The NHTSA reported statistics today on crashes of self-driving cars over the past year. The numbers are all but useless, but here they are anyway:

Tesla leads the pack among Level 2 cars, which have limited self-driving capability. Among cars with higher levels of automation, Waymo is by far the highest.

But in neither case do we know how many miles these cars have driven. Tesla and Waymo have almost certainly driven far more automated miles than anyone else in their respective categories, and I suspect both would have pretty low numbers if you calculated crashes/mile—or, more crudely, even crashes/vehicle.

But we don't have that unless the car companies provide that information for the relevant time period. In the meantime, this is all the NHTSA has.

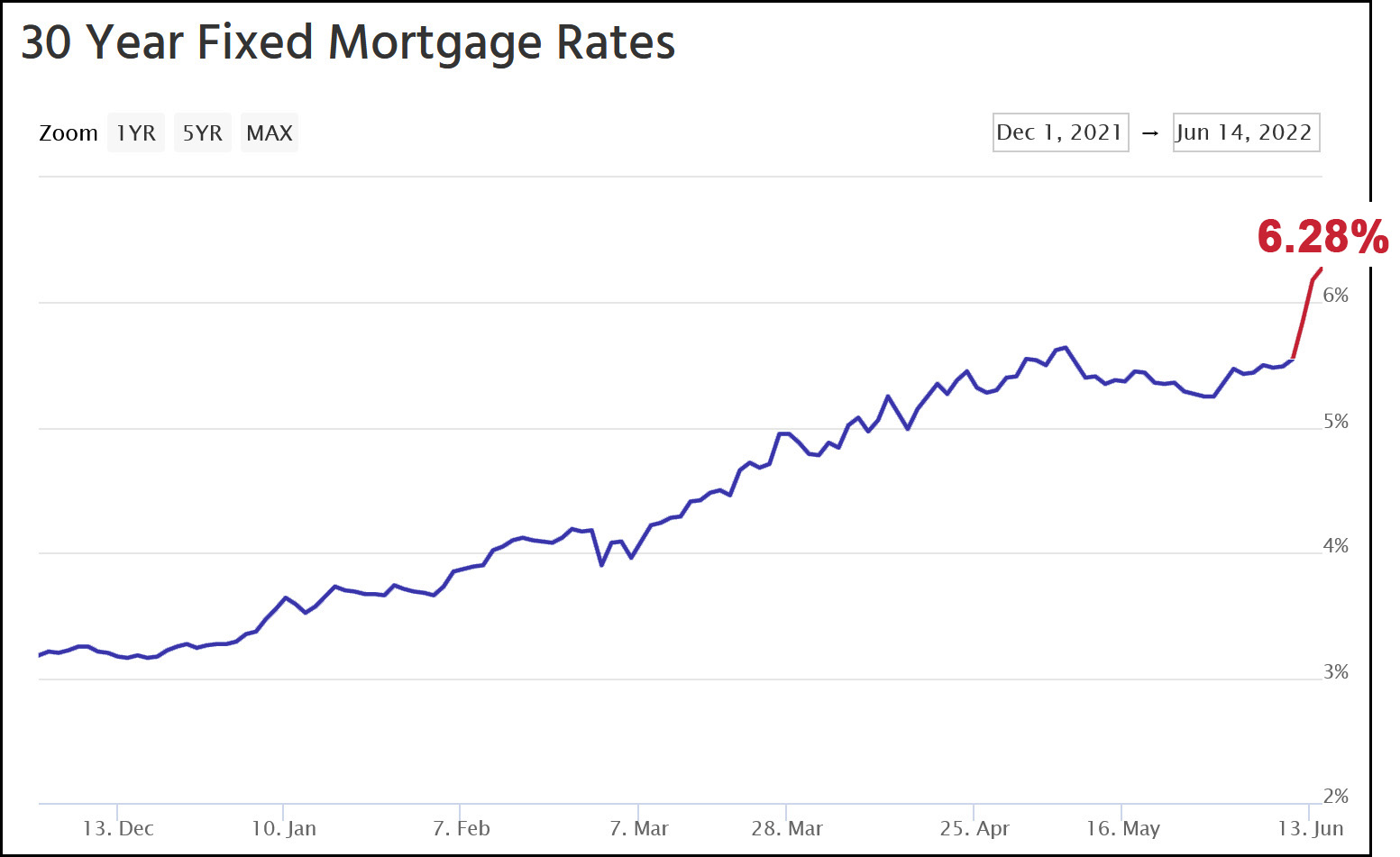

If Mortgage News Daily is to be believed, the interest rate on a 30-year fixed mortgage has jumped 0.73% over the course of just three business days. Since the start of the year rates have nearly doubled, from 3.29% to 6.28%.

