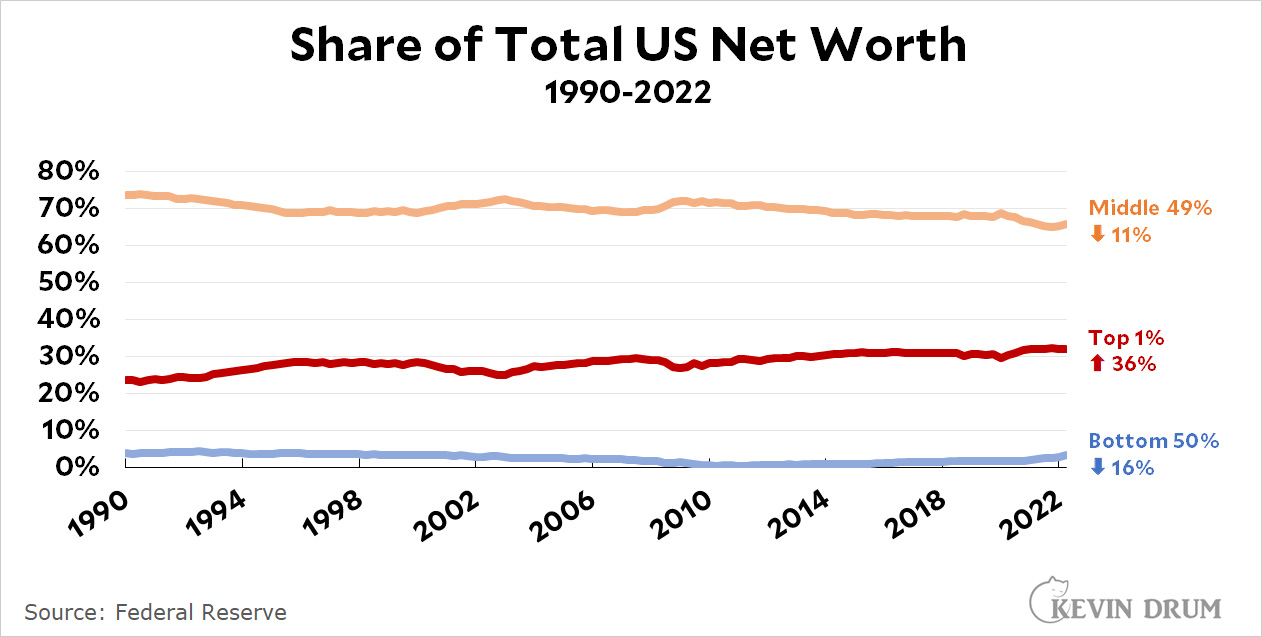

Except for one thing: Total net worth for all households has gone up 7x since 1990. So a record doesn't mean much unless that record is at least 7x the level in 1990.

It isn't. All that's happening right now is that net worth at the bottom is slowly making up for its long slide since 1990 followed by its disastrous plummet during the Great Recession. But even after 30 years, it still hasn't:

The share of total net worth owned by the bottom half of households has gone down 16% since 1990. Likewise, the share owned by the middle 49% has gone down 11%.

And the top 1%? I don't even have to tell you, do I? Its share has gone up 36%.

The post-Reagan era has been pretty disastrous for the working poor, the working class, and the middle class, and it's been OK for the upper middle class. But it's been truly spectacular for the rich.

And yet many folks in the working and middle classes still tell pollsters they trust Republicans more than Democrats to run the economy. Why? It is a mystery.

I took this picture in Bayeux, home of the Bayeux Tapestry. It's nothing special, but I like its pristine serenity. While I'm looking at it, I can believe for a few moments that there's nothing wrong with the world.

August apartment asking rents nationally fell 0.1% from July, according to a report from property data company CoStar Group. It was the first monthly decline in rent since December 2020, the company said.

Other surveys also showed rent declines of various degrees. Apartment-listing website Rent.com showed a 2.8% decrease in rent for one-bedroom apartments during the same month. A third measure, by the listings website Realtor.com, also noted a slight monthly decline in rent this August.

