Matt Darling is puzzled:

"In recent years, however, homeownership has become unavailable to more people than ever before, including white-collar workers and even members of the managerial classes."

??? https://t.co/jmByEZ0eXt pic.twitter.com/XVpsjhyAjK

— Matt Darling ????????️ (@besttrousers) October 18, 2023

It's true that the overall homeownership rate hasn't changed much recently, which might cause you to think that people are still buying homes as much as ever. But you'd be wrong. Homeownership rates have a ton of inertia built in because nearly all the people who owned homes a few years ago still own homes today. Even if homes are getting expensive and fewer new buyers can afford them, it takes a long time to show up in the homeownership rate. So instead, take a look directly at purchases of new homes:

After plummeting during the housing bust, purchases of new homes steadily increased back to their long-term average and then started to drop beginning in 2021. Here's why:

After plummeting during the housing bust, purchases of new homes steadily increased back to their long-term average and then started to drop beginning in 2021. Here's why:

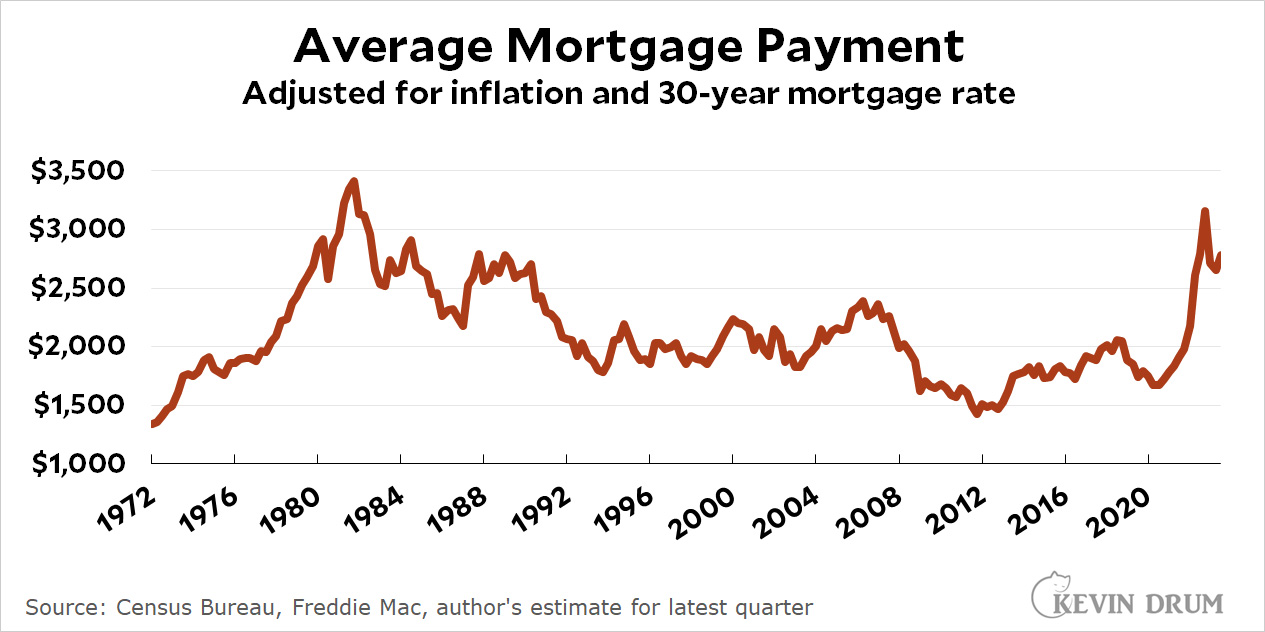

Due to higher home prices and higher interest rates, the cost of the median home mortgage skyrocketed starting in 2021.

Due to higher home prices and higher interest rates, the cost of the median home mortgage skyrocketed starting in 2021.

So, yeah, new homes have become less affordable over the past couple of years. You need to earn pretty good money to afford an annual nut of ~$32,000. A few years ago an income of $70,000 was enough to afford a median home. Today it's more like $115,000.

