Normally it takes a couple of days to settle payments in the banking system. But no longer. Later this month the Federal Reserve is introducing FedNow, which allows instant payment settlement 24 hours a day. Are you ready for the 20-minute 4 am bank run?

In addition to losing revenue from the time between a payment’s initiation and settlement, banks now have to worry about deposit flight outside of business hours. It comes just months after three major lenders failed in part because of rapid withdrawals and an inability to tap emergency sources of cash that were offline.

The March banking-sector crisis suggests cash can leave far quicker than bankers assumed, said Noor Menai, chief executive of Los Angeles-based lender CTBC Bank USA. Social media and smartphone apps allowed customers to withdraw deposits at a rapid clip, ultimately leading to a series of bank runs.

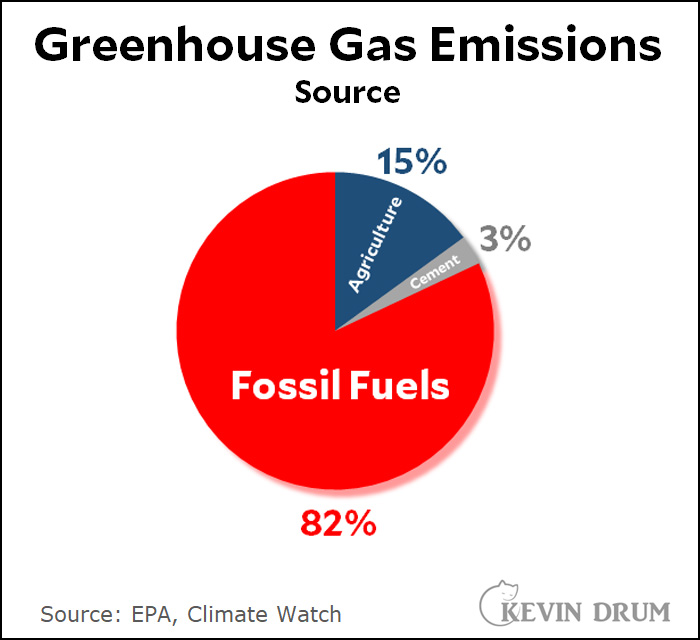

This chart shows total US greenhouse gas emissions—nearly all of it CO2 and methane—for the past two decades by sector:

Emissions peaked in 2007 and have fallen 12% since then, due almost exclusively to the fact that we've cut our use of coal-fired power plants in half.¹ These coal plants have largely been replaced by renewables, which are carbon-free, and combined-cycle gas-fired plants, powered by fracked natural gas, which emit about half as much CO2 per kWh of electricity generation as coal.

¹Industry has also gotten about 10% more energy efficient.

I know that M2 as a measure of money supply isn't taken too seriously these days, and M2 as a cause of inflation even less so. But last night I got curious about the sources of our recent inflation. Is it exclusively a result of reduced supply and increased demand brought on by the pandemic? Or is there also a traditional Friedmanesque monetary component?

As you can see in the chart, M2 surged in the early '70s and was followed a couple of years later by high inflation. Then it surged again in the late '70s and was followed yet again a couple of years later by even higher inflation. For the next 40 years things bounced around a bit, but basically both M2 growth and inflation growth were moderate.

Then, in 2020, M2 skyrocketed at a growth rate far beyond anything in the past. Sure enough, nearly two years later inflation followed.

The big difference between now and the '70s is that past surges lasted a couple of years and then slowly faded away. Our current surge spiked in a single year and then plummeted like a rock. M2 growth has actually been negative for the past year.

If M2 is still tied to inflation, this suggests that inflation is not just headed down, but potentially headed way down as pandemic shortages fully ease and M2 follows a steep downward trajectory. But then again, maybe it isn't. I don't know.