Not only has rent inflation peaked and then declined, it's now negative. We are experiencing rent deflation.

As usual, don't get too worked up about a single month's data. Still, the fact that rent inflation has been close to zero, whether negative or not, is yet another sign that inflation peaked at the beginning of the year and has been declining ever since.

Amid a national shortage of home-care workers that deepened during the covid-19 pandemic, the couple spent much of this year on a private agency list waiting to be assigned a professional home-care aide. But over four months, from April to August, no aides were available, leaving Acey to carry the load on her own.

....The shortage predates the pandemic but has been exacerbated by it, according to industry and government experts....“Fast food is trying to find workers and retail is trying to find workers and they are all trying to pull from the same labor pool,” said Kezia Scales, senior director of policy research at PHI.

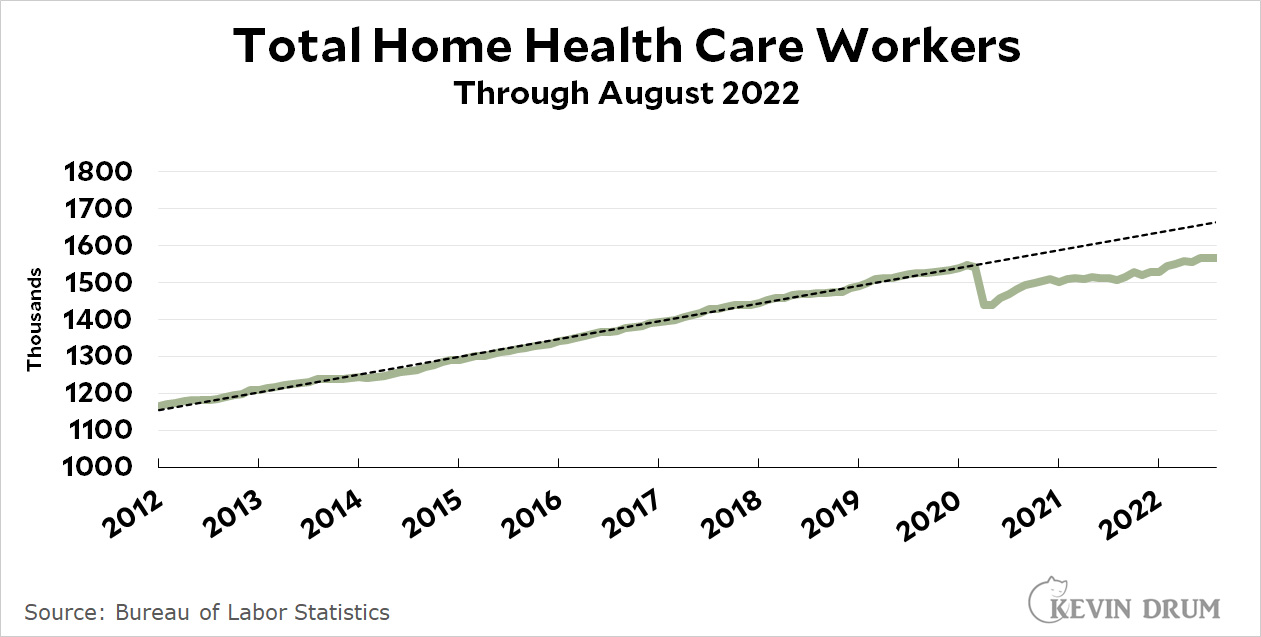

As I'm sure you know, this kind of story is like catnip to me. Is there really a shortage of home health care workers? Did it get worse during the pandemic? Here's what the Bureau of Labor Statistics has to say:

The Post has it right: The number of workers, which was probably already insufficient, crashed by 100,000 at the start of the pandemic and has never caught up.

