This is a picture I took in the Tuileries in Paris. In France, even the pigeons are elegant looking creatures.

Cats, charts, and politics

This is a picture I took in the Tuileries in Paris. In France, even the pigeons are elegant looking creatures.

I made this chart for an odd reason and didn't end up using it for anything. But as long as I made it, I might as well share it. Isn't that the kind of stochastic¹ mind dump that blogging is famous for?

¹Fancy word for "random."

House Judiciary Chairman Jim Jordan sent a letter Monday to IRS Commissioner Daniel Werfel and Treasury Secretary Janet Yellen seeking an explanation for why journalist Matt Taibbi received an unannounced home visit from an IRS agent.

....The bigger question is when did the IRS start to dispatch agents for surprise house calls?...The curious timing of this visit, on the heels of the FTC demand that Twitter turn over names of journalists, raises questions about potential intimidation, and Mr. Jordan is right to want to see documents and communications relating to the Taibbi visit.

The fear of many Americans is that, flush with its new $80 billion in funding from Congress, the IRS will unleash its fearsome power against political opponents. Mr. Taibbi deserves to know why the agency decided to pursue him with a very strange house call.

Did you guess that this is a Wall Street Journal editorial? Huh? Did you?

Michael Barr, the Fed’s vice chair for supervision, testified before Congress this morning about the failure of Silicon Valley Bank:

SVB was flagged in a presentation to the Federal Reserve Board on the risks created by rising interest rates weeks before its stunning March 10 collapse....“Staff relayed that they were actively engaged with SVB but, as it turned out, the full extent of the bank’s vulnerability was not apparent until the unexpected bank run on March 9,” Barr said. “SVB’s failure is a textbook case of mismanagement.”

This is ridiculous. SVB was "flagged" in a presentation "weeks before" its collapse? That's infinitely too late to have any impact. What's more, Barr says that SVB's vulnerability "was not apparent" until the bank run actually began.

In what way is this a textbook case of mismanagement? Regulators, who were fully aware of the basics all along, issued a tepid warning a few weeks ahead of time and never raised any serious red flags. If that's the Fed's response to a "textbook" case of bank mismanagement, they might as well hang up their spurs.

I'm wide open to being proved wrong about this, but today's testimony does nothing but strengthen my belief that, in fact, there was nothing all that seriously wrong with SVB. They were plenty solvent and exceeded all the normal capital and leverage requirements—something that would have been true even if they were governed by pre-2018 rules. Basically, the regulations were fine and the regulators were fine.

In the end, SVB was hurt by a slowdown in the tech startup market, and then demolished by a sudden panic within the tech community. An investigation of what caused the panic ought to be everyone's top priority.

From the LA Times this morning:

Three inmates died in Los Angeles County jails in just over a week

Three Los Angeles County inmates died in an nine-day period this month, according to the Los Angeles County Sheriff’s Department, a grim milestone.

....To people paying close attention to the county’s lockups, the cluster of deaths did not come as a surprise. “Because the jails are operating 20% over capacity, we’re going to continue to see people dying,” said Melissa Camacho, a senior staff attorney with the American Civil Liberties Union of Southern California.

Here's the 8th paragraph:

Los Angeles jails are on track to see fewer deaths this year than last, though incomplete information makes it difficult to draw conclusions about why. Seven people have died behind bars this year; records show the jails had seen 11 deaths by this point last year.

To people who pay even passing attention to statistics, the cluster of deaths also did not come as a surprise. That's just how random events happen. The real question here is why the LA Times tried to imply in its headline that jail deaths were up when, in fact, they're down 37% so far this year.

A few years ago the good people of Kentucky elected a Democrat governor. That's bad enough, but with Mitch McConnell in the hospital Republicans are now in a positive tizzy. They're afraid that McConnell might die or have to retire, leaving the governor free to appoint a Democrat to fill out his term.

Naturally this can't be allowed, even though it's been the practice in Kentucky for the past century. So the Republican legislature passed a law saying the governor has to choose a replacement of the same political party as the departing senator. Sherrilyn Ifill thinks this is corrupt, but over at National Review Charles Cooke says she's nuts:

So, a veto-proof supermajority within the elected Kentucky legislature passed a law that requires the state’s governor to choose an interim senator from the same party as the guy who was elected last time around, and this is an “attack on our democracy” that “makes voting irrelevant”?