So what happened on Friday to cause mortgage rates to suddenly jump? That was the day inflation numbers were released, so I suppose it was that. Bankers probably figured that continuing high inflation would prompt the Fed to raise rates sharply and this in turn would make their cost of money higher.

Or maybe there's some other three-bank-shot theory at work here. Long-term inflation expectations (5/10/30 year) have been either flat or down over the past few weeks, so that's not the answer.

In any case, this will add yet another $100 or so to the average monthly mortgage payment, and this in turn will depress the housing market. That's bad news for the economy.

This is the Irvine Spectrum shopping center, a vast and growing conglomeration of all the usual mall suspects.

As you can see, the photo was taken at sunrise via drone. After this I have one more drone picture to show you: the one that prompted me to finally buy a drone in the first place. Maybe next week.

The share of homes listed for sale that took recent price cuts has more than doubled since last year. During the four weeks that ended June 5, 16.2% of listings in L.A. County had at least one price cut, up from 7.5% during the same period last year, Redfin data show.

In Orange, Riverside and San Bernardino counties the share of price drops rose to more than 20% of listings, up from about 7% a year earlier.

Nationwide, there haven’t been this many price cuts since 2019. Homes for sale in Los Angeles and Orange Counties haven’t seen this number of price reductions since late 2018 — the last time mortgage rates shot up. In the Inland Empire, price reductions are at an all-time high in a dataset that started in 2015.

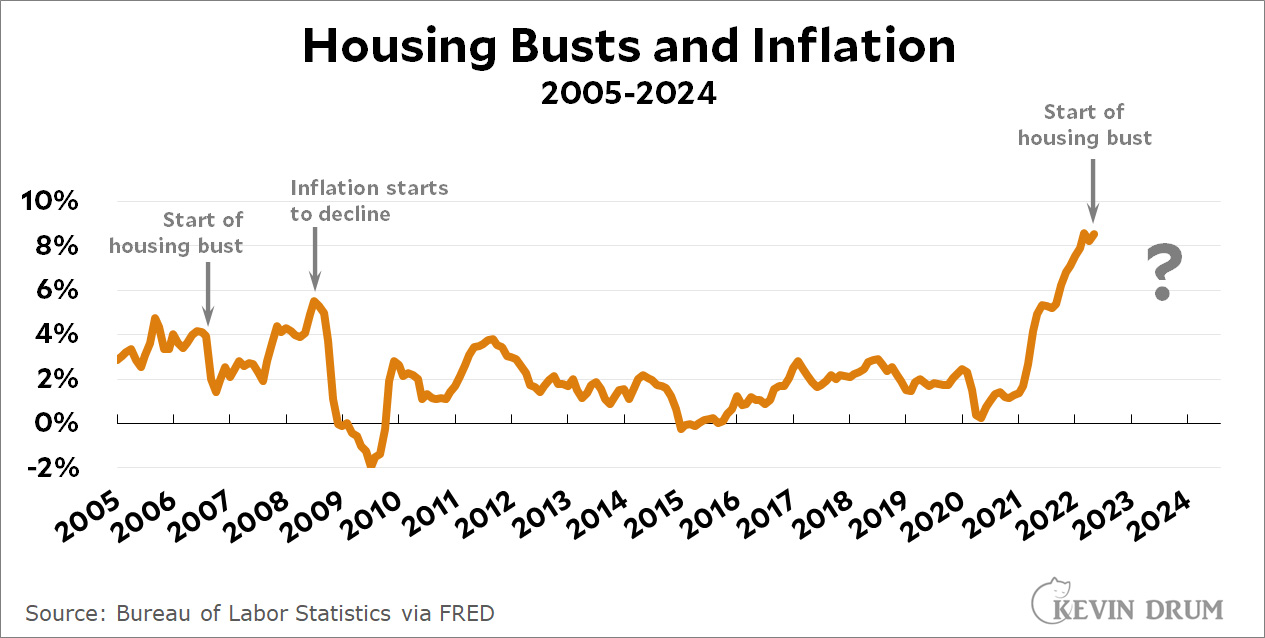

Realtors are bravely saying that there are still plenty of eager buyers and plenty of bidding wars. And it's true that housing prices continued to rise through March—the latest data available. But this is just the start. I don't expect a housing bust on the order of 2006-2008, but I do expect a sustained moderate drop in house prices. In aggregate, this decline is likely to shave half a point or more off GDP growth—and that's in addition to all the other headwinds facing the economy.

