may come to different conclusions.

Of course, how readers interpret a sentence or paragraph is an empirically testable question. I have carried out exactly that kind of test multiple times in my career. You could always conduct a survey …

A "statistical and econometric excercise" is just what it says, an excercise for econometricians / economists

That says literally nothing about a "procedure which any person could follow" - which must come from some prejudice of your own as there is nothing in using the phrase econometric above all tht implies vulgarisation for general readership and rather the opposite really.

Even were a "procedure" that general public (rather fantastical idea really given the general innumeracy of the general public, even Uni educated general public, who irrationally blame inflation on Presidents etc) could 'follow' meant, that in no way means an algo.

Good job. But I was sure you were going to push a 1000-word post on this topic out two days ago. Also, a day ago Jason Furman pointed to this: https://bityl.co/DYJY

I find it amusing that several institutions prefer to use monthly data because the quarterly GDP numbers are so often revised later. As though monthly data were noise-free!

I don't think anyone else clicked on that link. LOL.

I guess I have to say it out loud:

The link highlights two sources that explain when and why the notion of 2-consecutive quarters of negative GDP came to be informally known as a recession signal.

The NBER is not itself a government department, so, is it even valid to say they're the arbiters of what "officially" counts as a recession? I thought I had read that the US government indeed relies on this outfit to "officially" determine the start/stop date for recessions. But several moments of googling yield no evidence of this. What is true is that the government pays them for research.

So, as far as I can tell, the NBER is the "official" decider on whether or not we're in a recession only to the extent you accept their judgment. And indeed, if you start researching business cycle history, you'll quickly note recession start/end dates from different sources aren't in perfect agreement. If you prefer the straightforward "two consecutive quarter of GDP shrinkage," feel free to to use that definition. The NBER* is welcome to their opinion, and you're welcome to yours.

*I interviewed with this organization many years ago.

PS: Does any aspect of government policy change if we're determined to "officially" be in a recession? I'm not aware of any. The determination has obvious importance to the media, and from the perspective of politics, but I don't know of any concrete policy changes that occur when we cross the magical Rubicon from expansion to contraction. The most important metrics remain things like the unemployment rate, inflation, mortgage rates, job numbers, and so forth.

More or less my question - the 'official' seems to be one of those empty journo-to-blogger ostentatious declarations that is not with any particular real-world meaning (although for econometric history and analysis of analytical referential utility).

If there is in fact some action truly triggered in government or quasi-government policy, fine, but otherwise....

Agree fully with the P.S. Government policy should be responding to the specific issues that are dragging on the economy and harming large numbers of people, not attempting a ‘one-size-fits-all’ solution. So it’s important to get into the details, not just yell ‘Inflation!’

I have the same job I’ve had for many years and there is no chance I’ll get laid off. No recession for me.

Meanwhile - I know Mr. Drum doesn’t really write about this sort of thing but it shows the danger of this creeping police state. What do you do when the police are the enemy?

https://www.reuters.com/investigates/special-report/usa-elections-michigan-investigation/

Oh well. Good luck.

Here’s another good story. If a recession means that all this junk never gets made, then I’m all for if.

https://www.nytimes.com/2022/07/30/business/retail-returns-liquidation.html

Are we to believe that Wally O'Dell would allow his patented GQP-pumping vote-flip method in touchscreen voting technology to be perverted to elect Democrat grandpaedophile joebiden over Republican American muscle daddy Donald Trump?

This is preposterous. & a gross libel of Walden O.

ACAB in Barry county. Whack him. ????

If I understand the argument here, "we" have never delineated recessions by the two consecutive quarters rule, and as evidence you cite the fact that NBER doesn't use that rule, relying instead on bureaucrat vibes. This is quite a circular argument.

Yes, we all know that NBER uses vibes. But the two quarters rule has existed for decades as one can verify with a quick glance at any number of old economics texts. It has the benefit of being objective while usually providing results in line with observers' intuitive sense.

Econ 101 textbooks =/= actual econometrics as applied by working economists.

As a rule of thumb for general observation it is of course practical and pragmatic, if one is keeping in mind rules of thumb are not to be erected as something more than an observational short-cut.

So, calling recessions is like naming generic drugs. There's a low profile committee that makes the call. For drugs, it's Stephanie Shubat and Gail Karet of the United States Adopted Names Program at the American Medical Association, just in case you were curious.

I've also been reading that the GDP blip is largely due to inventories. Businesses loaded up on too much stuff to sell just as people started to go out. So GDP jump at end of last year, dip beginning of this year.

Still having supply chain issues--see new car sales. So lower GDP, but not because people don't want to nor are unable to buy...

A few days ago, I read that 1947 looked similar to our current economy. There were 2 quarters of GDP contraction, high inflation, but also low unemployment and fast job growth. No recession was declared that year, but there was a mild recession declared in 1949.

Bring on the Spirit Animals!

I mean the Animal Spirits!

https://youtu.be/d0nERTFo-Sk

Still the best rap battle in history.

Russia stealing planeloads of gold from Sudan,

https://www.cnn.com/2022/07/29/africa/sudan-russia-gold-investigation-cmd-intl/index.html

Sudan = Sudetenland = Crypto-German Nationalists = Nazis. Prolly a connection to Leni Riefenstahl's postwar photography career, too.

Putin's Army is just denazifying the Islamofascist Khartoum Republic of Blackest Afrikans the same way they are denazifying the ((( Zelenskyy ))) Kyiv Fascist State

Interesting that Honda auto production idled in June. Now it's starting to reboost with Honda announcing 7 day weeks for some plants in August. Probably moving to frame plants by September.

Pingback: Has the US economy really been shrinking? – Kevin Drum