Some special cases in SJ California.

In my old neighborhood off Winchester Blvd between Payne and Williams Zillow posts prices of $2m+. Just ordinary post war 2 and Korean vintage. My house was owner built in 1949.

It isn’t the structure so much as the land in which it sits. Last time I looked at my assessment in Sunnyvale, 80% was land.

It isn’t the structure so much as the land in which it sits

It's a mutually reinforcing feedback loop. In the parallel universe where people were allowed to build as many housing units as the market could absorb (which in areas like SF Bay would include a lot more MFH), that limited land could host a vastly larger number of dwellings.

Indeed, I'd guess one factor driving up land values in places like California is the artificially large quantity required per unit of housing. Buildable units of land, in other words, are artificially scarce.

But yes, land is obviously intrinsically scarcer than building materials, which can be produced in factories.

Yes, if only we had the population density of Manhattan, all would be well…

Yeah, I ran the numbers early last year before rates started going up. If I could find a condo in the $300K range it would be about $1200 all up (principal, interest, taxes, insurance and HOA fees). I found one that looked good for me recently which was $325K. It seemed nice, recently updated, with plenty of storage. I ran the numbers and it was $2K. I'm currently at about $1K for rent and planning to retire soon, so nein danke. I could swing the more or less constant $1200 with slow annual increases in exchange for an uncertain future in a rental. But I've been in my rental for more than 20 years.

I get the point of using mortgage payments, but I think a more telling figure is the median sales price and the median price per square foot: https://fred.stlouisfed.org/graph/?g=1aksX

The two in conjunction feels like a better indicator than "average" mortgage payments.

Something like 65% to 70+% of home purchases are made with a mortgage.

When interest rates are changing (up or down), the purchase price fails to provide an accurate picture of the actual cost facing a buyer and fails to explain changes in the number of homes purchased. Median sales price is much less important than the actual costs (monthly payments) faced by 65-70% of buyers, but it is a useful piece of data.

How so?

Average mortgage payments might or might not include (a) PMI, (b) withheld property taxes, (c) points, (d) different periods of mortgages, (e) variable/fixed/balloon rates, (f) fees, (g) and allowances.

Additionally, tracking average mortgage payments will inherently bias towards large, expensive homes.

Yes, median is better than average.....i actually think Kevins chart might be mislabeled, i believe it should median if he is using the census data. But there isnt a huge difference, we really dont see 20 million dollar mortgages for high end property.

Capturing the actual cost of the housing payment is more important than the sales price of the house for most discussions on this topic. Most buyers really only care about their payments.

Buyers may not actually care too much about future payments or even present payments. A lot of people got in over their heads during the 2006 bubble.

Lenders decide how much they will lend depending mostly on income. And if lenders aren't regulated they will also go wild, selling off mortgages to be bundled.

Anything is possible!

But its more likely that buyers care very much about current costs, future costs and the potential future income opportunities associated with those costs.

current costs going up based on potential future income and costs going up based on higher financing costs seem like very different things....and buyers appear to reacting very differently to these very different scenarios.

But remember everyone, that payments are actually down a bit lately: https://jabberwocking.com/average-mortgages-are-actually-down-a-bit-lately/

Yeah, I'm struggling to square this with prior posts. Is he changing his mind? I don't believe it.

Payments are still up compared to the last few decades, but they have come down a bit over the last several months.

Whats the confusion?

Things are getting better.

(Those same) things are getting worse.

…

Things are worse than they were in years past but they are better than they were a few months ago.

This isnt at all confusing or contradictory. Im going to assume trolling.

That Kevin is posting saying one thing, then posting something else that contradicts his first (adamantly-held) point that is part of his larger narratives without acknowledging that.

Sidney Powell to plead guilty in exchange for the most trivial possible sentence,

https://www.rawstory.com/sidney-powell-guilty-plea/

Pingback: Home sales drop to lowest rate in over a decade – Kevin Drum