It will also bring down price levels—although judging from our experience during the Great Recession it's hard to say how long it will take for it to work its way through to lower inflation rates:

Our last housing bust was followed by a quick decline in inflation, but the decline was small and temporary. It was two years before inflation was seriously affected.

So what will it be this time around, with different circumstances and a smaller fall in housing prices? If I knew, would I still be doing this free blogging thing?

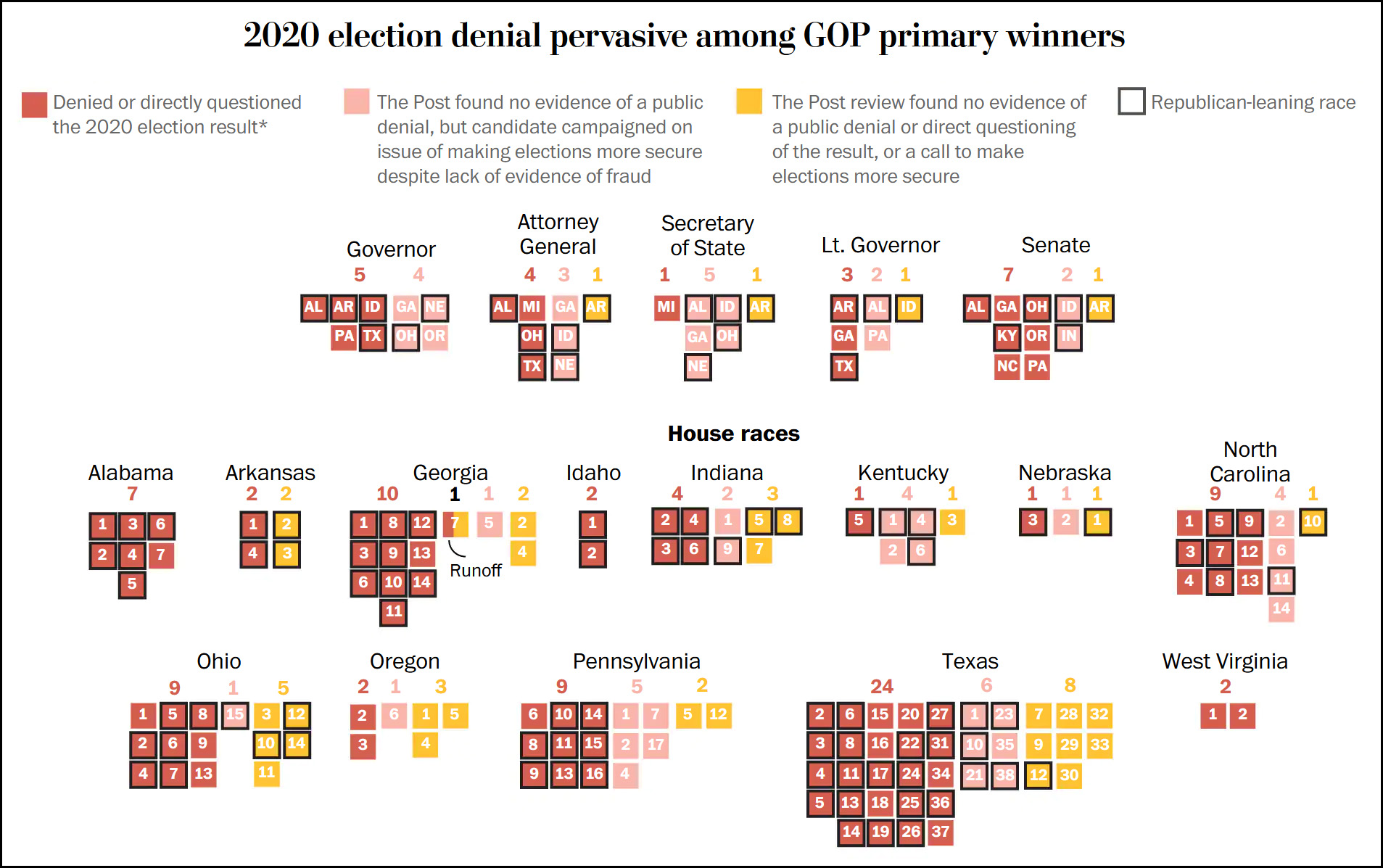

The Washington Post reports today that Republican voters are eager to nominate candidates for office who repeat Donald Trump's big lie about the 2020 election being stolen:

District by district, state by state, voters in places that cast ballots through the end of May have chosen at least 108 candidates for statewide office or Congress who have repeated Trump’s lies. The number jumps to at least 149 winning candidates — out of more than 170 races — when it includes those who have campaigned on a platform of tightening voting rules or more stringently enforcing those already on the books, despite the lack of evidence of widespread fraud.