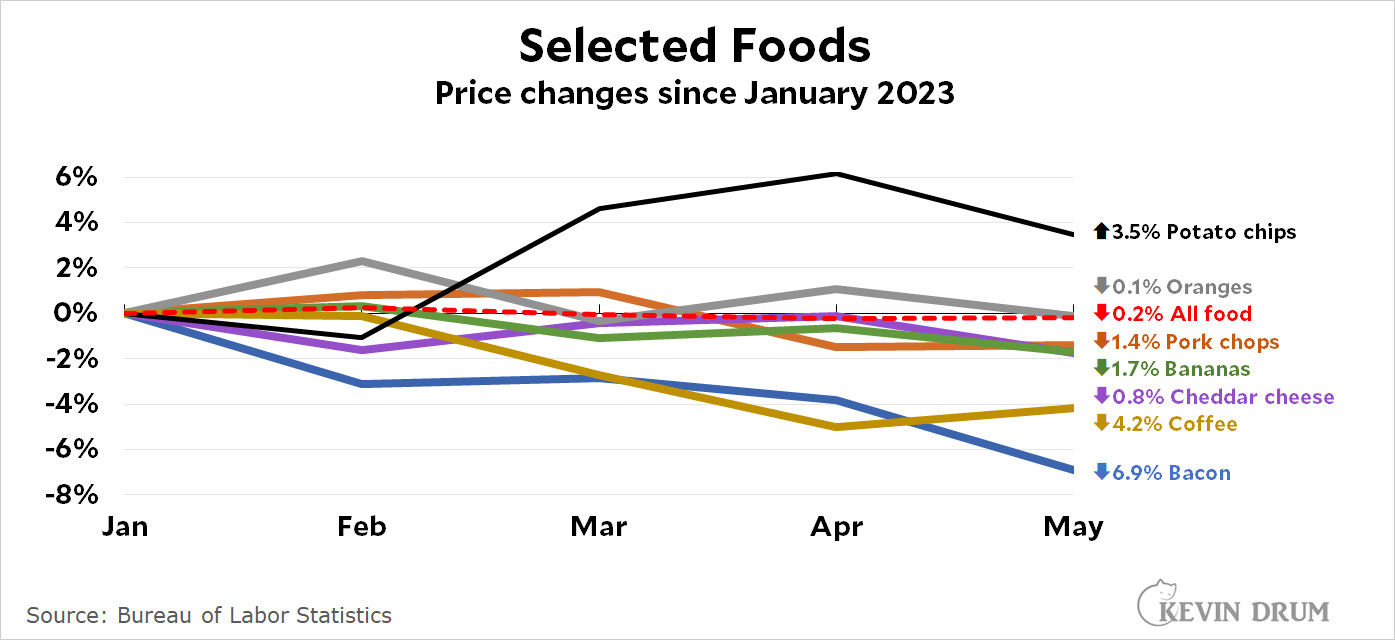

The Supermarket Aisle Where Prices Are Still Soaring

They're talking about highly processed foods like potato chips—which, in fact, are up only 3.5% since January. Not precisely soaring. And they admit that inflation has eased elsewhere.

What they don't admit is that food inflation is gone. Since the start of the year, the overall inflation rate for food at home is below zero. In some cases, prices have very noticeably dropped. So why not a story about the supermarket aisle where inflation hasn't just eased, but prices have declined since the beginning of the year? For example:

Since the start of the year food prices have gone down. Not just flattened. Gone down. Why are there no blaring stories about that?

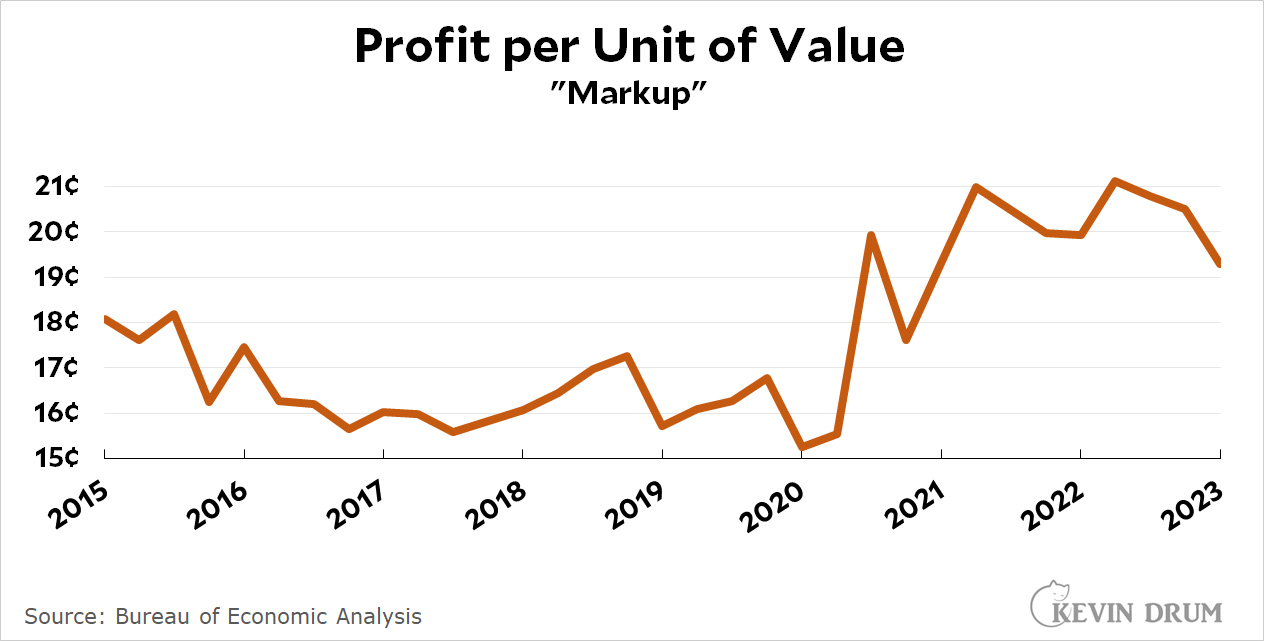

As we all know, corporations have raised prices substantially over the past couple of years, generating huge windfall profits. Is this "greedflation" the real cause of our recent bout of inflation?

