A lot of people are becoming instant experts this weekend on the subject of deposit insurance, including the question of what to do if you have cash in excess of the $250,000 FDIC limit.

There are ways to deal with this, including (obviously) opening multiple bank accounts. But that's not really the answer. The real answer is that people and corporations with lots of cash don't keep it in a bank account in the first place. They invest it.

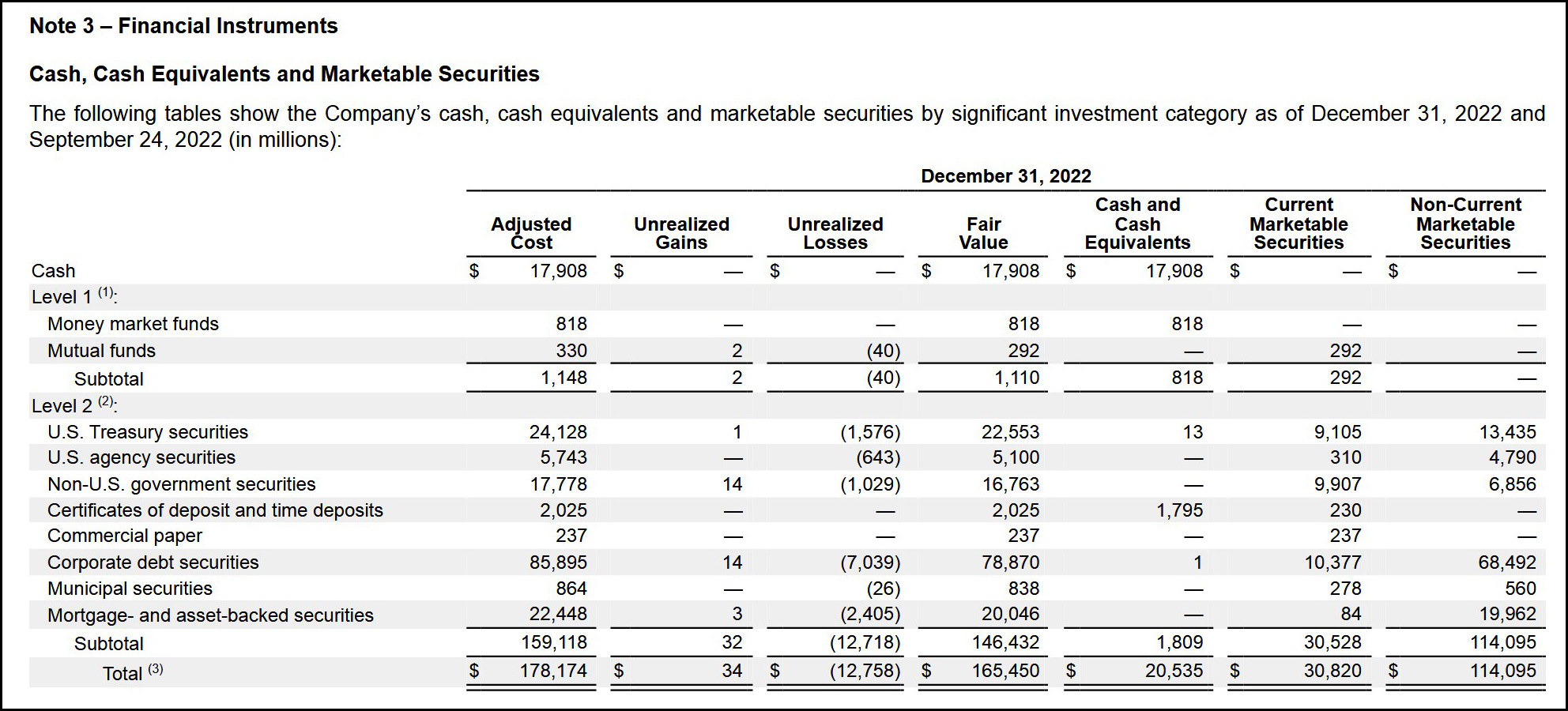

Apple Corp., for example, famously has nearly $200 billion in "cash"—i.e., undistributed profits. Here's where that money is held:

As you can see, 90% of their $178 billion is held in mutual funds, treasurys, commercial paper, etc. And this is true of all corporations big enough to have substantial amounts of cash. They put it to work, while keeping around only enough to fund routine daily operations.

