The American economy gained 216,000 jobs last month. We need 90,000 new jobs just to keep up with population growth, which means that net job growth clocked in at a moderate 116,000 jobs. The headline unemployment rate was unchanged at 3.7%.

This is a perfectly reasonable report, but the bad news is that December saw a huge exodus from the labor force. The number of employed people dropped by 683,000 and a total of 845,000 people left the labor force. These are seasonally adjusted numbers, so they aren't due to any kind of holiday hiring artifact.

As a result of this, the labor force participation rate went down from 62.8% to 62.5%. This is not a huge decrease by itself, but it's not a good trend.

Florida governor Ron DeSantis (R.) called for the abolishment of the IRS during a CNN town hall in Iowa as he makes his final few pitches to the voters of the Hawkeye State. DeSantis said, “I want to eliminate the IRS, and I would like a flat — one single-rate flat tax.”

....While DeSantis’s call to level the IRS and its loopholes may strike the casual viewer as either a move of desperation for a flagging campaign or....

Nope, we can stop right there. It's a move of desperation, full stop. This is just about the oldest con in the Republican book, a cheap applause line with nothing to back it up.

For what it's worth, a flat tax would cut taxes on millionaires and raise taxes on the middle class. It would also blow up the deficit since no plausible flat tax would raise anywhere near the revenue we currently raise.

But you all know that. Everyone knows that—including Ron DeSantis.

Yesterday I wrote about the federal budget for this year and how much it was going to get cut in various scenarios. As you'll recall, I was puzzled about what was really going on.

But complaining gets results around here! Today the CBO published a definitive letter on precisely this subject. Note that "this subject" is nondefense discretionary spending; defense spending is relatively untouched by all this. Here's the short version:

Under the continuing resolution we're currently using (because House Republicans can't agree on a budget), we are spending at a rate of $777 billion.

If the CR is still in place by May 1, spending has to be cut to its 2023 level ($744 billion) minus 1%. This comes to $736 billion.

If we pass a budget, we have to abide by caps agreed to in the debt ceiling agreement. This comes to $704 billion.

You can stop reading now if you don't want to tear your hair out. But if your follicles are strong, read on.

First: By definition, a continuing resolution keeps spending at old levels. So if CBO says 2023 spending was $744 billion, why are we currently spending at a rate of $777 billion? This is largely because there are a few items that were prefunded at higher levels than last year. Those higher levels are in effect now but didn't exist in 2023, so they don't count as part of the 2023 budget.

Second: If we spend at a rate of $777 billion from October through April, that's $453 billion. In order to get to $736 billion for the full year, we can only spend $283 billion in the final five months from May through September. That's a run rate of $679 billion, a decrease of about 13% from current levels.

Third: If we run into this situation, then on May 1 the president has to sequester spending to the new level. This is not done by picking and choosing what to cut. It demands a 13% cut across the board. That would be devastating.

Fourth: If we do pass a budget, we're even worse off. That would require spending be reduced to $704 billion. If the budget were passed on May 1, we'd have to cut spending for the second half of the year to a rate of $602 billion. That's a 22% cut. The good news is that since it's a budget, it can cut specific programs instead of just slashing across the board. Alternatively, of course, Congress could also ignore the $704 billion cap since it's not bound by its own legislation.

Fifth: None of this is set in stone. Congress can do whatever it wants regardless of what limits it placed on itself in the past. CRs always have exceptions (the current one has exceptions for WIC and the Columbia submarine, for example), and Congress could pass a full-year CR with exceptions for the prefunded stuff if it wants to. It could also choose to fund everything at a higher level. It can do anything it wants.

So, did you get all that? Huh? Did you?

Of course you did. It all makes perfect sense, doesn't it?