Corporate price markups shot up temporarily at the very start of the pandemic and then abated when the initial shock was over. But then they rose again and stayed high, coinciding with the start of inflation. Why?

In a nutshell, Eric Levitz says no. All that happened is that the pandemic caused supply shortages while government stimulus payments kept demand high, which caused prices to rise. Corporations then went along for the ride. I think this is broadly correct, but not entirely. After all, the evidence suggests corporations didn't just go along for the ride. They increased prices well beyond the rate of inflation. Was that related to lack of competition?

This raises an obvious problem: Corporate concentration has been transpiring over decades. In 2019, U.S. industries were roughly as concentrated as they were in 2022. Yet in the former year, inflation sat near 2 percent, a low level by historical standards. In the latter year, by contrast, prices rose by 6.5 percent. So why did corporate concentration yield historically low inflation throughout the 2010s, only to suddenly produce exceptionally high inflation following the pandemic?

Indeed. If they could get away with this, why wait for the pandemic?

It is unclear why corporations would feel compelled to wait for an “excuse” before seeking to maximize their profits....Generally speaking, companies do not feel compelled to provide an excuse for pursuing their mercenary interests....U.S. firms have been perfectly happy to offshore jobs to low-wage areas, even in the absence of an economic crisis that would serve to rationalize such profit-maximizing endeavors. Pharmaceutical firms, meanwhile, routinely price-gouged on life-saving medicines, even when inflation was near historic lows.

I think there's a straightforward answer to this question of timing. During periods of low inflation, price increases are conspicuous and consumers react to them. Big, flashy price increases run the risk of consumers abandoning your product and substituting something else.

But when the economy is chaotic and inflation is already high—and consumers are faced with endless news coverage of it—these constraints ease. If inflation is running at 8% and everyone is panicking, it's barely noticeable if a bag of Cheetos goes up 8% or 17%. It just seems like yet another wild price increase, like eggs or beef or used cars experienced for a while. At the same time, there's little risk of your prices being undercut, not because of corporate concentration but because everyone else is suffering supply shortages at the same time.

So my take is simple: Our current round of inflation is fundamentally a result of pandemic shocks, but it's been made a little worse by greedflation. This stands in stark contrast to the usual bogeyman of labor costs, which have been rising at less than the rate of inflation. In other words, it's not that greedflation isn't real—it is—it's just that it's a modest part of the whole story. That's how companies are able to get away with it, after all.

I am three months away from qualifying for Medicare and everything is going smoothly. HHS already sent me a card, and a couple of days ago Kaiser Permanente sent me a signup form that looks like just what I want. But there is a weird little mystery that I can't figure out. Here is the Kaiser description of benefits for two plans, the standard HMO and the Value HMO:

There's not much difference. But the standard HMO is better: It has no inpatient hospitalization copay and the annual out-of-pocket is $1,000 less. Now here are the plan prices:

They are the same: $0. I don't suppose anyone cares much about this. Even I don't care much about it. But it seems awfully peculiar. Why bother having two plans that are close to identical in the first place? And if you do, shouldn't you charge more for the better plan? What's going on here?

With the harvesting of wood expected to increase dramatically in coming decades, researchers are warning that policy officials have woefully underestimated logging’s carbon footprint....Between 2010 and 2050, global demand for wood is expected to surge 54%....During that time, greenhouse gas emissions from wood harvests would significantly increase, likely releasing 3.5 billion to 4.2 billion metric tons of carbon dioxide each year.

Estimates vary a bit, but here are the basic stats on greenhouse gas emissions:

The wood researchers are estimating an increase of 0.7 billion metric tons of CO2 out of a total of 50 billion that the world currently emits. That's barely more than 1%. It's trivial.

There are two, and only two, things we should be seriously concerned about if we want to rein in climate change:

Fossil fuels

Carbon capture

We need to focus on fossil fuels because that's the whole mozilla. We need to focus on carbon capture of some kind because we can't reach our climate goals merely by reducing emissions. Everyone agrees that we need a lower concentration of greenhouse gases than we have now.

But is there any harm in pointing out other contributors to climate change? Agriculture in general is certainly #2. The problem is that being peppered by constant news coverage of this kind is a dangerous distraction. People hardly need more excuses to focus on more congenial but basically ineffective solutions to climate change. As hard as it is, we need to be focused like a laser on fossil fuels as the only thing that truly matters.

It's either that or geoengineering. Those are our choices.

Among all Americans, 4.5% of deaths are due to opioid overdoses, mostly fentanyl

Among the youngish middle-aged (20-39), 21% of all deaths are due to opioids.

Among men in this age group, 30% of all deaths are due to opioids.

Now, part of the reason the percentage is so high among the youngish is that not many people of that age die in the first place. The basic mortality rate is only 0.25%, so that 21% death rate from opioids amounts to only 0.05% of the population.

But that's still 21% of all deaths in that age group and that's still a remarkable number.