Here's the chart:

This is obviously a terrible trend. Make no mistake.

But. It's also worth noting that virtually every one of these candidates comes from either a deep red state or a red district within a purplish state. In other words, they come from places where Republicans are likely to win anyway and no elections will even need to be overturned. Congressional races are a little different, but even there very few of these districts would ever nominate someone who wasn't willing to go along with a vote to install Trump as president if the vote ever ended up in the House.

In practical terms, then, these nominations won't change much of anything. It's disheartening that so many Republicans have gone over this cliff edge, but the truth is that they went over it many years ago. This is just the latest manifestation of Gingrichism, Foxism, Tea Partyism, and now, Trumpism.

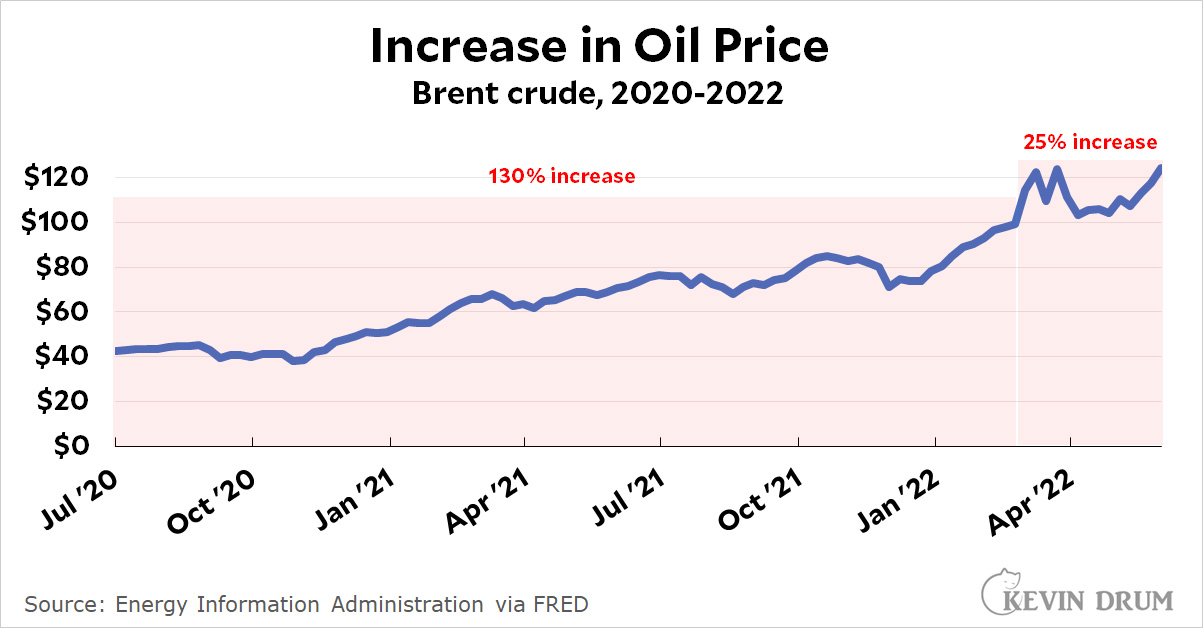

Here is the price of Brent crude over the past couple of years.

