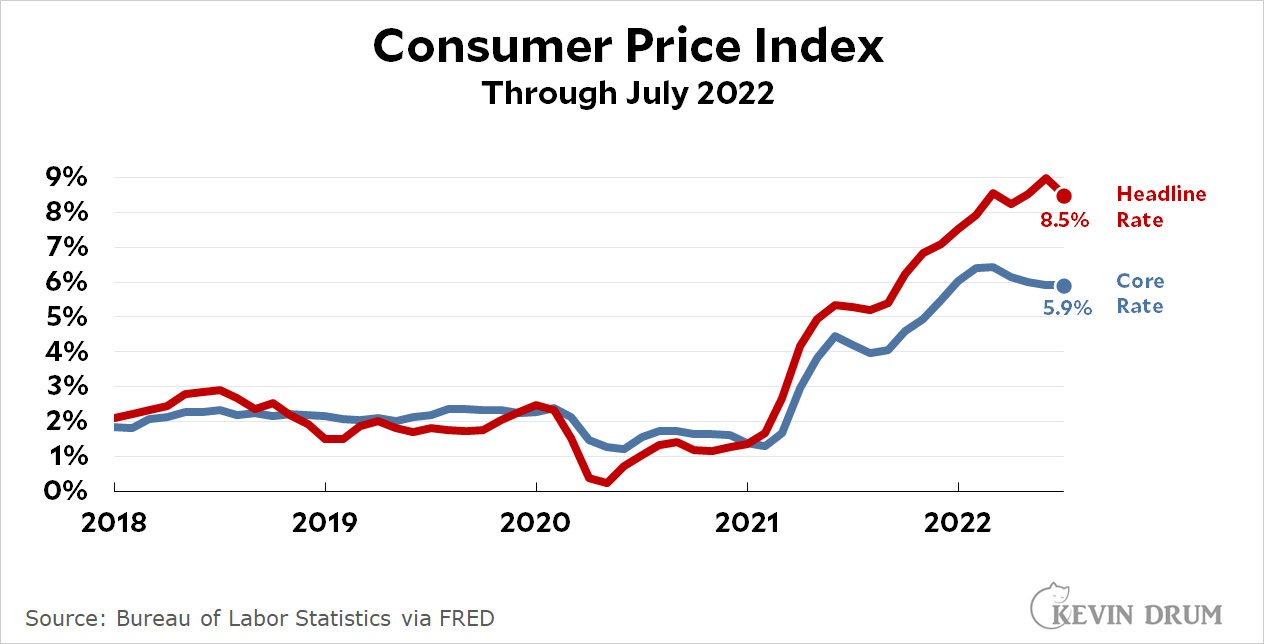

If we take CPI as our measure and assume that June was the peak for headline inflation, here's how long our current round of inflation lasted:

Headline: 15 months (April 2021 to June 2022)

Core: 12 months (April 2021 to March 2022)

Does 12 months count as transitory? Certainly it's longer than Team Transitory initially expected, which I think was around six months. On the other hand, one year isn't really all that long, especially when you consider the exacerbating effect of the Ukraine war, which was hardly predictable.

Personally, I was on Team Transitory all along and I still am. Am I just being stubborn? Maybe, especially when you consider how high inflation got. But in the great scheme of things, I don't think 12 or 15 months counts as a major league round of inflation. We took a chance on a big stimulus bill keeping the economy strong at the risk of higher inflation, and unfortunately the risk of inflation turned out to be real—largely because pandemic supply chain problems lingered longer than we expected; 2021 housing price increases got recorded this year for technical reasons; and Vladimir Putin decided to invade Ukraine and then botched it. But even knowing all that, I'd still make the same choice today. Maybe I'd cut back the stimulus bill a bit, but only by a bit.

OK, not really, but the news is good this month. The headline rate of inflation dropped from 9% to 8.5% while the core rate of inflation stayed steady at 5.9%. Given the underlying state of the economy, which is pretty strong, this probably finally represents that we've passed the peak of our latest round of inflation.

If that's true, it lasted about 12-18 months depending on how you measure things, and that's certainly as long as it should have lasted. With stimulus money long gone and housing prices starting to ease after a torrid 2021, the core rate started declining earlier this year. And with energy prices finally coming down from their June peaks, headline inflation is coming down too. In fact, it should be declining more, if you ask me. But food is still a problem, rising at a 10.9% annualized rate in July.