This is profoundly ridiculous. Again: with an apparently straight face, Ifill is arguing that it is more democratic to empower just one of Kentucky’s elected officials to choose a temporary federal senator than it is for a supermajority within the elected state legislature....(You will be shocked to learn that Ifill makes no mention of the fact that the change Kentucky has made is already the law in a handful of other states, including in Hawaii and Maryland, where it presumably serves to “maintain perpetual Democratic political power.”)

I should hardly need to say this, but no one is arguing that one method is any better than the other in theory. What Ifill and others are complaining about is the Republican habit of playing Calvinball with this stuff. In Wisconsin, when a Democrat was elected governor, Republican governor Scott Walker had the gall to sign a bill taking away powers he himself had exercised for eight years. When Virginia became a state friendly to Democratic presidential candidates, Republicans tried to get rid of the winner-take-all system for electoral votes that they had been fine with since the beginning of the Republic. And of course, in the Senate Republicans routinely change the rules for judicial appointments depending on which party holds the White House.

This is Calvinball. There are lots of different rules that are fine in theory, but there's no excuse for changing them just because the opposing party wins an election. That's what we're complaining about.

Today the Washington Post asks, "Why Americans are so pessimistic about their finances?"

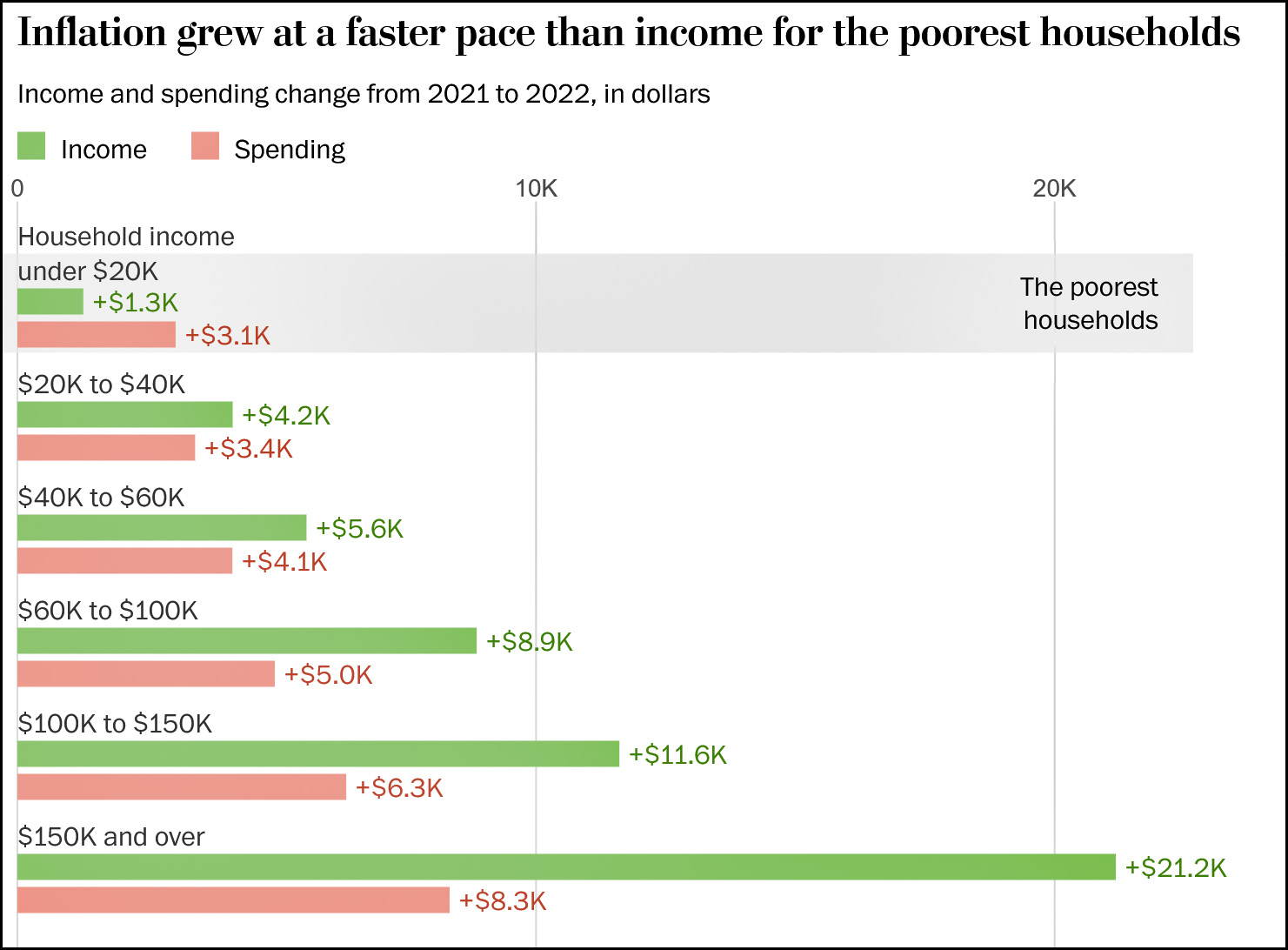

After presenting three stories of families at different income levels, their conclusion is that the price of eggs is up. Unfortunately, their data doesn't really back this up, since household income has increased more than spending. So they take a different tack, warning that percentage increases are misleading. Instead, they ask us to focus on raw dollar increases:

This doesn't work either. Except for the very poorest families, income has increased more than spending even in dollar terms. And low-income families are something of a special case because they rely so heavily on government benefits, which declined in 2022 after the temporary bumps of the COVID years.

This doesn't work either. Except for the very poorest families, income has increased more than spending even in dollar terms. And low-income families are something of a special case because they rely so heavily on government benefits, which declined in 2022 after the temporary bumps of the COVID years.

So this doesn't explain widespread pessimism about personal finances either, which means we have to invent something else:

Even these calculations don’t capture the full experience of what it’s felt like to live among so much economic uncertainty the past couple of years. Americans are frustrated by rising costs, yes. But they’re also frustrated by how much more attention they must pay to these rising costs — attention that is itself costly. This hidden strain on families is likely to continue for some time, even if some headline economic measures continue to improve.