The price of Brent crude dipped at the start of the pandemic and then started recovering. This is far before the Ukraine war. The price mostly recovered by July 2020, which is where I start my chart, and then rose 130% ($60) by January 2022. After the Ukraine war started, the price increased another 25% ($25).

In other words, the Ukraine war is not the primary cause of high oil prices (and hence high gasoline prices). It just added a bit to a price that had already been soaring for a long time.

Quite so. The only surprising thing about Grim's account is that it took so long for someone on the left to write it. The widespread revolt of young staffers, especially in the nonprofit space, is the subject of endless talk within the progressive movement, but you'd never know it on the outside because it's been written about only in bits and pieces that never quite add up to a full story. Grim is the first to put the whole thing together without (very much) defensiveness or punch pulling.

The clash Grim describes between workers and management has been brewing for a while—since the election of Donald Trump, at least—but took off in earnest only after the 2020 murder of George Floyd by Minneapolis police. Staffers at progressive nonprofits, in a game of follow the leader, all began issuing demands, writing manifestos, and declaring that the organizations they worked for were hopelessly misogynistic, classist, white supremacist, and, inevitably, "unsafe." These revolts were eerily similar, and they drove management nuts:

At the ACLU, as at many organizations, the controversy quickly evolved to include charges that senior leaders were hostile to staff from marginalized communities. Each accusation is unique; some have obvious merit, while others don’t withstand scrutiny. What emerges by zooming out is the striking similarity of their trajectories. One foundation official who has funded many of the groups entangled in turmoil said that having a panoramic view allowed her to see those common threads. “It’s the kind of thing that looks very context-specific, until you see a larger pattern,” she said.

....Inner turmoil can often begin, the managers said, with performance-based disputes that spiral into moral questions. “I also see a pattern of … people who are not competent in their orgs getting ahead of the game by declaring that others have engaged in some kind of -ism, thereby triggering a process that protects them in that job while there’s an investigation or turmoil over it,” the foundation official added. Such disputes then trigger broader cultural conversations, with battle lines being drawn on each side.

Unsurprisingly to anyone who has any experience with progressive organizations, this problem may have its roots in social justice but it's been weaponized by technology:

Twitter, as the saying goes, may not be real life, but in a world of remote work, Slack very much is.”

In the past, workers gathered around the water cooler to air their gripes to each other. Today it's an endless barrage of Slack conversations, Twitter feuds, and Zoom meetings. All of these are things that can reach out to far more people than will fit around a water cooler, and they can be used relentlessly and effortlessly by a generation that takes to them naturally. Managers fight perpetual rear-guard battles, but because progressives tend to be highly verbal people this generally leads only to more and more talk:

[Months after Joe Biden's inauguration] most of the foundation-backed organizations that make up the backbone of the party’s ideological infrastructure were still spending their time locked in virtual retreats, Slack wars, and healing sessions, grappling with tensions over hierarchy, patriarchy, race, gender, and power.

....“I got to a point like three years ago where I had a crisis of faith, like, I don’t even know, most of these spaces on the left are just not — they’re not healthy. Like all these people are just not — they’re not doing well,” [a senior manager] said.

....The environment has pushed expectations far beyond what workplaces previously offered to employees. “A lot of staff that work for me, they expect the organization to be all the things: a movement, OK, get out the vote, OK, healing, OK, take care of you when you’re sick, OK. It’s all the things,” said one executive director. “Can you get your love and healing at home, please? But I can’t say that, they would crucify me.”

Could the Heritage Society come up with a better scheme for eviscerating their progressive foes?

Another leader said the strife has become so destructive that it feels like an op. “I’m not saying it’s a right-wing plot, because we are incredibly good at doing ourselves in, but — if you tried — you couldn’t conceive of a better right-wing plot to paralyze progressive leaders....Progressive leaders cannot do anything but fight inside the orgs, thereby rendering the orgs completely toothless for the external battles in play.”

One of the biggest problem with all this is that it prompts progressive orgs to fight back against conservative orgs not with the messages most likely to win people to their side, but with maximal left-wing arguments that just scare people off. Young staffers insist on it, and management, who are supposed to be the adults in the room, have neither the power or the fortitude to rein them in and manage.

