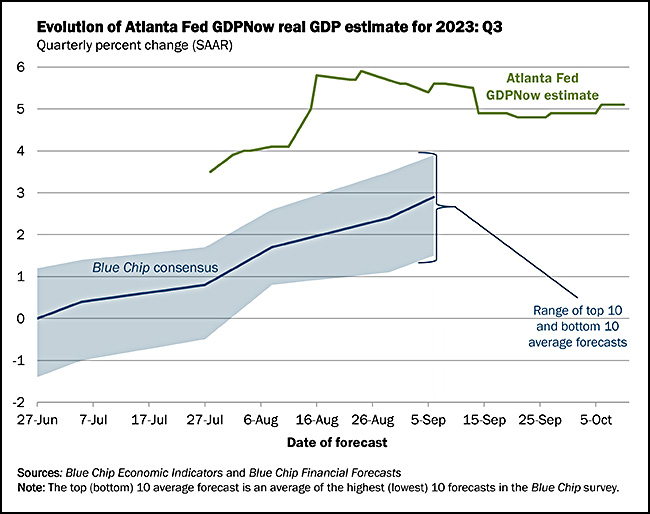

The Atlanta Fed's GDPNow forecast continues to suggest that the economy was red hot in Q3:

Their forecast of 5.1% growth is largely based on increases in consumer spending (2.5%) and net exports (1%). Those subcomponents are indeed looking good so far:

Their forecast of 5.1% growth is largely based on increases in consumer spending (2.5%) and net exports (1%). Those subcomponents are indeed looking good so far:

The trade deficit is on track to be $20+ billion better than in Q2, while PCE jumped in July and has stayed on a higher track since then. That 5.1% growth forecast is still a little hard to believe, though, and the New York Fed agrees:

The trade deficit is on track to be $20+ billion better than in Q2, while PCE jumped in July and has stayed on a higher track since then. That 5.1% growth forecast is still a little hard to believe, though, and the New York Fed agrees:

Both of these forecasts have reasonably good track records, so it's odd that they're in such sharp disagreement. The New York Fed doesn't put the Atlanta Fed's forecast even within the outer bounds of probability.

Both of these forecasts have reasonably good track records, so it's odd that they're in such sharp disagreement. The New York Fed doesn't put the Atlanta Fed's forecast even within the outer bounds of probability.

The BEA's first official estimate of third quarter GDP will be released in a couple of weeks, on October 26. We'll find out then who's right.

It is odd that the forecasts differ by so much. I expect economic modellers to be very interested because they are about to learn something very interesting.

Of course, it could just be a dumb bug in the Atlanta model. But it would have to be one that hasn't shown up before, so there is clearly something unusual about the quarter.

Is that growth or annual growth rate? Annual growth rate of 5.1% for a quarter is high but not unbelievable. An actual increase of 5.1% in a quarter is so high as to be unbelievable.

Those outer bounds of probability in the New York Fed's forecast cover only a 68% probability range. So it's not at all a long shot, in their estimation, that the eventually reported GDP is outside that range. If they're assuming a normal distribution and they showed us the 95% probability range, it would extend up to 5.5%. You could still think the Atlanta model is off, but it isn't that hard to fit it into the uncertain picture described by the New York model.