So Apple has "only" about $18 billion in actual cash (or equivalents). I don't know what they do with it, but there are plenty of fairly simple options for making sure it's safe, the most obvious of which is to keep it in multiple accounts at multiple banks.

This is corporate finance 101 and it's what large depositors at Silicon Valley Bank have done. That is, it's what they've done unless their CFOs are idiots, in which case they deserve to take a bath just as a way of teaching them a lesson.

Beyond that, SVB may be in receivership now, but that doesn't mean it lost everything. In fact, it was pretty well capitalized and its remaining assets are probably enough to cover something like 90-100% of their deposits. So folks with large amounts of money in SVB will almost certainly be made whole, or very close to it.

And beyond even that, the FDIC will make a large share of deposits (probably 50% or more) available at start of business on Monday. This is enough for everyone to make payroll, buy more paperclips, and so forth. So to summarize:

- Most companies have only a modest portion of their "cash" in actual cash.

- To protect the actual cash, most companies spread it out in various ways.

- Of the ones who (inexplicably) don't do either of these things, they'll have access to half their money tomorrow morning.

- And, more than likely, they'll get 90% or more of it back within a few weeks.

If the entire banking system were in some kind of systemic trouble, as in 1997 or 2008, that would be one thing. But it's not—or at least, it doesn't seem to be.¹ This is just a single bank failure, and it's likely that virtually no one will lose more than a small amount of money.

So calm down.

¹And if it is, we have way bigger things to worry about than SVB.

This says it all: https://www.reddit.com/r/wallstreetbets/comments/11omavh/here_we_go_again/?ref=share&ref_source=embed&utm_content=media&utm_medium=post_embed&utm_name=84f971968879480097b82ebaf1f5cd52&utm_source=embedly&utm_term=11omavh

Google paid 99 dollars an hour on the internet. Everything I did was basic Οnline w0rk from comfort at hΟme for 5-7 hours per day that I g0t from this office I f0und over the web and they paid me 100 dollars each hour. For more details

visit this article... https://createmaxwealth.blogspot.com

Notably as particulalry a large number of Silicon Valley VC firms have signed public statement to recommence with SVB with new buyer

(https://www.cnbc.com/2023/03/12/hundreds-of-vcs-vow-to-work-with-svb-again-if-new-owner-found.html)

Of course non-binding statements are worth at one level the paper or electrons they are made up of, on other hand as Drum has noted the broad fundamentals on SVB financing business appear to be broadly acceptable and a specialist buyer (one might hypothesize a private equity consortium interested in picking up SVB at a subsidised fire-sale price)

I was just reading on TPM that hedge funds are approaching depositors to give them 60 to 80 cents on the dollar for their deposits at SVB. As TPM noted, that means the expected return would be higher than that.

https://talkingpointsmemo.com/edblog/how-to-think-about-the-silicon-valley-bank-collapse

The Hedgies offer is indeed indicative. While Talking Points Memo comment is not particularly insightul on SVB itself (fair eough, not a financial blog I see) the offer on deposits for quick liquidity is highly indicative of the chances of not only orderly resolutoin but under right circumstances revival.

Arguably a backing to enable an acquisition and avoid liquidation will be less overall costly to the public, although the Libertarians hypocrisy merits being rubbed deeply in their faces.

Sure, but a lot of the panicky talk has been to the effect that the banking system is in mortal danger if the depositors get anything less than 100 cents on the dollar. It's absurd and maybe just this once they should take a haircut so future depositors put a little thought and effort into basic corporate finance.

SVB share holders (not account holders) will lose a lot of money. If it's just a garden variety bank run, some cash-rich enterprise like Berkshire Hathaway will swoop in and pick up SVB's business on the cheap.