Even worse, this is all happening at a time when conservatives have become complete lunatics. It should be a golden age for progressives, who have the chance of a lifetime to make huge strides in the political arena. Instead we've gotten weaker. That's a hell of an indictment when you're competing against a conservative movement headlined by the likes of Donald Trump, Tucker Carlson, Kevin McCarthy, Ron DeSantis, and Steve Bannon.

This progressive war of all against all has long since become intractable and unwinnable. Is there anybody on our side who commands the moral authority and widespread respect to put us back on track?¹

¹Actually, there is: Barack Obama. It's a shame that he's virtually abandoned both the Democratic Party and the progressive movement since stepping down as president.

A string of troubling inflation reports in recent days is likely to lead Federal Reserve officials to consider surprising markets with a larger-than-expected 0.75-percentage-point interest-rate increase at their meeting this week.

Before officials began their premeeting quiet period on June 4, they had signaled they were prepared to raise interest rates by a half percentage point this week and again at their meeting in July.

I hope they don't do this. First, these "surprise" moves are never surprises because they're always telegraphed in advance. Second, the latest inflation report wasn't that bad. It showed a plateau in headline CPI, not a new resurgence of rising prices, along with a continuing decline in core CPI.

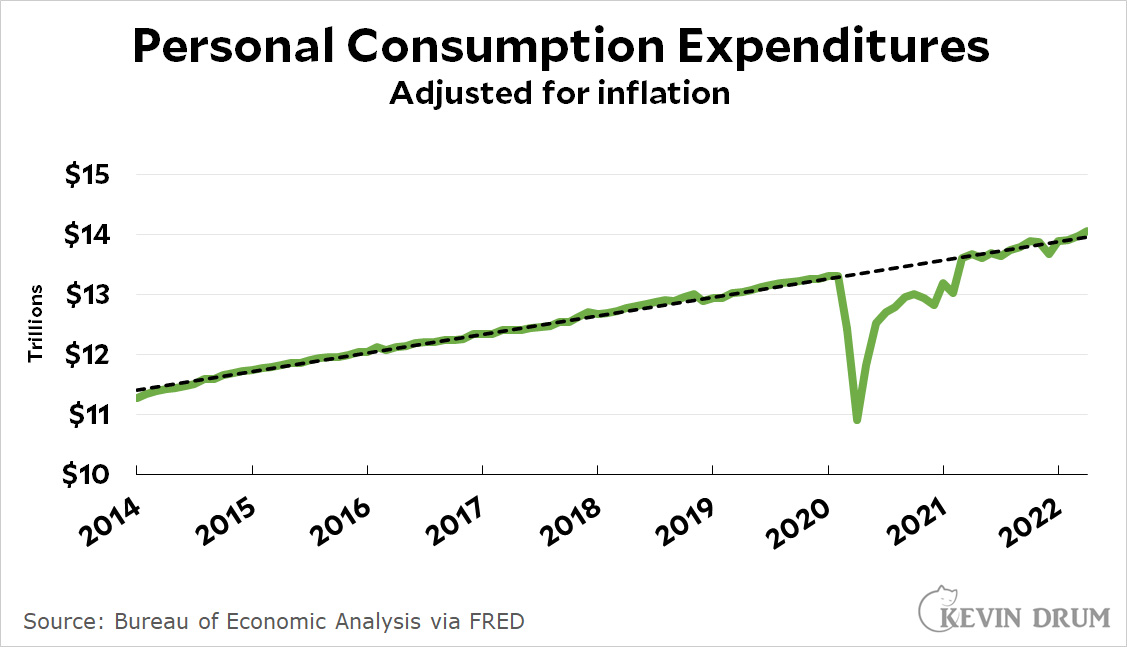

What's more, there are several good reasons to think the economy is going to slow down without any extra help: (1) the Fed is already raising interest rates and slowing asset purchases, (2) the Biden stimulus will fade out in the second half of the year, (3) the housing market is likely to pop thanks to mortgage rates above 5%, (4) personal savings have dropped back to pre-pandemic levels, (5) consumer debt has increased to nearly its historical average, (6) real consumer spending hit its pre-pandemic level in early 2021 and has been rising at normal historical rates ever since, and (7) supply chain problems are easing and will probably continue to ease.