On the wage front, the news was good or bad depending on what you were hoping for. On a monthly basis, hourly wages were up 0.46% and weekly wages were up 0.49%. Since monthly inflation was down .02%, this means that hourly and weekly wages were up 0.48% and 0.51% respectively after adjusting for inflation. On an annualized basis that comes to 7.6% and 8.2%.

On a year-over-year basis, hourly wages were up 5.2%, which comes to -3.3% adjusted for inflation. Weekly wages were up 4.6%, which comes to -3.9% adjusted for inflation.

So wages were way up for the month but still negative for the year. Also remember that up is good if you're a worker, but down is good if you're worried about a wage-price inflation spiral. So you may decide for yourself if you think the July numbers were good or bad.

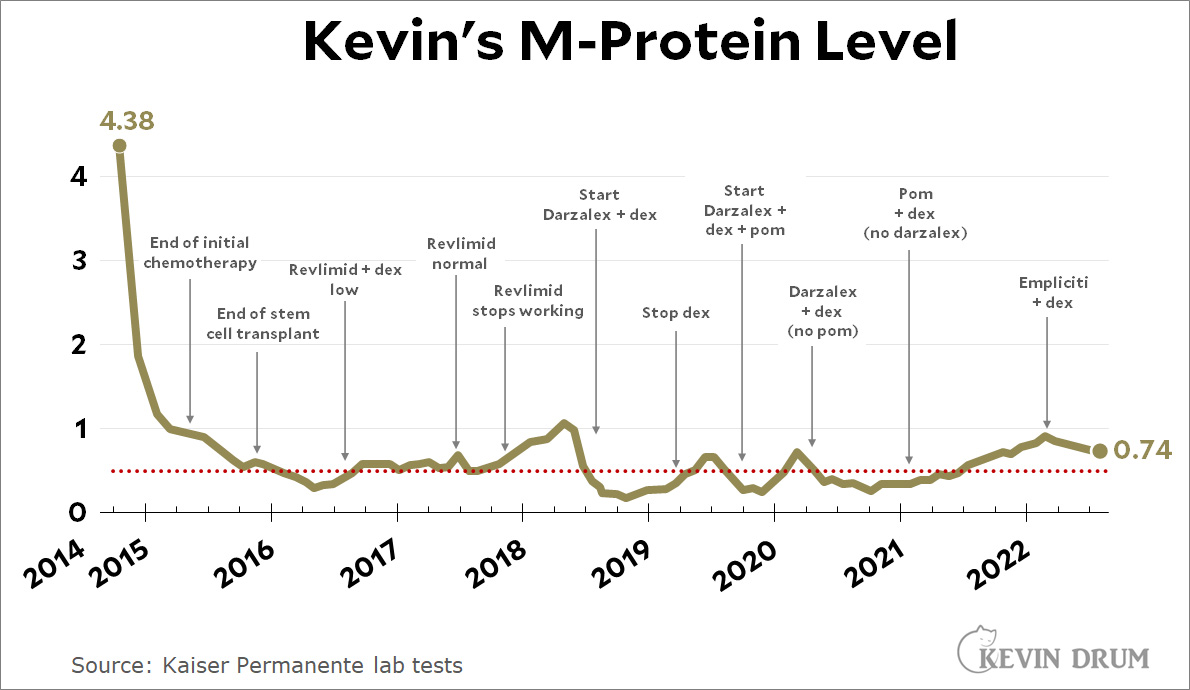

My M-protein level dropped from 0.75 to 0.74. A bigger decline would be nice, but holding things steady is fine. This won't matter for much longer anyway if I get the call for CAR-T treatment soon, since that will then be responsible for my cancer load and I'll be off the chemo treatments. Clap hard for this to happen in August.

Your average lazy travel blogger/photographer wouldn't bother to visit La Defense on a trip to Paris. "It's just a puffed-up office park. What's the point?" Or maybe they'd take a telephoto image from around the Arc de Triomphe and call it a day.

But not me. Admittedly, I didn't go until our very last day, when I had an afternoon to kill and nothing else to do. And it is just a quick Metro ride from central Paris. And it was born the same year as me. But the point is that I went.