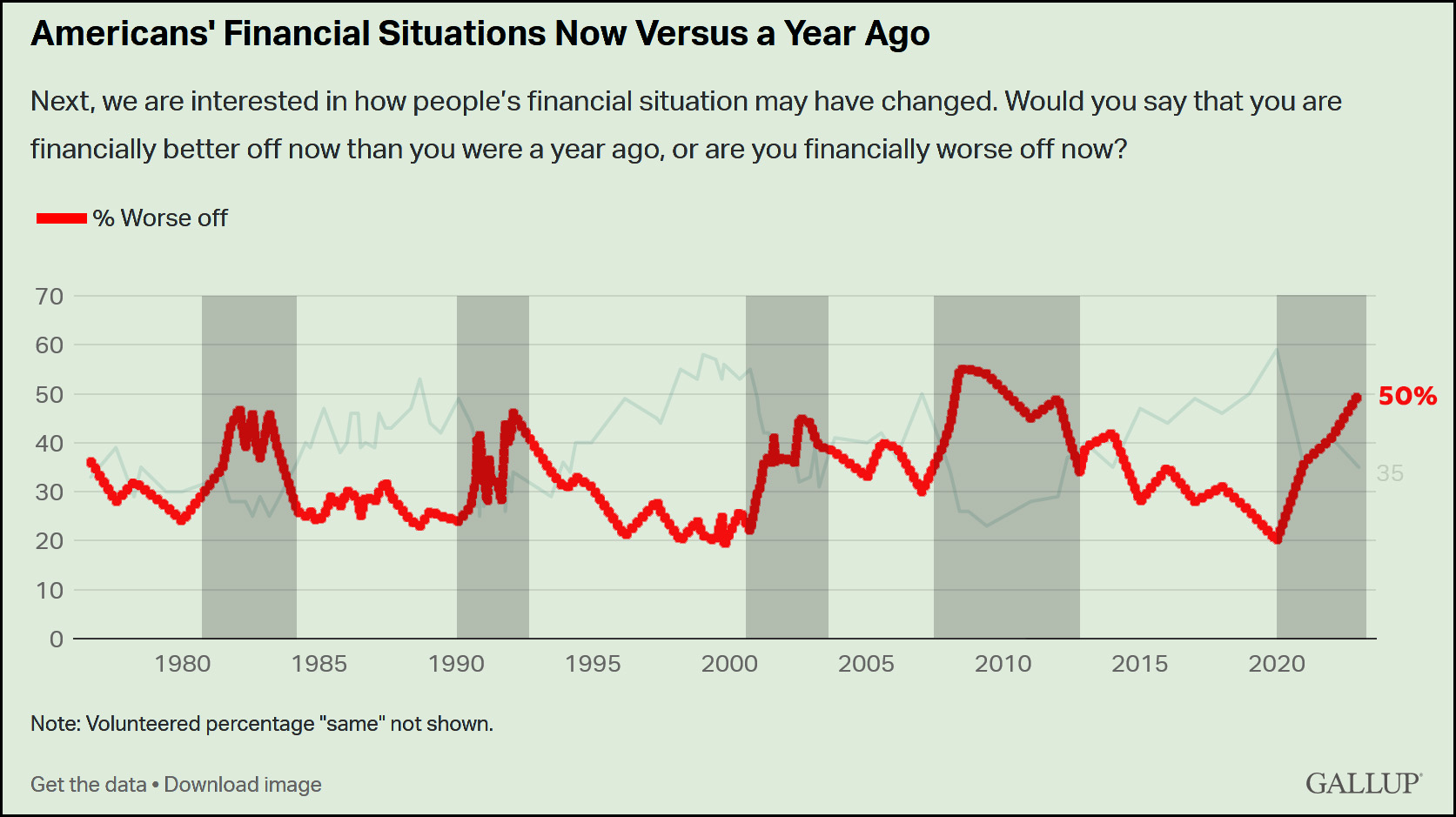

It's the mental strain of inflation that turns out to be the culprit! And you know, maybe so, although it seems like a bit of a stretch. Take a look at the long-term Gallup data that sparked this conversation in the first place:

During each recession and its immediate aftermath (the gray areas) anxiety about finances went up, and in 2021 Americans started to treat COVID like a recession. This is before inflation spiked up, so that can hardly be the cause. The primary answer, I suspect, is simpler:

During each recession and its immediate aftermath (the gray areas) anxiety about finances went up, and in 2021 Americans started to treat COVID like a recession. This is before inflation spiked up, so that can hardly be the cause. The primary answer, I suspect, is simpler:

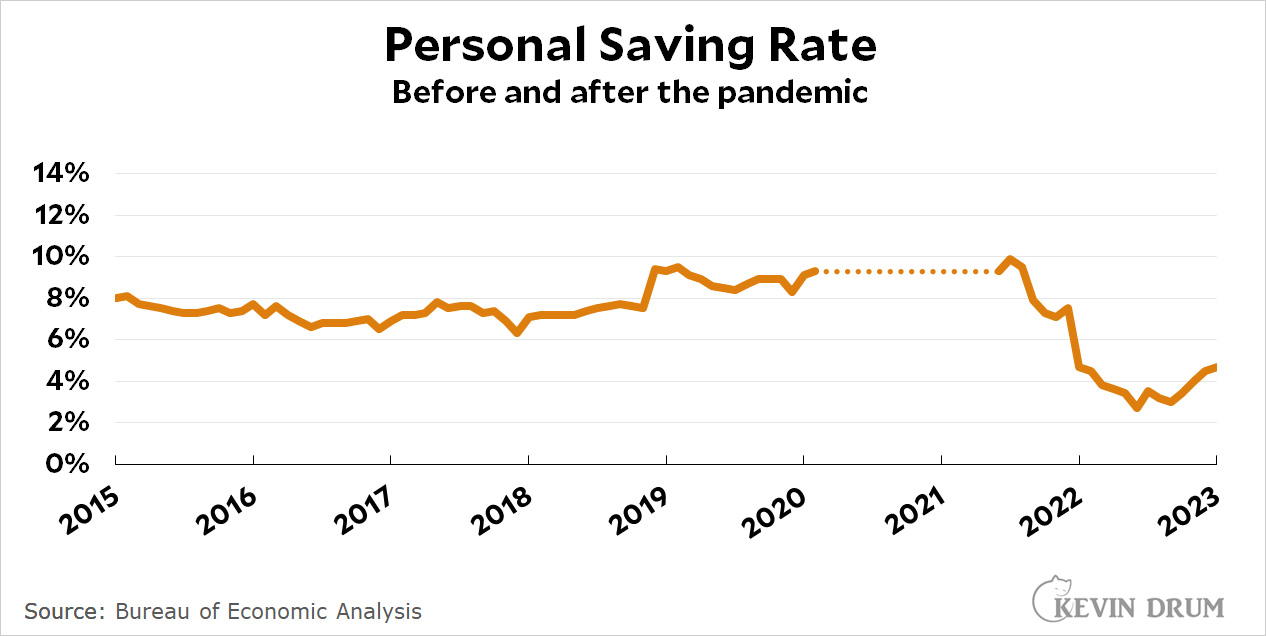

Before the pandemic, people were saving about 8% of their income. That made them feel safe. During the pandemic, they were socking away huge amounts thanks to government checks, and that made them feel safe even in the midst of hard times.

Before the pandemic, people were saving about 8% of their income. That made them feel safe. During the pandemic, they were socking away huge amounts thanks to government checks, and that made them feel safe even in the midst of hard times.

But then the government checks stopped and people started using up their savings. They did this throughout all of 2021 and kept doing it through the first half of 2022, ending up at a saving rate of around 3%. This makes them feel decidedly unsafe regardless of their income or their actual amount of savings.

As an explanation of financial distress this makes more sense than trying to torture the inflation statistics to tell a story they don't really want to tell. Incomes are in decent shape; employment is strong; and life is mostly back to normal after the pandemic. However, savings are being spent down instead of being replenished, and this makes a lot of people feel like they're on the edge of disaster, where any single blow could wreck their finances completely.

So, in order, the proximate causes of financial anxiety are (1) COVID, (2) declining savings, and (3) inflation. There's no question that inflation, especially of high profile items like food and gasoline, takes a toll, but it's really not the main problem here.

I went out to the desert on Friday to do some astronomy, but in order to avoid traffic I left the house early and took the scenic route. In Banning I turned off the interstate and took Highway 243 up to Idyllwild and then back down to Indio.

By the time I got to the desert the wind was picking up and it wasn't a great photography night. Plus there was some kind of software error that ruined a bunch of images. I'll try again next month.

But the scenic route did produce some nice ordinary photographs. We'll start with two views of Mt. San Gorgonio taken from different spots in Banning. There will be plenty more later.