And there's one more thing: Milton Friedman's famous long and variable lags. For fiscal policy, like Biden's stimulus, it takes time for the money to get spent and then a while longer for the spending to affect the economy. In other words, we should expect its peak effects right about now, followed by a steady decline. Monetary policy also takes a while to affect inflation and economic growth. The bright side of this is that Fed action probably won't dampen growth right away. The dark side is that it will dampen growth in 2023—and are we sure we're going to want that when 2023 finally rolls around?

Inflation is likely to subside over the rest of the year and the Fed really shouldn't panic over it. All that does is panic everyone else in a time when the Fed should be demonstrating stability and restraint. Beyond that, we certainly don't need to throw the economy into a recession just because that's what Paul Volcker did in 1980. Today's economy is nothing close to what Volcker faced.

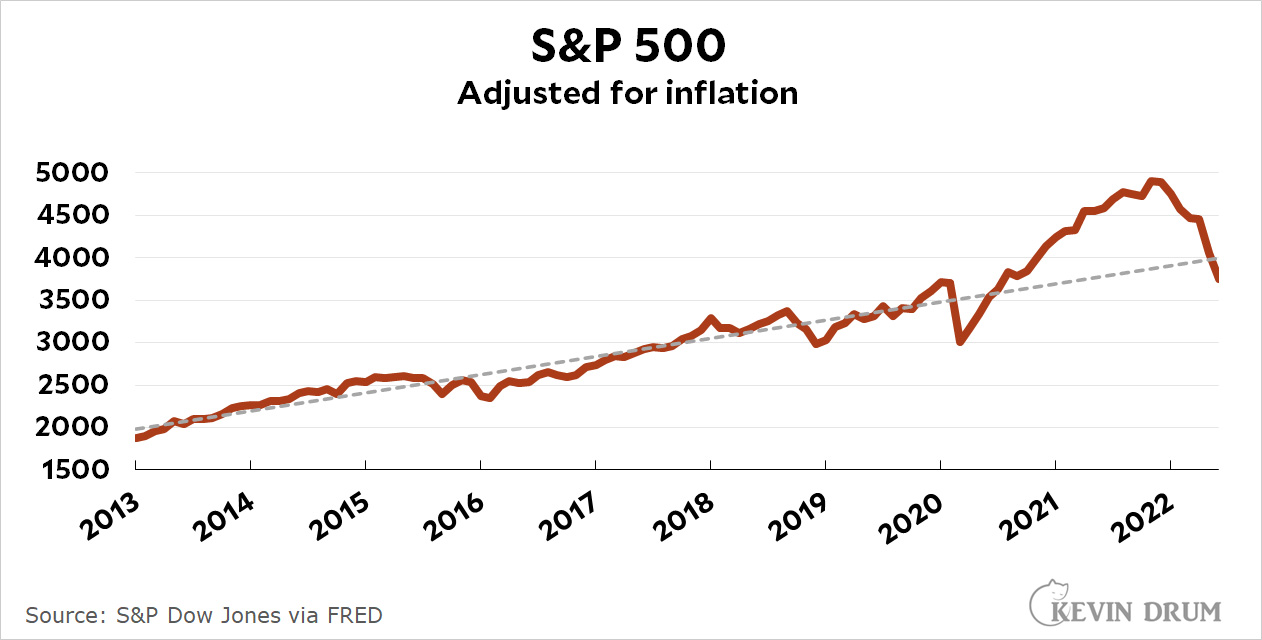

There are two things about this chart that are different from most of the ones you see. First, I adjusted the S&P index for inflation. This doesn't usually make a huge difference, but if you're looking at price levels over a long period of time—or during a period of high inflation—it's best to go ahead and adjust.

Second, I ran my favorite trendline through the raw numbers. As usual, it's based on data only through February 2020 and then extended to the present. It shows you where the S&P 500 would be if there had been no pandemic and the market had just kept rising at its post-recession rate.

The answer is that it would be about where it is now. It's corrected for the weird boom of 2021 and nothing more. So far.

That may change, especially if the Fed overreacts to inflation. For now, though, it doesn't look all that scary except to people who bought at the peak of the 2021 bubble.

