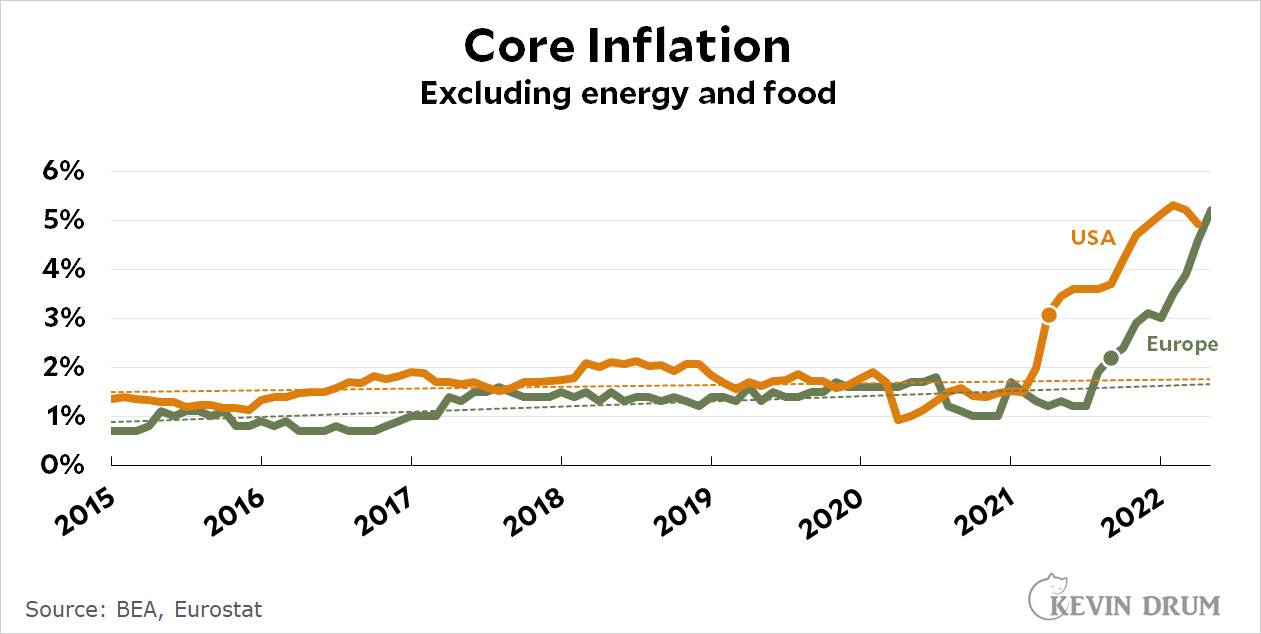

The chart below shows core inflation for both the US and Europe:

For the US I used the PCE price index excluding energy and food. For Europe I used Eurostat's HICP index excluding energy and unprocessed food. Since these are core inflation rates, they are unaffected by differences in oil spikes, Ukrainian food blockades, and so forth. This is just plain, underlying inflation.

The two markers show when core inflation first jumped more than half a point above its trendline. For the US that happened in April 2021. For Europe it happened in September 2021.

Given the timing, it seems likely that the initial surge in the US was prompted by the $1.9 trillion American Rescue Plan, which produced higher consumer spending for a few months before the flow of money stabilized. Then, in September, inflation surged again in both the US and Europe even though consumer spending was pretty flat. Given this, I would apportion the causes of core US inflation like this:

- Underlying inflation: 1.5%

- ARP: 2%

- Supply chains etc.: 1.5%

In Europe, it's more like:

- Underlying inflation: 1.4%

- Supply chains etc.: 3.8%

I've done this calculation a few times before using different data, but it always comes out about the same.

So here is my surprising conclusion: ARP has run its course, which is why core inflation has softened over the past couple of months. That will eventually leave us with core inflation of about 3.5%, which will decline as consumer spending eases and supply chains open back up.

Europe is a different story. They apparently handled supply chain issues considerably worse than we did, and that's pretty much the sole source of their surge in core inflation. It will not start to decline until they fix this.

In addition, both the US and Europe are suffering from an additional 3.6% inflation thanks to soaring food and energy prices. This is likely temporary, and in any case there's very little that policymakers can do about it.

Bottom line: Despite our endless whining about it, the US handled its supply chain issues pretty well. And while Joe Biden's spending package may have created some additional inflation, it was temporary and it gave the economy (i.e., actual American people) a boost when things looked bleak.

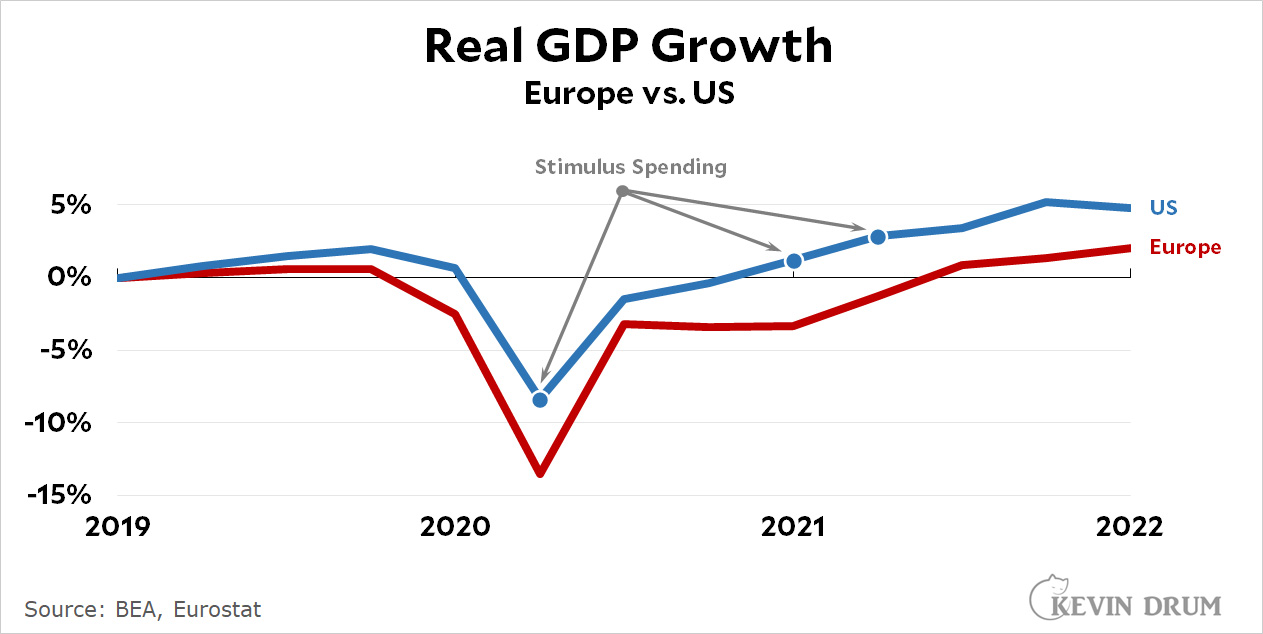

Europe, by contrast, appears to be suffering much worse from its handling of supply chains, and their economy is more sluggish than ours because we were more generous with stimulus spending (in March 2020, December 2020, and March 2021).¹ We might not have been perfect, but which place would you rather live in?

¹Europe didn't need as much stimulus thanks to its relatively strong safety net. Even so, they were too stingy with stimulus spending. In the end, this stinginess hurt their economic growth and didn't help them with inflation, which is currently higher than ours.