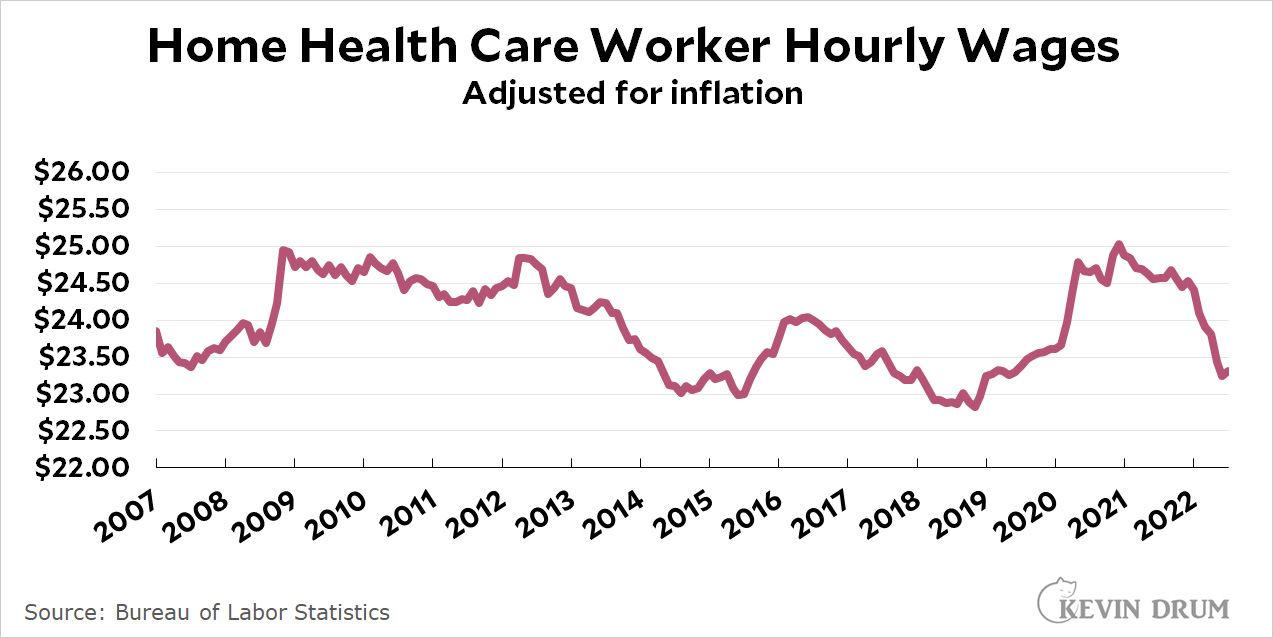

But you know what's coming next, don't you? Here's how much we pay these folks:

Pay went up at the start of the pandemic, but then slipped back down afterward. It's now less than it was in 2007. And even this overstates things, since it includes all home health care workers, including registered nurses and other specialists. For ordinary unskilled aides, pay is more in the range of $15—which ought to sound familiar.

Sure enough, the quote from Kezia Scales in the Post story says it all: we're pulling home health care workers from the pool of fast food workers. If that's what we think of the job, is it any wonder that we can't find enough of them?

The only way this gets better is if we pay home health care workers considerably more than we do now. But of course lots of people can't afford that. And that's why this is ultimately a Medicare problem: we desperately need to make long-term nursing care part of Medicare, and we need to pay workers more if we want to attract higher quality folks. This would be expensive, but it's inevitable that it will happen someday. The sooner we accept that the better.

Officials in Russian-occupied territories in eastern and southern Ukraine were forcing people to vote “under a gun barrel,” residents said on Saturday as staged referendums — intended to validate Moscow’s annexation of the territory it occupies — entered their second day.

What's the point of this? Everyone knows what's going on, and Moscow is hardly even making an attempt to pretend the referendums are real. Should we take it as good news that even a thug like Vladimir Putin feels like he has to at least symbolically carry out the norms of democracy?

Having written a technical preface a couple of days ago, it's now time to write a review of Brad DeLong's Slouching Towards Utopia. I'd like to keep this tolerably short, but even as I type these words I know that's not in the cards. Don't say you weren't warned.