And I'm glad I did. Sure, it's just a big office park, sort of like the Pentagon is just a big building. But it's impressive in its own right—although they should shoot the person who decided it was a good idea to build a crappy chain restaurant right in the middle of the courtyard. Overall, it was worth milling around there for a couple of hours watching the kids do wheelies and taking pictures here and there.

Republicans have gone all in on their gigantic hissy fit over the FBI search of Mar-a-Lago. In one sense, of course, this isn't surprising: the hissy fit has been the defining characteristic of the Republican Party ever since Newt Gingrich invented it in the '90s and and Fox News perfected it in the aughts.

At the same time, this is a particularly instructive case since literally no one has any idea what the FBI search was about. Classified document handling? Maybe. But we haven't seen the warrant. Or the application for the warrant. Or the judge's approval. Or any of the FBI work product leading up to it. Or anything. The FBI could be investigating Trump for anything from shoplifting to serial murder for all we know.

In other words, we know—for a fact—that the Republican hissy fit is based on absolutely nothing. It's just a reflex designed to work the refs, and we can only hope that this time around the refs (i.e., the media) don't fall for it. Republicans should get no extra coverage for their claims just because they're united and loud. They should get coverage if they have actual evidence to back up their complaints.¹

¹I feel like this should go without saying, but I mean real evidence, not the daily drip of dimwitted, context-less snippets that Republicans perfected during the Obama administration (Solyndra, Fast & Furious, the IRS, Benghazi, Hillary's emails, etc.).

Does the Republican hissy fit deserve the entire top half of the Washington Post's front page? You be the judge.

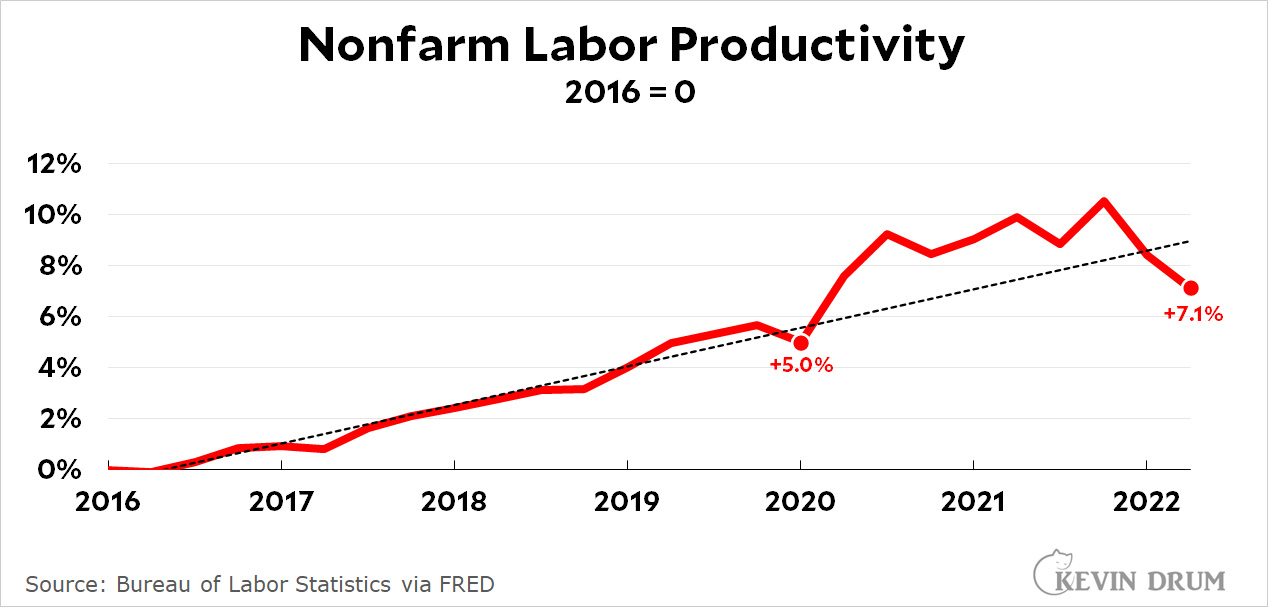

The BLS released productivity numbers for Q2 this morning, and the headline number is bad: a 4.6% decline from the previous quarter (at an annualized rate). This is bad, but in a slightly different way than it seems. Here's a chart that shows the absolute level of productivity, not the change from quarter to quarter:

This is, as usual, my favorite format. First I draw productivity from 2016 through the first quarter of 2020, just before the pandemic. Then I draw a trendline. Then I fill in the numbers from 2020 to the present.