Crypto stable coins:

"Circle announced on Friday that $3.3bn of its $40bn of USDC reserves are held at collapsed lender Silicon Valley Bank."

https://www.theguardian.com/technology/2023/mar/11/usd-coin-depeg-silicon-valley-bank-collapse.

At least the reserves were distributed.

Sadly I lost track of a tweet I saw earlier, but it said there is a standard mechanism for large entities to automatically spit their accounts to keep them below the $250k max. Hope to see some detail if true not, not sure what the value of cutting this safety feature would net for SVB.

Reliance on Twitter as always is a bad idea. Regulators look at beneficial ownership, not simply single accounts, at the institution in question.

Corporate CFOs with signficant balances distribute balances across several institutions to manage exposure risks. And of course also monitor - that's what makes Jumbo corporate deposits (i.e. over insurance limits) risky from a liquidity perspective, they run fast.

Finally shook the memory lose after more coffee, it was from a thread from David Dayen who included the link to the service in question known as an Insured Cash Sweep,

"It essentially cuts up your large account if you're a business into insured pieces, $250k each. In the event of a run, those deposits over the limit are safe."

https://twitter.com/ddayen/status/1634925784271036417

The FDIC deals with insolvent banks all the time. The difference here is that it's a relatively big bank, and that the depositors are mostly in one prominent line of business and are mounting a full-scale panic in the media. Which the media are happily running with-- it's a big story involving a publicity-hungry business sector, and it draws eyeballs.

I've read the same TPM writeup golack mentions and a few other things too, and underneath it all, it seems like SVB made a lot of questionable moves as the deposits poured in so that its ability to cover accelerated withdrawals mostly depended on interest rates not rising at all (apparently they put a lot of it into 3-year treasuries). But rates did go up, and pretty swiftly, iirc (and as most of the smart money was anticipating).

Because of these and other possibly boneheaded moves, I think it's likely that potential buyers need more than day or two to figure out what SVB really has to its name. A buyer with time and its own asset base, as Josh Marshall puts it, can wait until the treasuries mature and get their full value while keeping depositors liquid. But a buyer needs to be able to figure out what the rest of the stuff on SVB's books is worth, and that could take a few more days. Meanwhile the FDIC has things in hand.

The schadenfreude is the good part for a statist lib like me, I have to say. Raging libertarians, who demand to be untrammeled masters of all our fates, suddenly running in circles and screaming all wild-eyed for Uncle to bail them out, what could be a better show? It'll be hard for the Oscars to top this.

Supposedly 90-95% of SVC's deposits were uninsured. So far the FDIC has only said that the insured deposits will be immediately available. Probably a lot of firms will be scrambling to get the money they need. If they didn't need it on short notice it wouldn't be deposited in the bank.

I'm not so sure about that last point, honestly. Apparently Thiel and other start-up angel VCs were telling their fundees to put all the money there, and they kind of felt obliged to.

Also, it's hard for me to see a tech start-up directing much effort toward actively managing the money they've been fronted in any sophisticated way for maximal safety and return. Particularly not in a spectacularly low-interest-rate environment. Imagine trying to justify a high-priced CFO, or spending a lot of time on financial management, to your biggest and probably only backer, the one who's explicitly told you just to park it in SVB and run it down as needed.

Some reading from Delong: https://braddelong.substack.com/p/reading-now-why-did-joe-biden-pick?utm_source=post-email-title&publication_id=47874&post_id=107963070&isFreemail=true&utm_medium=email&fbclid=IwAR3HjFYJ9aFZWCpFd0gmsX1kY3HRaFNEX0C51q1-D17xMS0I_L5tdeIVgzM

Unfortunately, lots of media pundits have been busting for an opportunity to bray that they were right all along, this is Jimmy Carter's second term, and the economy is as terrible as they always said it was. Along with the market gamblers trying to drive down stock prices so they can make a killing, they may well succeed in creating a wholly baseless financial panic.

And of course Republicans are waiting in the wings with threats to default on US debt, confident most of the subsequent chaos would be blamed on Joe Biden.