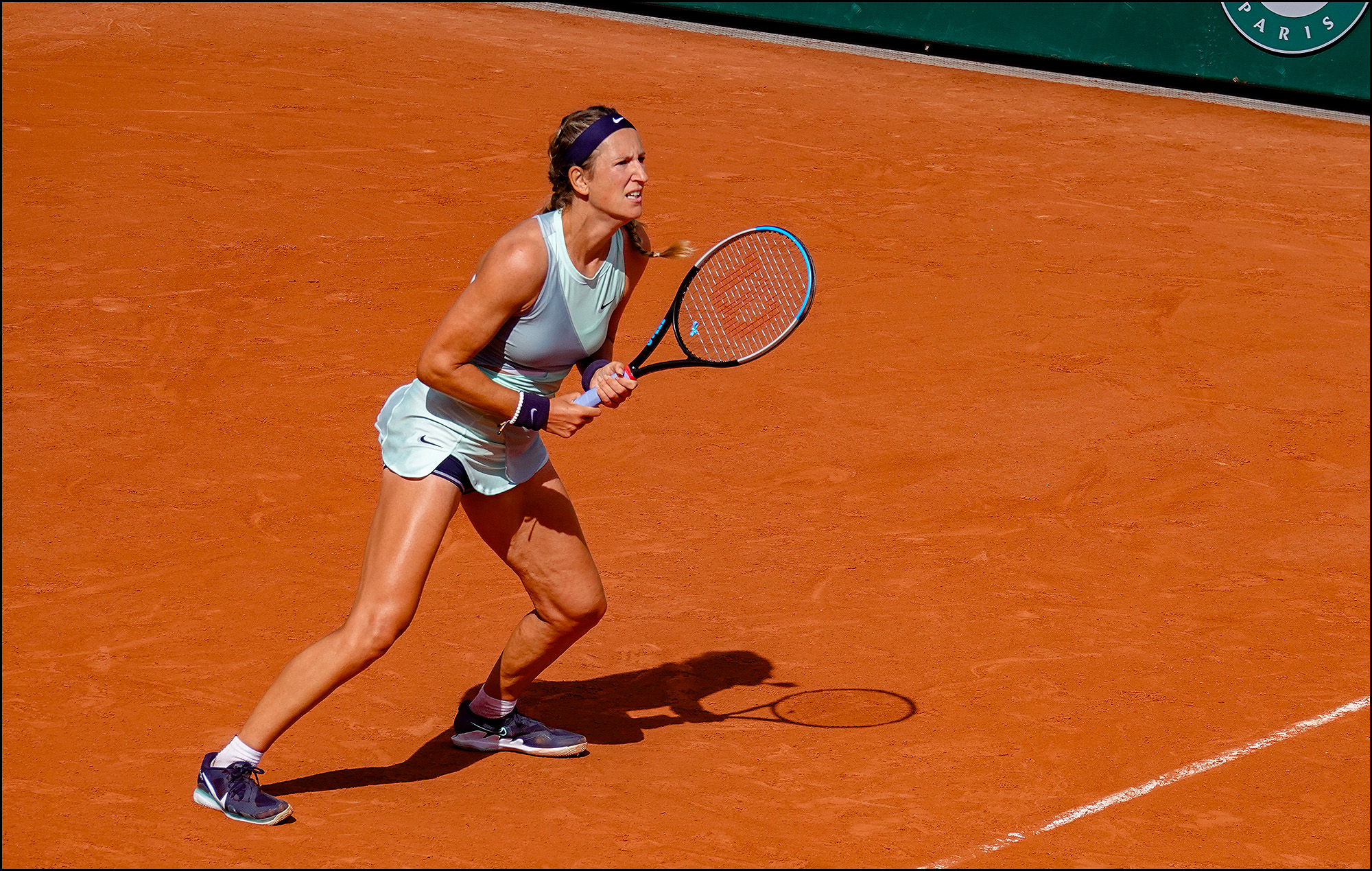

The top picture shows Victoria Azarenka playing at this year's French Open. A decade ago Azarenka was ranked #1 in the world but then suffered through some injuries and afterward took time off for the birth of her son. She never regained her top form after that and was ranked 15th going into Roland Garros.

The photo was taken during Azarenka's third round match against Jil Teichmann of Switzerland, who was ranked 24th at the time. Teichmann, at bottom, won in the third set.

Tesla leads the pack among Level 2 cars, which have limited self-driving capability. Among cars with higher levels of automation, Waymo is by far the highest.

Tesla leads the pack among Level 2 cars, which have limited self-driving capability. Among cars with higher levels of automation, Waymo is by far the highest.