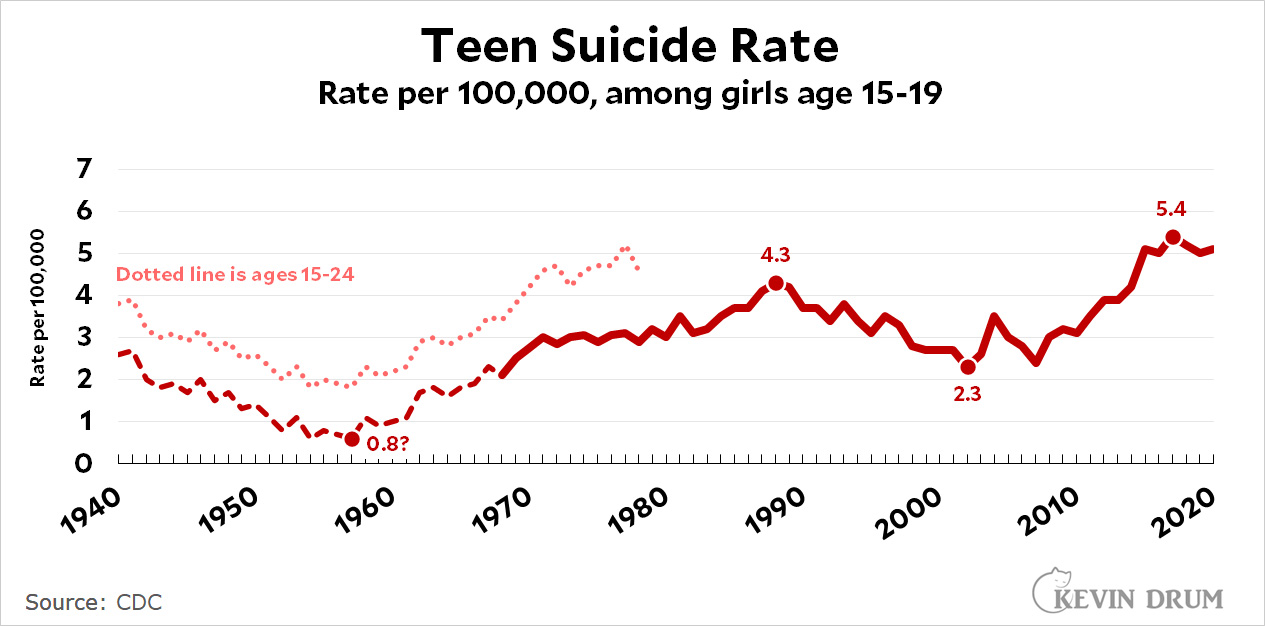

Here is the suicide rate among teen girls age 15-19 going back to 1940. Values before 1968 are estimated from the age 15-24 suicide rate.

The suicide rate:

The suicide rate:

NOTE: Dotted line data (1940-1978) is in HIST290_4049, HIST290_5059, HIST290_6067, and HIST290_6878 here. Solid line data (1968-1978) is here. Solid line data (1979-1998) is in HIST002R_1 here. Solid line data (1999-2020) is from the CDC WONDER database.

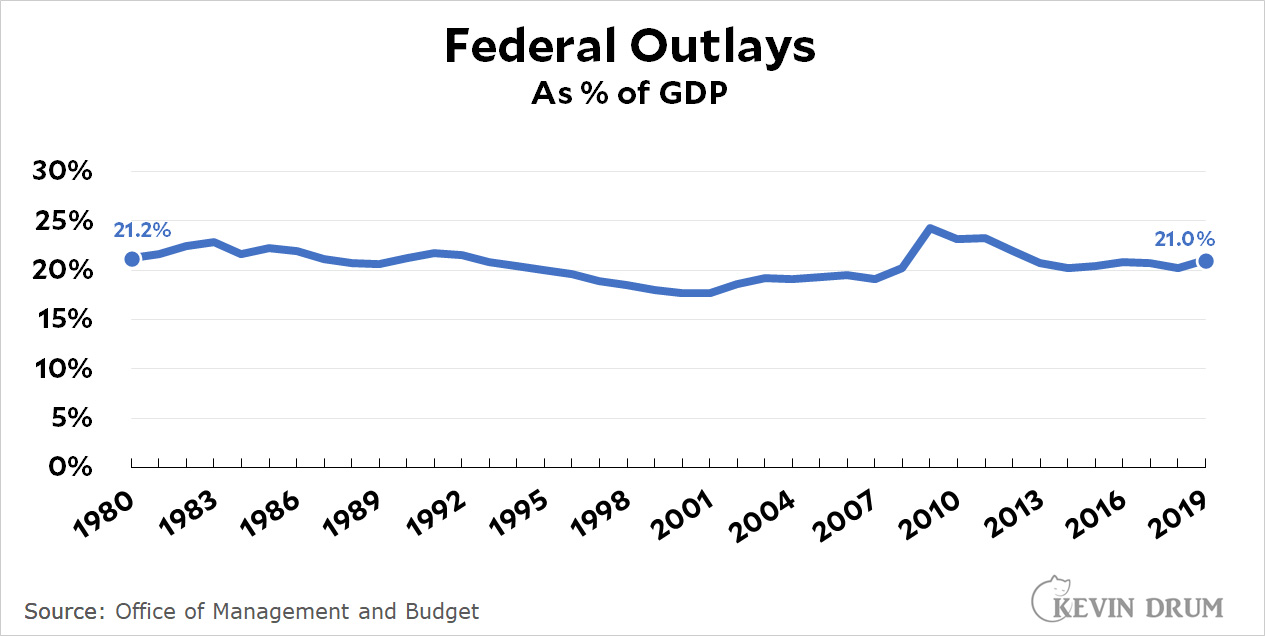

The Center for American Progress says that our recent big deficits are due to Republican tax cuts. Their explanation is a little complicated, but it's all pretty obvious if you just look at federal spending:

In 2019—the last year before the pandemic—the federal government spent almost exactly as much as it did in 1980. Spending was up a bit during the 1991 and 2000 recessions, and up a lot during the 2008 recession, but it always settled down afterward to around 20% or so.

