Tyler Cowen takes a look at the housing market . . .

. . . and concludes that we didn't really have a housing bubble in the early aughts. Prices have now returned to their 2006 height, which suggests that the big price runup was mostly based on fundamentals with just a little bit of bubbly mixed in.

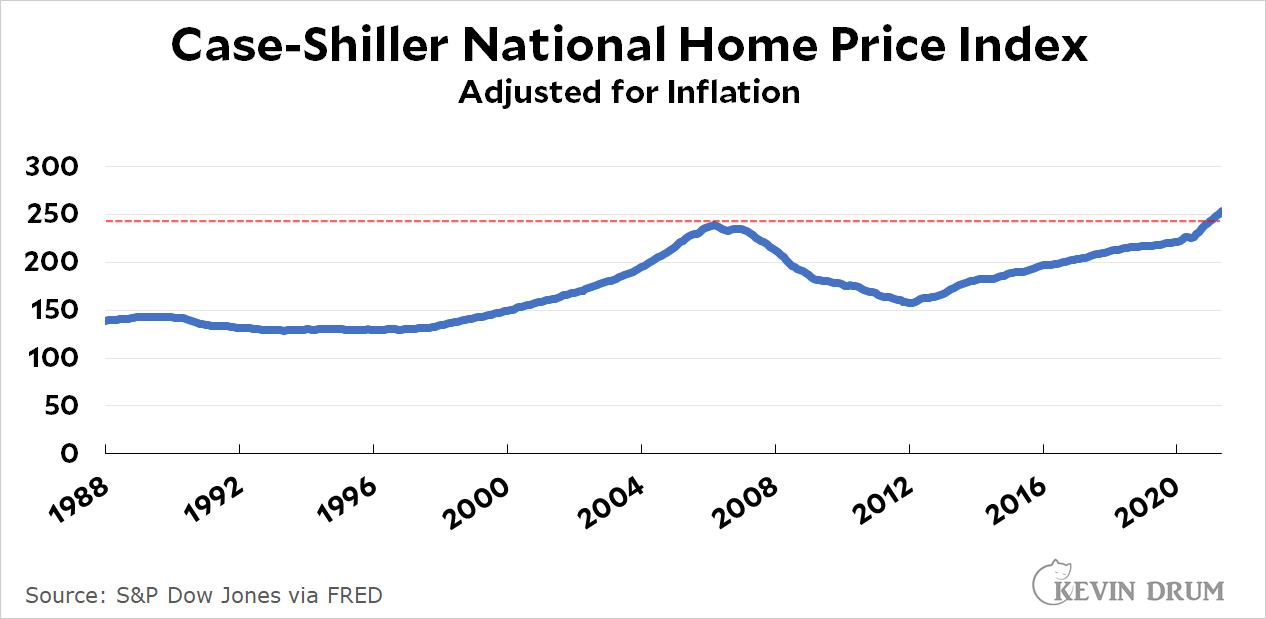

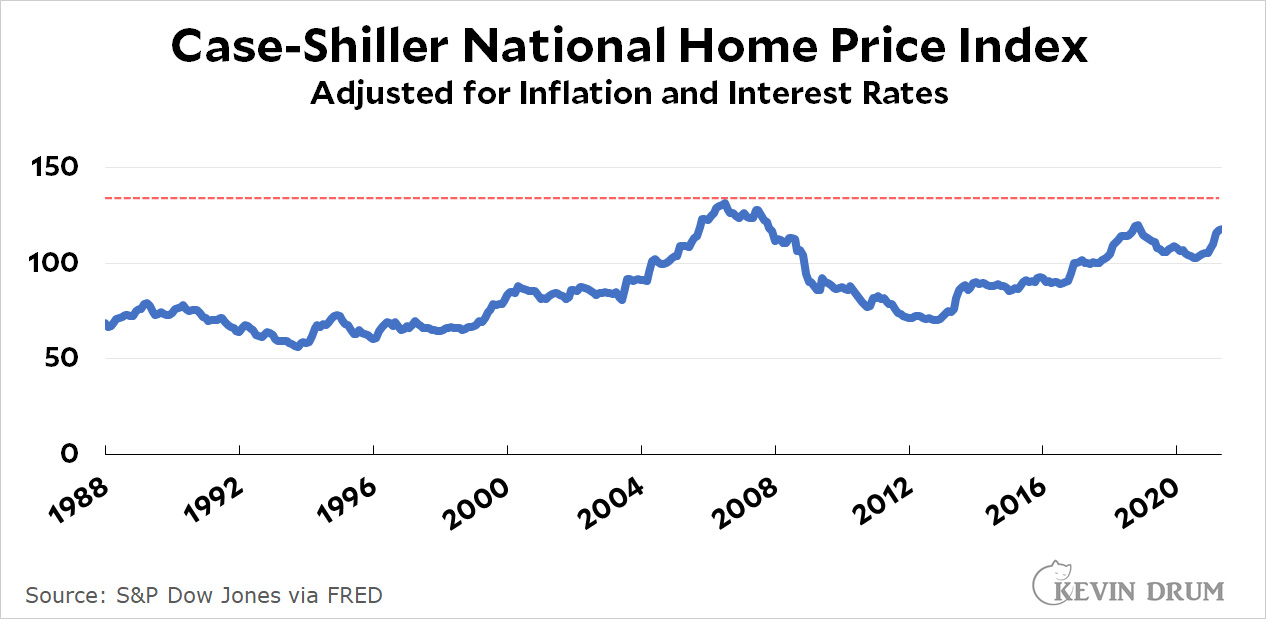

Maybe! Let's take a look at two other things before we decide. First, here's the home price index adjusted for mortgage interest rates, which have declined steadily for the past 20 years:

On average, this represents what people actually have to pay each month, which is more important than the raw house price. As you can see, we aren't yet at the level of 2006.

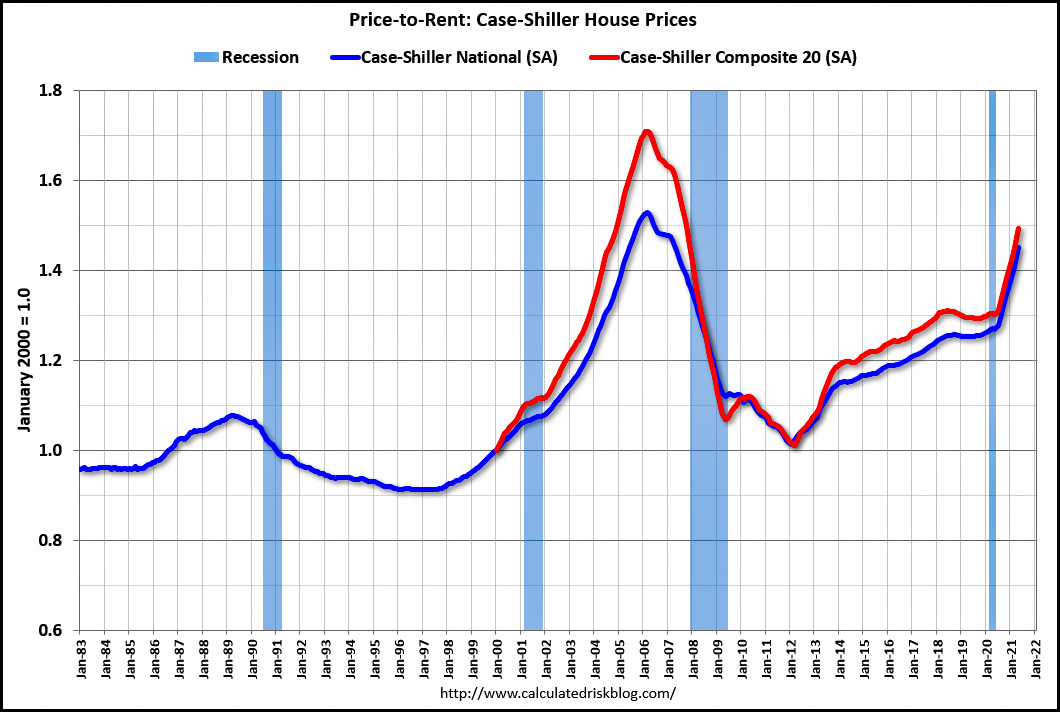

Second, I've always been sort of addicted to the price-rent ratio as one of the best signs of a housing bubble. Via Calculated Risk, here it is through May of this year:

We're getting close to the 2006 peak, but we're not there yet. (Not through May, anyway.) Still, a price-to-rent ratio this high sure seems kind of bubbly to me, and I wouldn't be surprised if the big spike starting in 2020 is COVID related, not fundamentals related.

So . . . who knows? When you adjust for both inflation and interest rates, we're still below the 2006 bubble peak. On the other hand, over the past 18 months there's been a spike that does look kind of bubbly. If I had to guess, I'd say (a) 2006 was a bubble, though perhaps more driven by fundamentals than we thought at the time; and (b) we weren't in a bubble up through 2020, but we might be in one now.

Of course, the pandemic will end eventually and—presumably—housing pressure will continue to grow until it reaches a point that we start building enough houses to serve the market again. If we do, then house prices will either go down or stabilize. This will depend a lot on whether young buyers continue to lust after houses in urban markets that are likely to stay tight or if they finally give up and start looking at mid-size cities that have more scope for home building.