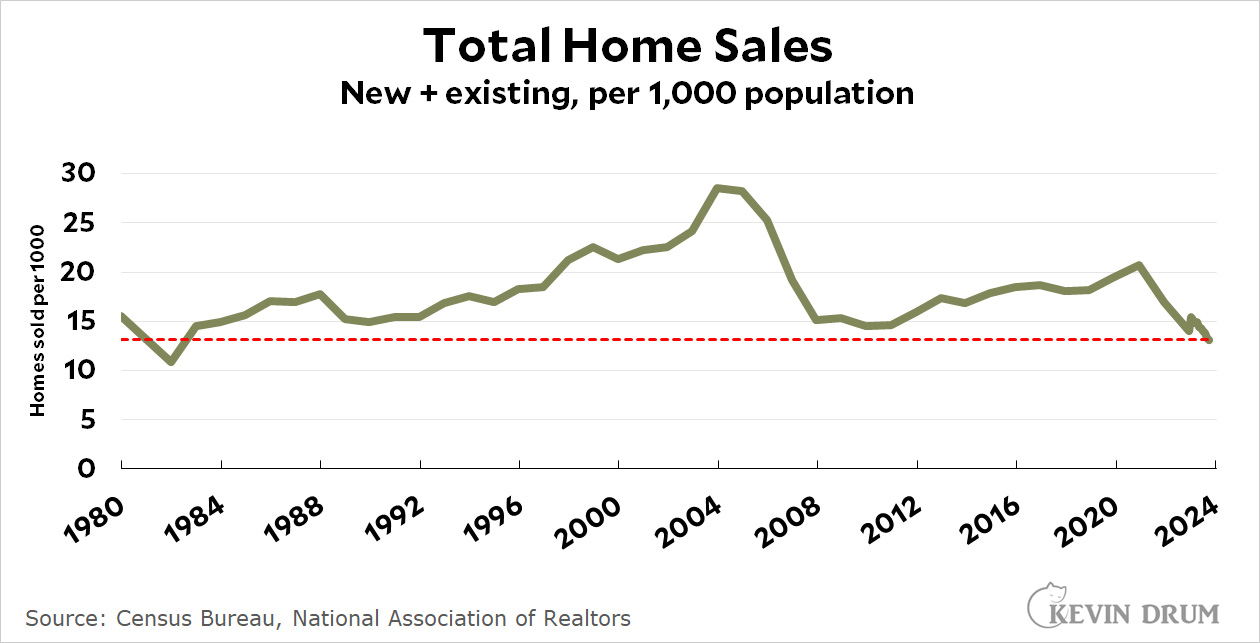

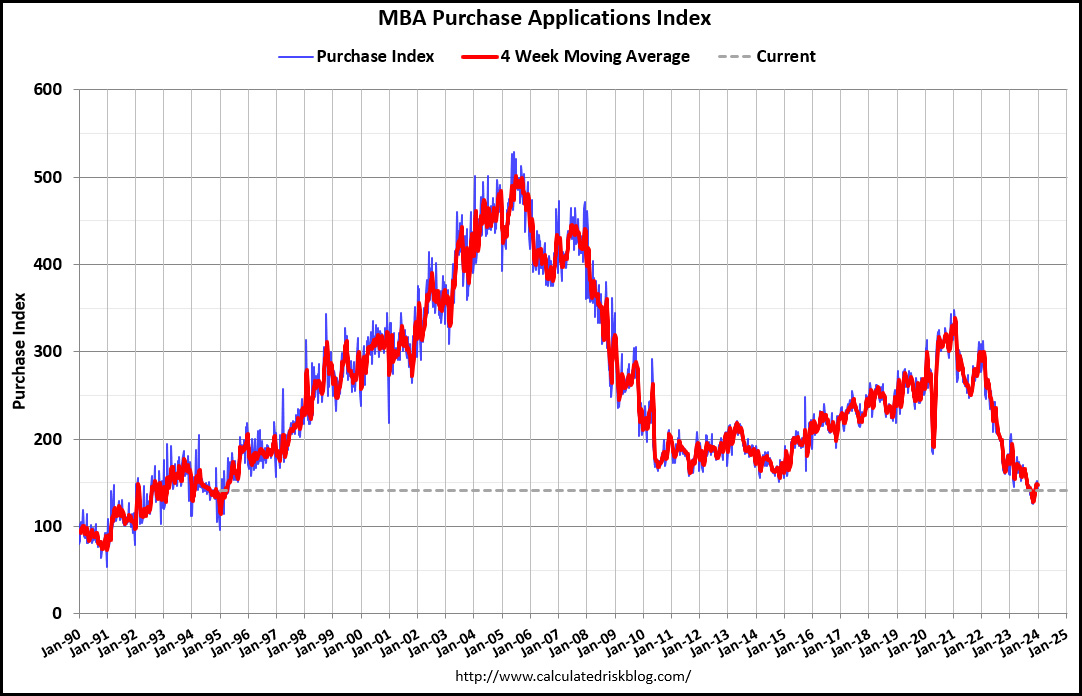

How's the housing market doing? There are two good measures: (a) total home sales and (b) mortgage applications. Here they are:

The top chart is home sales adjusted for population. It shows total home sales at the lowest level since the depths of the 1981-82 recession.

The bottom chart is unadjusted raw numbers for mortgage applications, and it shows they've dropped to their lowest level since 1995. If it were adjusted for population it would be very similar to the top chart.

So both measures agree: Home sales have dropped to lows we haven't seen for three or four decades.

This is not a great picture, but I had to hike for a good long time to take it. So by God, you're all going to see it.

This is Balcony House, one of the ancient cliff dwellings at Mesa Verde National Park. The only way to see it is to take a trail that curves around outside the right hand of the frame and then circles back on the other side of the canyon. When you get to the end, you have a long distance view of the dwelling.

Thanks to my bum hip and CAR-T fatigue I'm not much for long distance walking these days, and the trail is unmarked by any signage telling you how far you've gone or how far you have left. As it happens, it only took about half an hour to get to the overlook, but it felt like I was walking forever. And then I had to walk back! But at least on the way back I had some idea of how far I had to go. In the end, I was fine and my hip was none the worse for wear. And I got the picture.