OK then. Roughly speaking, I'd say there are two main themes in STU:

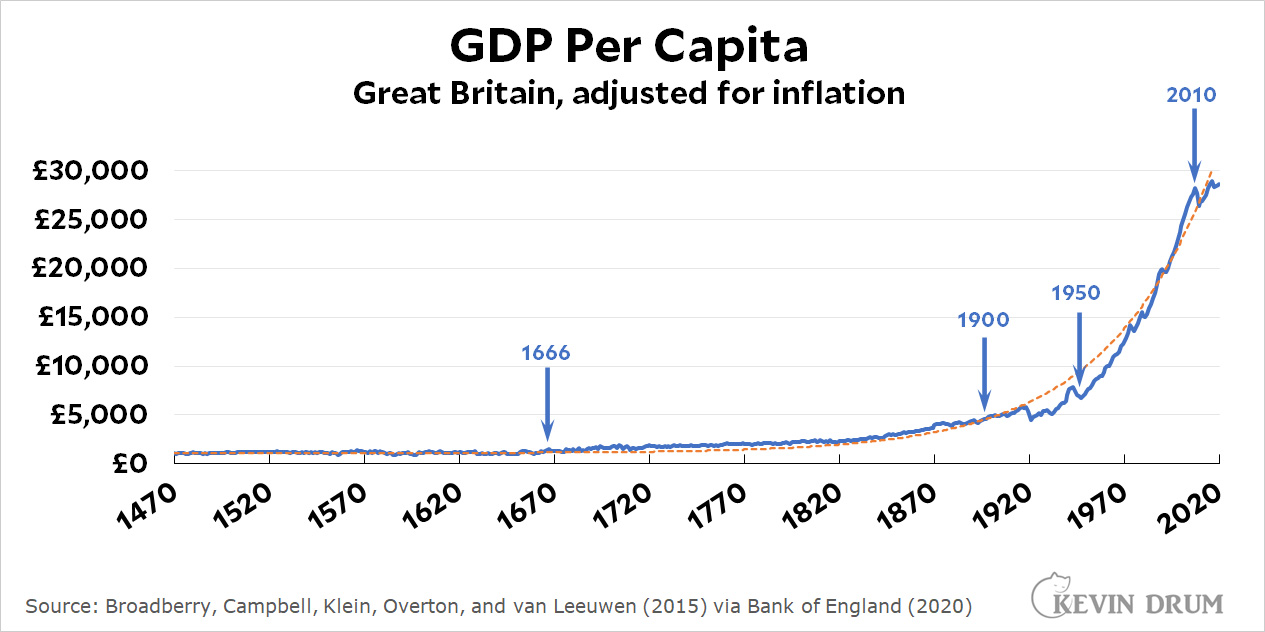

The year 1870 is a breakpoint in human history thanks to the development of globalization, modern corporations, and industrial research labs. Because of these things, it's the first time that the world—or, more precisely, the northern half of the world—broke out of its Malthusian trap and began to provide permanently higher incomes to common workers. (I am skeptical of this for reasons I outlined at length in the preface.)

The economic history of the "long 20th century" from 1870-2010 was primarily a contest between free-market capitalism, which produced growth but not an equitable distribution of goodies, and the welfare state, which interfered with the efficiency of the market but allowed everyone to benefit from technological progress.

First things first: purely as an economic history, this is a wonderful and engaging book. I didn't learn a lot that I didn't already know, but a large part of that is because I've been reading Brad's stuff for 20 years. Nevertheless, I enjoyed reading it again all in one place.

But I had a problem with it. I explained in the technical preface that I didn't buy the notion that 1870 was special per se. Rather, it just happened to be the point on the growth curve of the Britain-led Industrial Revolution that produced per capita GDP high enough to start trickling down to everyone.

