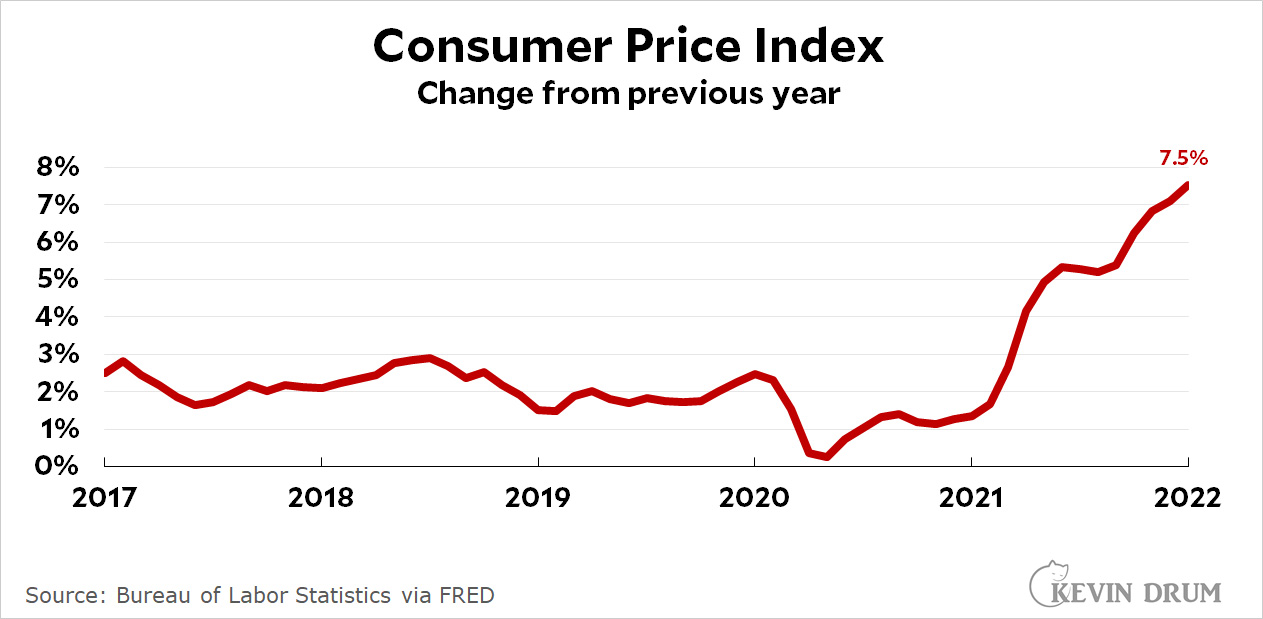

Inflation remained high in January:

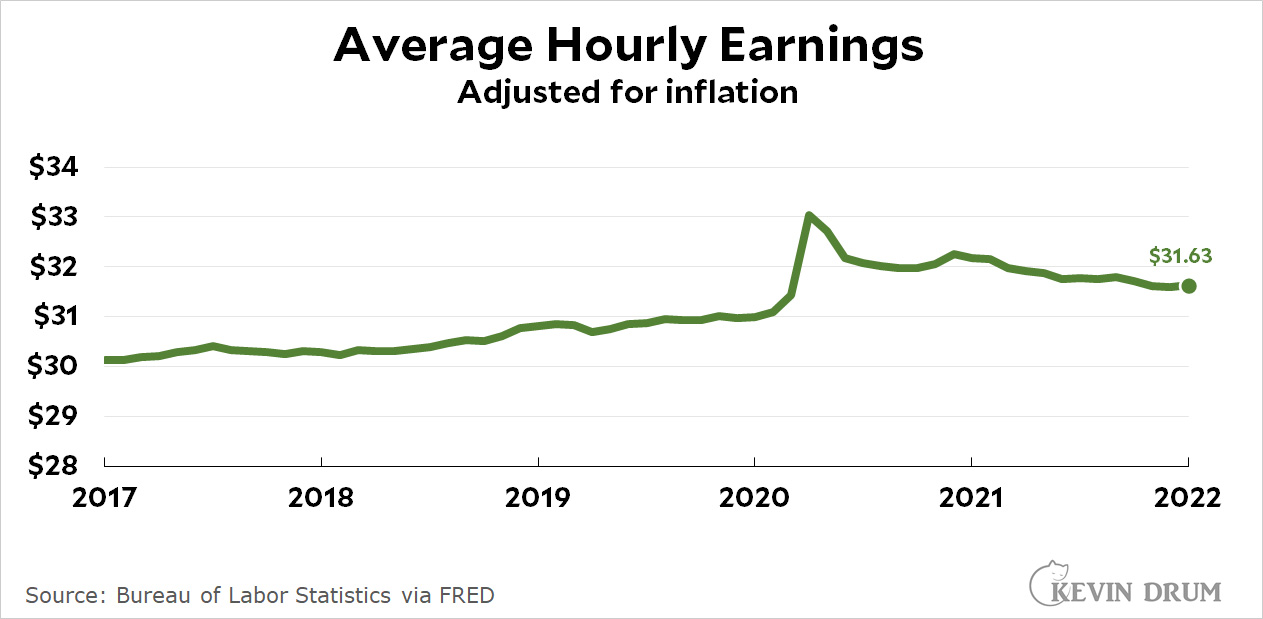

Because of this, real hourly earnings were down yet again:

Because of this, real hourly earnings were down yet again:

Real hourly earnings fell throughout all of 2021 and are continuing to fall in 2022.