October 13, 2023 — Mesa Verde National Park, Colorado

The LA Times draws my attention today to one of my pet topics: working at home. Gensler Research recently conducted a survey of office workers to find out if they were happy with their home-office split. They weren't, but not in the direction you'd think: on average, they said they spend 48% of their time in the office and would prefer to spend 63% of their time there. But why do they value more office time? Here's the breakdown:

Among all age groups the top reason was the same: to focus on work. Surprise! It's harder to focus on work at home than in the office, and apparently people are figuring this out. This gibes with time-use studies showing that people generally get less done at home than in the office.

Will this eventually lead to a broader retreat from working at home? Stay tuned.

Israel sent a drone into Beirut a couple of days ago to kill a senior Hamas commander. Hezbollah has said it will retaliate. Today the US sent a missile into Baghdad to kill a militia commander linked to Iran who had claimed responsibility for attacks on American troops. In the Red Sea, it seems only a matter of time before the US Navy takes aim at Iranian ships that are providing targeting information for Houthi attacks on Western cargo freighters. If that happens, Iran will undoubtedly launch reprisals.

President Biden has been an unshakeable ally of Israel in the Gaza war, but he's also desperate to keep the war from widening into a regional conflagration. It's starting to look less and less likely that he can thread this particular needle.

30-year mortgage rates are generally higher than long-term Treasury yields because mortgages are riskier. Usually the spread is around 1.7%, but for the past year it's been close to 3%. However, the Wall Street Journal informs us that the spread is coming down, which indeed it is. But not by much:

The Journal promises to tell us the "hidden force" behind the decline in the spread, but tell me if this makes any sense:

These days, investors have lots of reasons to demand more yield. For one, there is the risk that mortgages extended today won’t be around tomorrow. If rates fall, as many expect, homeowners will refinance into lower-rate loans.... The central bank last month signaled it is likely finished raising rates and could cut rates this year as inflation has been falling and the economy has remained strong. That is reviving investor demand for mortgages somewhat and pushing down the spread.

We are told that (a) the spread is high because rates might fall in the future and homeowners will refinance, and (b) the Fed could cut rates and this is pushing down the spread. Huh?

I have no idea what's really going on, but I suspect this is little more than the usual Journal practice of desperately looking for trend pieces based on tiny amounts of data. Elsewhere today, they have an article about panic among investors because the stock market was down for the first two days of the year.

POSTSCRIPT: The New York Times has a reputation for publishing a lot of iffy trend pieces, but the Journal really wins the prize here. The Journal's trend pieces are typically less sexy because they're related to finance and economics, not avocado toast, but if anything they publish more of them and rely on even thinner evidence than the Times. Our nation's CEOs are apparently desperate to consume a constant stream of faddish business trends and don't care much if they're true as long as they tell them what they wanted to believe in the first place.¹

¹Examples: inflation is a threat, it's impossible to find good workers, millennials are slackers who think they're owed a job, Gen Z's weird habits are destroying some market or another, colleges have gone soft, it's getting harder and harder to make a profit, a bull market is right around the corner, etc. etc.

According to Democrats on the House Oversight Committee, foreign governments trying to curry favor with Donald Trump spent nearly $8 million in stays at Trump's hotels during his presidency. As a public service, I have made a chart out of the top ten sycophants with the columns colored in beautiful Trump gold:

China is #1 by a mile at $5.6 million, but this is an unfair comparison since they're a lot bigger than the others. Here is per capita spending among the top ten:

Qatar is the winner! For its size, China is a relatively modest crook—and not a very effective one, either. Still, it's all pocket change for these guys.

How is Joe Biden doing in a trial heat against Donald Trump? In particular, how is he doing with young voters and Black voters? Take your pick:

Both polls were in the field at nearly the same time. But the Suffolk poll says Biden is behind with young voters 33%-37% while the YouGov poll says he's ahead 51%-33%. That's a net swing of 22 points.

The big difference is that in the Suffolk poll 30% of young voters say they're undecided or would vote for a third party. In the YouGov poll only 12% say that. This is a difference of 18 points, and accounts for most of the disparity between the two polls.

Among Black voters, the two polls largely agree. Suffolk says Biden has a +51% lead while YouGov says he has a +52% lead.

In the end, I doubt these two polls really disagree that much. For some reason, the Suffolk poll picked up a much larger protest vote among young people, but that's not likely to stand the test of time.

This is a perfectly reasonable report, but the bad news is that December saw a huge exodus from the labor force. The number of employed people dropped by 683,000 and a total of 845,000 people left the labor force. These are seasonally adjusted numbers, so they aren't due to any kind of holiday hiring artifact.

This is a perfectly reasonable report, but the bad news is that December saw a huge exodus from the labor force. The number of employed people dropped by 683,000 and a total of 845,000 people left the labor force. These are seasonally adjusted numbers, so they aren't due to any kind of holiday hiring artifact.