What you see is that productivity went up faster than trend during the pandemic. This is because a huge number of people were laid off. Total output went down, but the number of workers went down even more. By simple arithmetic, this means that output on a per-person basis was higher than before.

As the pandemic eased, the opposite happened. Output went up, but the number of workers went up even more. The same arithmetic tells us that this means output on a per-person better declined.

There's nothing especially wrong with that. We should expect productivity to return to trend level once the economy has recovered. The problem is that this happened in the first quarter. But then, instead of leveling out, productivity declined again, taking us well below the pre-pandemic trend.

It's typical of recent recessions that productivity continues to go up or, at worst, stays flat. Usually, however, productivity keeps going up after the recession is over. This happened again this time, but only for a couple of years before it began to turn down. This is only the second time in 30 years that productivity has decreased two quarters in a row (the other time was in late 2012).

This is yet another indication of how strange the economy is right now: GDP is declining even as employment keeps going up. This is not usually how a recession works. (Nor is it how an expansion works.) So everyone is puzzled.

Here's one explanation that will probably ruffle some feathers: unemployment is too low. Employers have been snapping up anyone with a pulse, and this means they're pulling relatively unproductive workers off the sidelines. Many of them are now now stuck: hiring more people doesn't really improve output because the new workers are of such poor quality. They require more management time and more cleanup time after mistakes than they're worth. Maybe the conventional wisdom was right all along: 4% unemployment really is about the lowest it should ever get in an advanced economy like ours.