Nor did 1870 represent a sudden outbreak of new inventions. Here's a brief list of 19th century inventions and ideas:

High-pressure steam engine

Steamboats

Steam locomotives

Canal networks

Telegraph

Rifle/revolver

Electric motor/generator/dynamo

Vulcanized rubber

Portland cement

Colonialism — I'm thinking here not of the necessarily limited coastal version but of the brutal extractive version that dominated the second half of the 19th century.

Modern fractional reserve banking

Steel-hulled steamships

McCormick reaper

Sewing machine

Bessemer process

Limited liability companies

Safety elevator/skyscrapers

Progress — by which I mean the idea that not only should we expect technological progress, we should actively promote it. Manifestations of this are things like patent offices, industrial labs, and research universities.

Internal combustion engine

Mail order catalogs

Telephone

Light bulb

Public health improvements

Automobile

AC electricity grid

These things span the entire 19th century. Some are ordinary physical inventions (steamships, light bulbs) while others are ideas or organizational improvements (progress, capitalism). Some have specific invention dates, while others developed steadily over long periods. But nothing about this list suggests any kind of sudden surge around 1870.

Does this really matter? It does. The whole concept of 1870 being special is surprisingly central to Brad's larger thesis. His contention—and I hope I'm being fair here—is that the miraculous growth which started in 1870 opened up the doors to utopia (thus the title of the book). That is, it suddenly became possible to envision a future in which every one of us was literally awash in the products of our factories and laboratories. All we had to do was follow a simple path that was now clearly marked out for us.

But we blew it. There was World War I. Then the Great Depression. And World War II. Then the "Glorious 30 Years" of fabulous growth, but followed by the neoliberal turn in which ordinary workers were once again cannon fodder for the rich. And all along we failed to include the global south in our growth revolution. Finally, the Great Recession of 2010 exposed our financial system as a lie, and in 2016 the election of Donald Trump showed that ordinary workers were fed up and no longer believed the lie.

That sounds pretty discouraging. But what if 1870 isn't special? What if it's just another year in a long period of human progress—unprecedented progress, to be sure, but a long, continual period nonetheless? If that's the case, then there's no reason to view it as a turning point and no reason to think that human nature should change just because we all got steadily richer. In other words, we didn't blow it. We just did what h. sapiens does and always has done.

As Brad knows well, because he's written similar things frequently, we humans are just overclocked primates. We have developed a thin layer of cognition that allows us to gossip more effectively and solve differential equations on request, but that thin layer lives on top of millions of years of primate evolution. And we are still bound by it. In particular:

We are territorial.

We are patriarchal.

We are hierarchical.

We are addicted to dominance displays.

We are tribal.

So just as always, after 1870 we continued to have stupid wars. We continued to base our social structures on racism and tribalism. We continued to be seduced by charismatic (male) leaders. We continued to do stupid things just to show that we couldn't be pushed around.

This is, perhaps counterintuitively, a more optimistic view of the world than Brad's. He thinks something should have changed in 1870 and he's disappointed that it didn't happen. His entire book, but especially the last few chapters, is clouded by despondence over the events of the past century and, especially, the past decade.

I, on the other hand, think that nothing special should have happened just because we got better at inventing things. And it didn't. We just continued on our sloppy way, complete with wars and exploitation and lynchings and occasionally lunatic political parties. Still, we've made progress on all these things. Not a lot, but what do you expect in only a few hundred years?

This is why, for example, I think that our current MAGA-inflected politics is a pothole, not a roadmap for the future. We'll get over it.

As for economics in general, you all know what I think: in another 20 or 30 years we will have cheap, genuine artificial intelligence. That will be a breakpoint in human history and will make all our current arguments moot. Practically any economic disagreement you can think of simply makes no sense in a world dominated by robots and AI.

But we should keep arguing anyway. After all, I might be wrong about AI.