In 2019—the last year before the pandemic—the federal government spent almost exactly as much as it did in 1980. Spending was up a bit during the 1991 and 2000 recessions, and up a lot during the 2008 recession, but it always settled down afterward to around 20% or so.

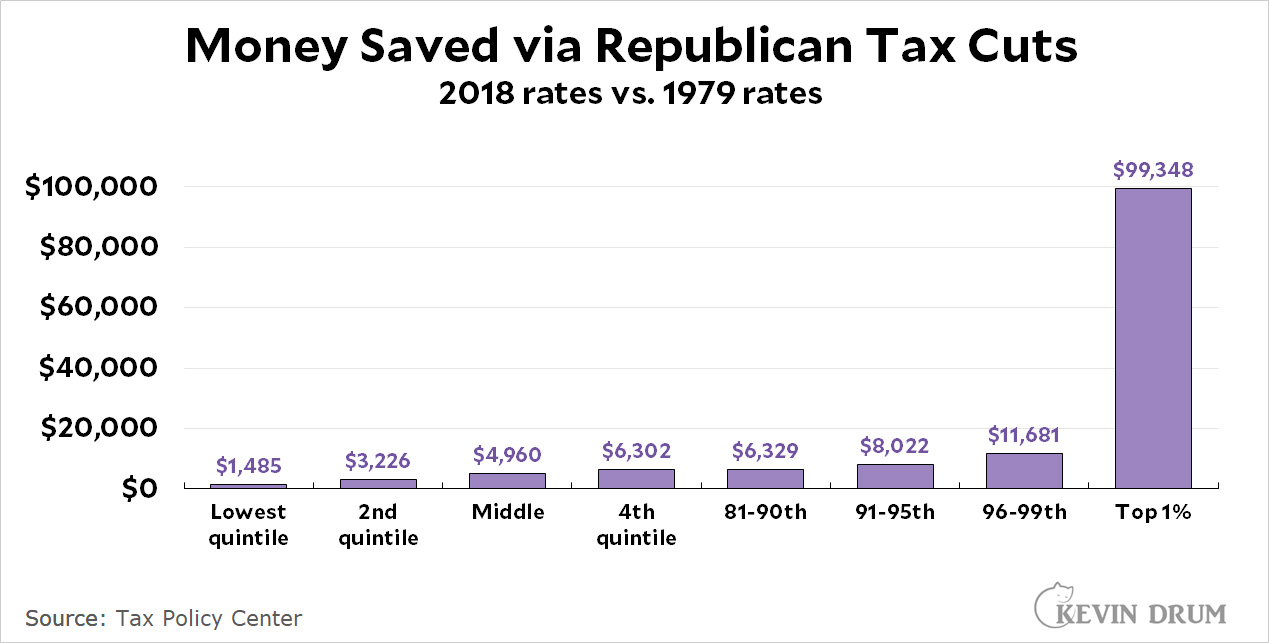

So yes, if spending is the same as it was 40 years ago then consistent deficits are obviously due to tax cuts.¹ And here's a reminder of just who those tax cuts were for:

Everybody has gotten tax cuts, but the big winners were the super-rich. Not only have their incomes quadrupled since Reagan was president,² but their tax rates have gone down enough to save them some serious money on top of that. It's a sweet deal.

Everybody has gotten tax cuts, but the big winners were the super-rich. Not only have their incomes quadrupled since Reagan was president,² but their tax rates have gone down enough to save them some serious money on top of that. It's a sweet deal.

¹That is, average deficits over time. There are also temporary deficits during recessions, including the one we had during the pandemic recession. Those typically last a few years and then disappear.

²Yes, of course I adjusted that for inflation.