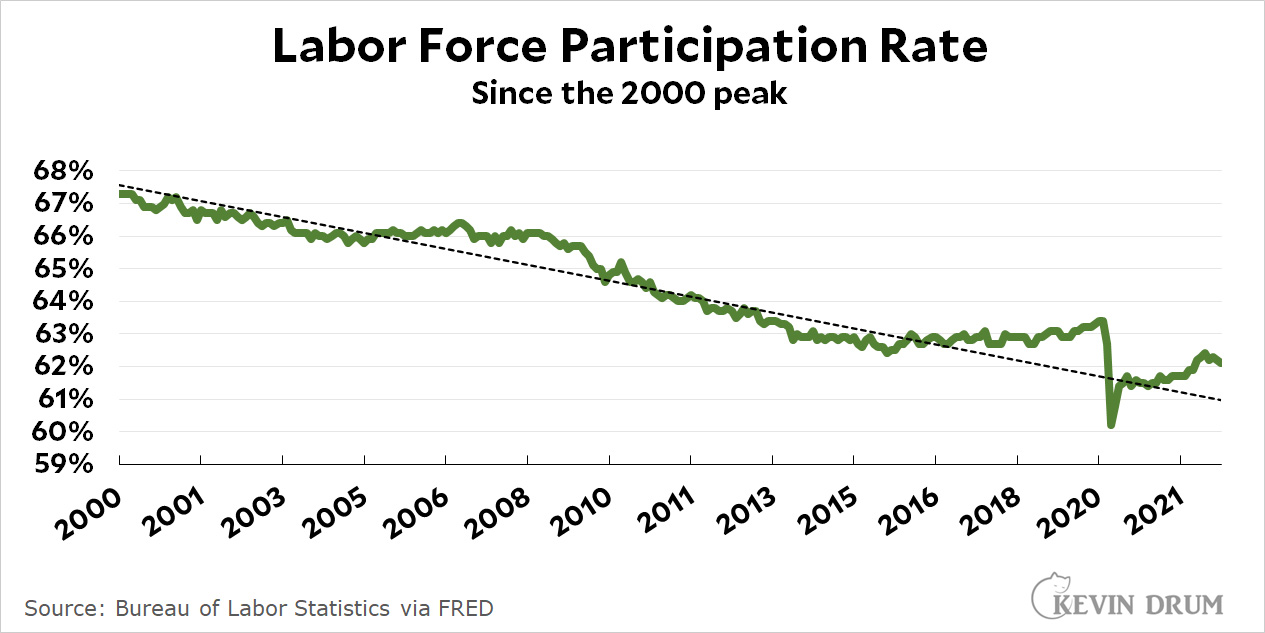

The way to return to growing productivity, as usual for the past century, is more machines. But things have changed. When the Industrial Revolution started, the productivity increase from automation was so great that we needed as many workers as before just to handle the huge increase in output. Lately, though, that hasn't been true. Automation has produced modest increases in productivity and the number of workers needed to handle the higher output has gone down. You can see that in the fact that the labor force participation rate has declined from its peak of 67% in 2000 to about 62% today. Here's what that looks like in a slightly modified version of my favorite format:

This time I drew the trendline through 2016, which shows a steady decrease in labor force participation. But then the participation rate flattened and even moved up in 2019. There was a huge downward spike during the pandemic, but the recovery put us right back on trend. Starting in 2021, however, participation grew well above trend.

Perhaps it grew too much. Perhaps employers have been more reluctant this time around to replace workers with automation. But that's not likely to last. For the first time in quite a while I saw a movie on Sunday and there were no ticket sellers at all. The entire process at our local gigantic multiplex was handled by touch screens. Fast food restaurants are moving in the same direction. The eventual result is going to be fewer workers but a return to normal productivity growth.

This is our long-term future and we can't avoid it except for short periods here and there. We're apparently in one of those periods now, but we'll probably return to trend before long. That means some pain in the employment rate, which the Fed seems determined to make even worse, but eventually a return to normal labor participation and productivity rates.

As you know by now, the FBI conducted a search of Mar-a-Lago, Donald Trump's Florida home, on Monday morning. For some reason, everyone assumes that they were looking for boxes of documents that Trump should have turned over to the National Archives but instead took with him when he left office.

That makes no sense. This was something that happened 18 months ago, and anyway, the Archives retrieved those boxes earlier this year. The FBI was obviously looking for something else.

But what? Nobody knows, but the reaction of Democrats and Republicans was nearly unanimously polarized:

Democrats: It takes a lot for a judge to approve a warrant like this. It's got to be something pretty serious.

Republicans: This is obviously a political motivated attack by the Department of Justice. Needless to say, Trump himself led the charge on this interpretation of events.

Now, I don't think this is politically motivated in any way. I'm not a huge fan of the FBI, but they have a long-time reputation for being a pretty conservative organization. What's more, Trump himself appointed the current head of the FBI.

On the other hand, I'm not so sure that judges require all that much convincing to approve an FBI warrant. Nor do I put it above the FBI to cut a few corners. They've certainly done it before.

I wouldn't be too surprised if the FBI's conduct wasn't entirely righteous, but I'd be very surprised if it was politicized in any serious way. As for what it was all about, we'll just have to wait and see.

I'm bored. It's dex night and I can't sleep but I have nothing to do. I'd like to play with my telescope but it's too cloudy even for testing.