Real hourly earnings fell throughout all of 2021 and are continuing to fall in 2022.

Cats, charts, and politics

Inflation remained high in January:

Because of this, real hourly earnings were down yet again:

Real hourly earnings fell throughout all of 2021 and are continuing to fall in 2022.

Comments are closed.

Tha Carter II: as Inflation skyrockets, Democrat officials await the next footwear collapse -- James Earl Carter IV endorsing Stacy Abrams's hopeless challenge to virile stud Brian Kemp.

It's funny that some experts are being quoted as worrying that, though inflation will subside in coming months, it will probably stay higher than it was in 2019.

As I recall, people like Paul Krugman thought the inflation rate was too low in 2019. Letting the rate be higher than 2% has been the Federal Reserve's plan for a while now. Not that they want it to be 7%, but I get the idea they'd be comfortable with 3% or even 4% inflation.

Inflation was uncomfortably low for quite some time.

A stable inflation rate of 3 to 5 percent is likey somewhat better for overall macro-economic management as helping avoid rate compression around the "zero bound" and negative interest rates which are awkward.

A rapid acceleration to 7%+ is however not a great thing, particularly as the lessons of the early 1970s were that being sanguine about such has a tendency to open the door to inflation spirals.

And of course rapid inflation shifts do rather tend to hit lower income classes rather more strongly, which is upsetting to them, having less absorption buffers. So Democrats would be well advised to not repeat their 1970s responses.

The bond market does not seem to reflect the idea that we're heading toward 70's style inflation but I wonder how the bond market behaved back them. Is it a good predicter ?

There is no reason for the bond market to yet reflect that, any more than expectations yet reflect.

The lesson is not that the USA (whose inflaiton is rather more than EU experience at this stage) is heading to 1970s but rather as with late 1960s early 1970s, hand waving away and inattention to the risk of sustained and self-reinforcing inflation has the potential to open up that door.

Should reasonble action be taken, then being sanguine is reasonable.

But the story of Transitional is over.

But the story of Transitional is over.

You keep banging on this particular drum. But in the case of the United States, at least, the most famous example of transitory inflation—the post World War II burst—in fact lasted two years. Which would imply that the inflation currently plaguing the US economy: A) might well be transitory in nature, and B) might have another year or so to go

The Newspeak dictionary’s entry for “transitory” will need an update.

I don’t believe there is anywhere sufficient historical data to provide an empirically-validated estimate of the maximum duration of a transitory inflationary period. The post-World War II inflation lasted about two years, and ended without aggressive Fed or Treasury action, apparently: https://www.federalreservehistory.org/essays/wwii-and-its-aftermath

why? the current definition of not permanent seems fine.

With past punditry promoting trend lines it seems apt to point out how real earnings appear to be reverting to the historical trend.

I'd say so.

Was CNBC in error asserting

or is this a matter of which of many metrics to choose? https://www.cnbc.com/2022/02/10/january-2022-cpi-inflation-rises-7point5percent-over-the-past-year-even-more-than-expected.html

The most recent month on Kevin's chart looks like a slight uptick. I don't know why he said it was down.

He was wrong. .7 increase vs .6 increase. .1 increase.

Isn't this expected? After all you don't want to compensate people for inflation that has not occurred yet.

What--not plot of month to month changes???

There have been two humps in month to month inflation (seasonally adjusted) over the past year: one topping off at 0.9 in June 2021, which dropped down to 0.4 ish; then a spike in Oct 2021 to 0.9 then slowly dropping down, now at 0.6 in Jan 22.

Year over year inflation rates will start to drop in March and April since the baseline prices were already going up by then last year.

Dumb question, I'm sure, but wouldn't the Fed be advised to move up their expected rate hike, to, like, now? Why wait until next month? I'm sure they have procedures they follow, and no doubt they don't want to panic markets. But I think markets (and consumes) would welcome the reassurance that the Fed has no intention of standing idly by. The key thing to avoid is allowing inflationary expectations to become entrenched into the psychology of businesses, workers and consumers. So, maybe some surprise on the hawkery side would be helpful.

Typically the Central Banks hate to take out-of-cycle decisions as this tends to signal an emergency and a crisis from market perpsective. And hastiness has its own risks. Unless there is indeed an urgency, typically better for the Central Bank to display deliberative sang froid.

Yes.

They're still unwinding the "quantitative easing" now.

Also, just the talking of the Fed's interest rate hike has driven up some mortgage rates already.

I'm not quite sure what goes into inflation calculations, the price of the house or the cost of mortgage payments....

FWIW, I haven't gotten a raise (I'm in high tech) in two years because my company has been worried about the impact of the pandemic. We've been incredibly profitable over this time but I understood why the past two Junes (when raises are decided) it was decided to forego raise becauses of uncertainty. It is very likely we will get raises this year and they may be larger than is typical.