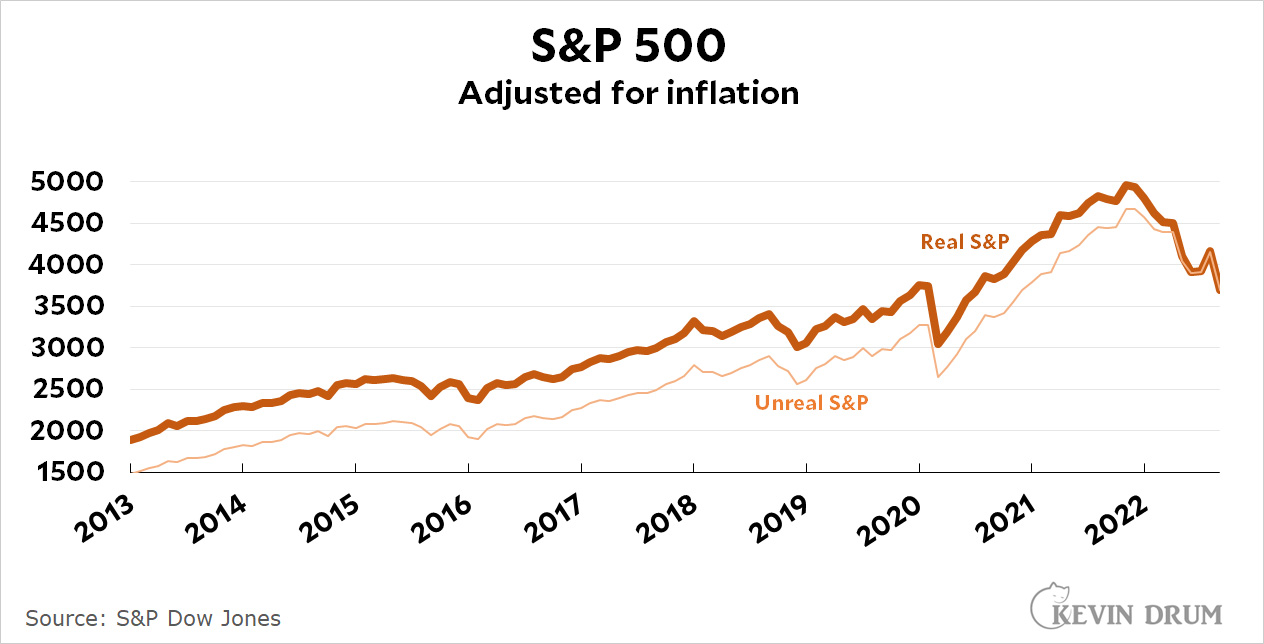

The Wall Street Journal tells us that the stock market is plummeting:

Dow Closes at a 2022 Low as Growth Fears Roil Markets

Wave of selling sweeps across the globe

But it's actually even worse than that. Here's something you don't usually see:

Adjusted for inflation, the market is down 25% from its peak, not just 20%.

It's a funny thing. In the bond market you can't avoid talk of inflation. The entire premise of the market is to get a return higher than inflation, and that's built into the entire structure of buying and selling.

But that's the premise of any investment, including stocks. And yet no one ever mentions inflation-adjusted stock prices. No one even compares the market indexes to the inflation rate—not often, anyway. Why is that?

In any case, even if you adjust for inflation the stock market has produced returns of 5% per year over the past five years. That's pretty good.¹ Hooray for long-term investing.

¹Assuming you put a bunch of money into the market five years ago, of course.

Business surveys published on Friday indicate that economic activity in Europe declined sharply in September, raising the risk of recession in one of the world’s industrial powerhouses as governments grapple with surging prices and disruptions from Moscow’s attack on Ukraine.

With Asian economies also struggling with rising interest rates and weakening exports, this leaves the U.S. as the only large economy showing a degree of resilience.

Don't worry, though! The Fed is doing its level best to wreck the US economy too. Pretty soon every region in the world will be collapsing.

But at least inflation rates will come down. Maybe we'll even be able to add deflation to our list of economic disasters.

The share of total net worth owned by the bottom half of households has gone down 16% since 1990. Likewise, the share owned by the middle 49% has gone down 11%.

The share of total net worth owned by the bottom half of households has gone down 16% since 1990. Likewise, the share owned by the middle 49% has gone down 11%.