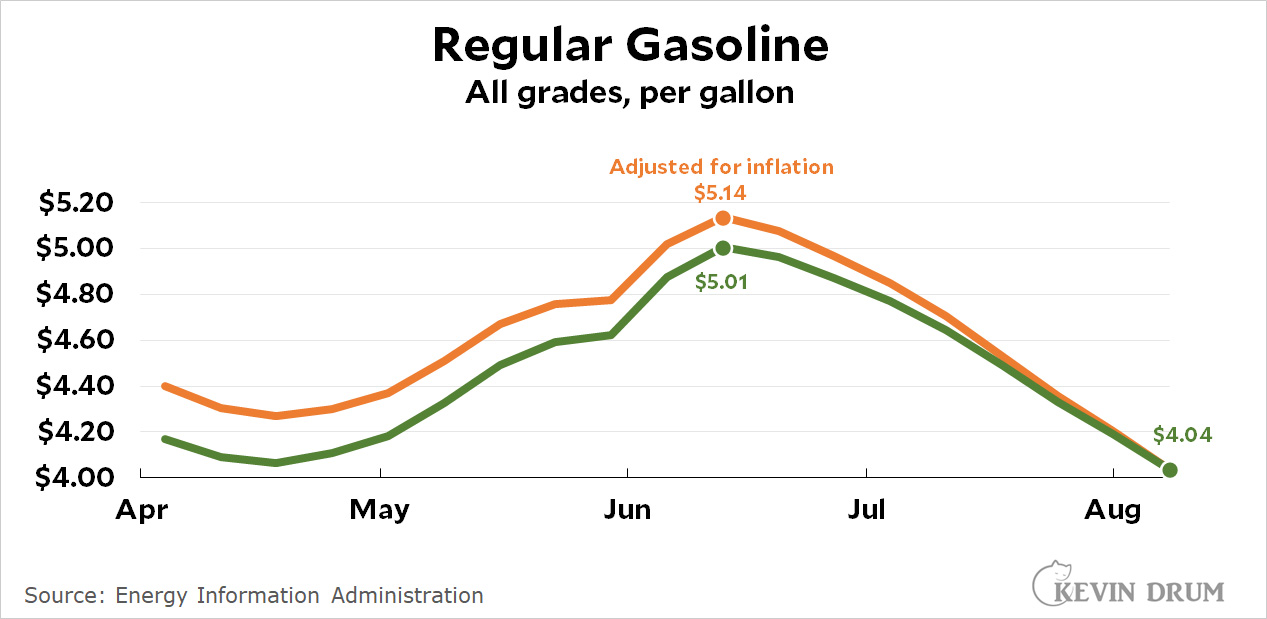

So how about if we update our gasoline price chart? It annoys conservatives, so it's worth doing:

The price of gasoline just keeps going down, down, and then down some more. Why? Because the price of oil has dropped about 25% since its June peak and gasoline is following along. It still has a ways to go to catch up, though, so we should continue to see gasoline prices decline for at least another week or two.

This is a long-tailed Pea-blue butterfly captured in our front yard a few days ago. It is a member of the gossamer winged family, and according to Wikipedia it is common in Europe, Africa, South and Southeast Asia, and Australia. Notably missing from this list is our entire hemisphere, let alone Southern California.

So maybe I have this wrong? Perhaps it's a butterfly that bears a striking resemblance to a Pea-blue, but is actually something else? Anyone care to chime in on this?

UPDATE: Rob Modic emails to say that this is almost certainly a Marine Blue, which is very common in Orange County.

One of the ways that the new climate change bill¹ raises money to pay for itself is by hiring more IRS agents to audit rich people. This will make up for the massive drop in audits of the rich that's been engineered by Republicans over the past decade.

Markowitz says that he has “never understood the fear of an IRS audit.” Given that he is an IRS-enrolled agent — that is, that he makes his living representing taxpayers in front of the IRS — this should perhaps not be too surprising.... “Don’t lie,” he suggests. “How about just don’t cheat on tax returns?” But this, of course, misses the point. I do not “cheat” on my tax return, and I never have. I don’t “lie,” either. But I’m still terrified of the IRS. Why? Because the process of being audited — especially in-person, which this funding will increase — is an absolute nightmare.

OK, sure. No one looks forward to an IRS audit. But the new funding is strictly for audits of the rich. The commissioner of the IRS—a Trump appointee—says the new money will be used only to increase the audit rate of people making more than $400,000 per year. These are the kind of people who have legions of accountants to handle their taxes. There's no fear involved except the fear of possibly having to pay all the taxes they owe.

But this is the bit I found the funniest:

One suspects that, in any other circumstance, this [fear] would be intuitively obvious. Suppose that, tomorrow, the FBI announced that it intended to begin “auditing” millions of people to find out if they had committed any federal crimes....

But this is precisely what the IRS did back in the '90s. As part of a deal over the Child Tax Credit, Newt Gingrich demanded a higher audit rate of EITC recipients, who are almost exclusively part of the working poor. As I recall, Republicans were all for it.

Bottom line: Cooke has nothing to worry about unless National Review pays a lot better than I think. The people who ought to be worried are the rich, but they cheat on their taxes in very abstruse ways and have no reason to be viscerally afraid of audits since most of them never see an IRS agent in the first place. For the rich, audits are just dreary, formal negotiations between opposing lawyers in mid-Manhattan conference rooms. They get occasional reports from their accountants while they relax on their private beaches in the Bahamas, and that's about it.

¹Can we all start calling it this? I'm a Democrat, and even I can't stomach calling it the Inflation Reduction Act.