Gee, if only there were some kind of regulation that required small banks to keep a certain % of cash on hand.

Oh, wait, there is (Dodd-Frank), except that the Trump admin raised the limit at which a bank is considered "systemically important," so SVB was no longer under the same scrutiny than it had been.

That's no guarantee that SVB would've survived this good ol' fashioned bank run, but they might've had a better chance.

Bbbut, the CEO lobbied! https://www.motherjones.com/politics/2023/03/silicon-valley-bank-greg-becker-dodd-frank/

The article however doesn’t say which specific risk assessment the bank would not have passed were it included.

Definitely time to panic, according to nut job Home Depot founder, as reported by the usually (always?) unreliable Daily Mail: https://www.dailymail.co.uk/news/article-11849277/Home-Depot-founder-Bernie-Marcus-warns-Americans-wake-woke-Silicon-Valley-Bank-goes-bust.html

I am really hoping to see a bunch of these start-ups and venture capitalists go under. Signature bank bites the dust. ???? who’s next?

Woke culture didn't force SVB to invest in long Treasury bonds with the huge piles of cash coming in from high tech start-up VC fundings, and didn't force big depositors to park huge sums of uninsured / undiversified cash in the bank. The start-up VC world may pay lip service to diversity and inclusion, but its all about pure dog eat dog capitalism at its core.

These folks at SVB simply fucked up big time, and I don't think Dodd Frank or Glass Stengel would have mattered, since on the surface, they did what traditional banks are suppose to do. If half of their security investments were in short term, liquid, investment grade instruments, they would not be insolvent today.

FYI, the FDIC just bailed out all the SVB and Signature Bank depositors.

FDIC is clearly afraid of national bank runs.

While true that people ought to keep their accounts under $250K, I want to remind you that if your bank gets seized and all assets frozen, if you live through your debit card rather than a credit card, your life is frozen for a little bit.

Comparing the finances of Apple and a startup doesn't make any sense. Apple has a huge positive cash flow from its business operations and lot of money in reserve. Startups typically get a round of investment money that is expected to fund their development for a year or more. They don't have positive cash flow from business operations, so they have to bank that money in a relatively liquid form so that it is available to meet payrolls and other operating expenses.

The right thing to do is to set up a Treasury ladder with varying maturities. Since a lot of expenses are predictable, they could have a set of bonds redeem in time to meet payroll, rent, hosting, license and other expense. It's a bit of a hassle, but it's pretty standard stuff. You could do it online yourself if you wanted to.

An alternative is to have a sweep account that buys CDs at various banks around the country using available cash at regular intervals. One of my brokerage accounts does this automatically.

Personally, I'd like to see the bank fail and a lot of the money vanish. It has been rather obvious since Biden's election that the Fed was eager to find an excuse to crush the working economy as part of its mandate to prevent meaningful economic growth. For decades, we've been defunding the police and repeatedly having to bail out industry after industry. A proper bank failure with actual consequences would remind people of why we hired those police in the first place.

Unfortunately, I expect everyone to be bailed out, then I expect that the VCs will winnow their investment lists so that a lot of startups that might have survived close down and lay everyone off. That way, we get the worst of both worlds. Wealthy incompetents avoid the consequences of their own stupidity, while people who have to work for a living get trashed by powers they have been taught are beyond their control.

I liked Altoid’s self-description of ‘statist lib’, that’s me, too. I think after national defense and public infrastructure, a principal responsibility of modern democratic government is insurer of last resort for the 90+ percent for whom events beyond their control might mean bankruptcy, foreclosure, eviction, repossessions, and other dire circumstances - events like layoffs, serious illness, family emergencies. So, yeah, the fat cats should be forced to wait to buy that second yacht, while the working folk are assured a roof over their heads, food on the household table, health care, and the rest of the essentials.

For Apple to keep $18bn in separately insurable cash accounts they would need 72,000 accounts. Managing that would be a nightmare. I'd bet they have decided to split it into a handful of different banks and that the risk of 2% of their cash on hand is acceptable.