I'm guessing my experience is not unusual and if so this would help keep median wage growth down.

But this is not the experience of people in the bottom quarter of income. Their wages have still gone up some even inflation adjusted.

https://fortune.com/2021/12/10/inflation-wages-low-income-workers/

If a company is making a lot of money and wants to share with the employees that made that happen but worries that it might not be able to support salary increases over the long term it issues bonuses.

Just not giving you a raise or a bonus is what they do when they figure they can just keep all the money themselves.

Your boss is fucking you over. All the anecdotes I hear about are people who are changing jobs for massive pay increases.

Imo a five year chart of 'vs one year ago' numbers is a weird thing. Why not just a chart of the cpi? What is the complication of vs one year ago adding?

Also a little tricky that a chart of a very odd display of inflation is paired with an inflation adjusted chart.

What do I expect these two to look like in various conditions? Not simple.

“Why not just a chart of the cpi?”

Here you are:

https://fred.stlouisfed.org/series/CPIAUCSL

Departure from the trend since ~1982 isn’t so dramatic … yet.

My favorite read in economics was “Asking about Prices” by Alan Blinder et al., which was an empirical investigation of price stickiness, and the implications for twelve hypotheses/theories found in the literature, none of which held up well. I wonder if some of the current prices increases are opportunistic - taking advantage of the ‘cover’ provided by the most salient rises, such as for gasoline. The pressure from stock analysts to meet short-term profit expectations may also be encouraging some to try to quickly make up for pandemic-related shortfalls.

I caught a sound bite--a company pushed thru a 10% (or was it 20) price increase and saw profit double.

When many people, like me, were worried in 2021, our friend Keven, for some unfathomable reason*, made at least a dozen "inflation is not a threat" posts with cherry-picked statistics and speculative theorizing. It was COVID, supply chain, used cars not a huge part of the economy, use this different index, etc. I pointed that out here and was lambasted for my impudence.

What interest me is, why be complacent about inflation, especially since *it hits the poor the hardest*. Any shmoe with $40,000 saved in cash saw an effective loss of $3,000. There are lots of people who aren't ready to buy a house or stocks and they simply cannot be made whole after inflation strikes. I'm surprised that Democrats weren't more concerned about those at the low end of the economic scale. They may now pay a political price, which isn't good for the nation this election year with democracy at stake.

* he lived through the inflation of the late 1970s and witnessed the massive disruption it caused. In particular, the ability of those better off, with real assets, kept their wealth while other lost massively.

“I'm surprised that Democrats weren't more concerned about those at the low end of the economic scale.”

First, for those on the low end of the economic scale, having a job, or two, is the top priority. If you don’t have an income, steady prices don’t help you.

Second, the President and most Democrats in Congress spent months trying to pass BBB, which contained a number of programs to help the low end pay for child care, health care, prescriptions, post-secondary education, and more. Initially, it contained tax increases for those on the high end, which would have helped cool the economy. That is about the limit of what the Executive and Legislative branches can do to ameliorate inflation and/or widespread price increases.

KenSchulz - respectfully most of the expert analysis of BBB had a slightly different take. BBB, because the spending was front loaded, would cause a small increase in 1 - 2 inflation: the magnitude would not be large. In contrast, once again the impact would be very small, BBB would have a limited impact on reducing ten year inflation. Basically, BBB was not large enough to meaningfully change inflation in either direction.

As for what a President could do to reduce inflation:

Clearly who is on the Fed board matters.

Regulatory policy matters. https://www.washingtonpost.com/us-policy/2022/01/26/inflation-white-house-experts/

Advocate for tax and spending policy that is deflationary: clearly this is the opposite of Modern Monetary Theory nor do I suggest this path

Reduce Federal employment/spending....I am not recommending this but yes that is in the range of options.

Often the actions that would reduce inflation, at least in the near term, are the opposite of the Democratic agenda...

I noted that only earlier versions of BBB were budget-neutral and therefore non-inflationary. Sen. Sinema and others rejected almost all of the proposed tax increases, so the smaller bill would have been modestly inflationary.

The FRB Board of Governors should not be politicized; each President has a limited number of opportunities to appoint.

The object of controlling inflation is to prevent the harm it inflicts on citizens - creating a recession to reduce inflation is a lousy solution. The Democratic agenda does more to protect citizens from economic harm than the blunt instrument of interest rate hikes.

Actually, fiscal policy (taxing and spending) is exactly how MMT proposes to control inflation.

You certainly cherry-picked the WaPo article, and regulatory policy and FRBBOG appointments are very slow-acting. William Spriggs’ recommendation is much better targeted: not only do high-income people consume disproportionately more, they drive inflation even more, because they are less likely than low- and middle-income earners to substitute.

Republicans=high unemployment. Deal fool.

Not quite. January rose expected and it's lower than 7% monthly. On pace for 4.8% yearly. It's why I ignore yry accounting. Most of this is lagging metrics and yry surge in gasoline stocks.

Demand has slowed back to normal. YrY declines exenergy coming.