The Fed minutes for their June 14-15 meeting were released today, and they explained why the Fed took such aggressive action on interest rates:

“The near-term inflation outlook had deteriorated since the time of the May meeting,” the minutes said. “Participants were concerned that the May CPI release indicated that inflation pressures had yet to show signs of abating, and a number of them saw it as solidifying the view that inflation would be more persistent than they had previously anticipated.”

This was all because four days earlier the BLS announced that CPI had clocked in at 8.6% in May. This was splashed across front pages everywhere as "the biggest increase since 1981."

But guess what? The media freakout was based on a CPI figure of 8.58% compared to 8.54% two months earlier. Some record. And that was for headline CPI using the non-seasonally adjusted figures. Using the more normal seasonally-adjusted figure, it wasn't a record at all. (March was.) And using the even more relevant core CPI figures, May represented the second month in a row of declining inflation.

And of course that's CPI, which the Fed claims not to care much about. They care about the core PCE rate. At the time of their meeting, the core year-over-year PCE rate had declined since February from 5.3% to 5.2% to 4.9%. And although they didn't know it, a few days later it would decline again to 4.7%.

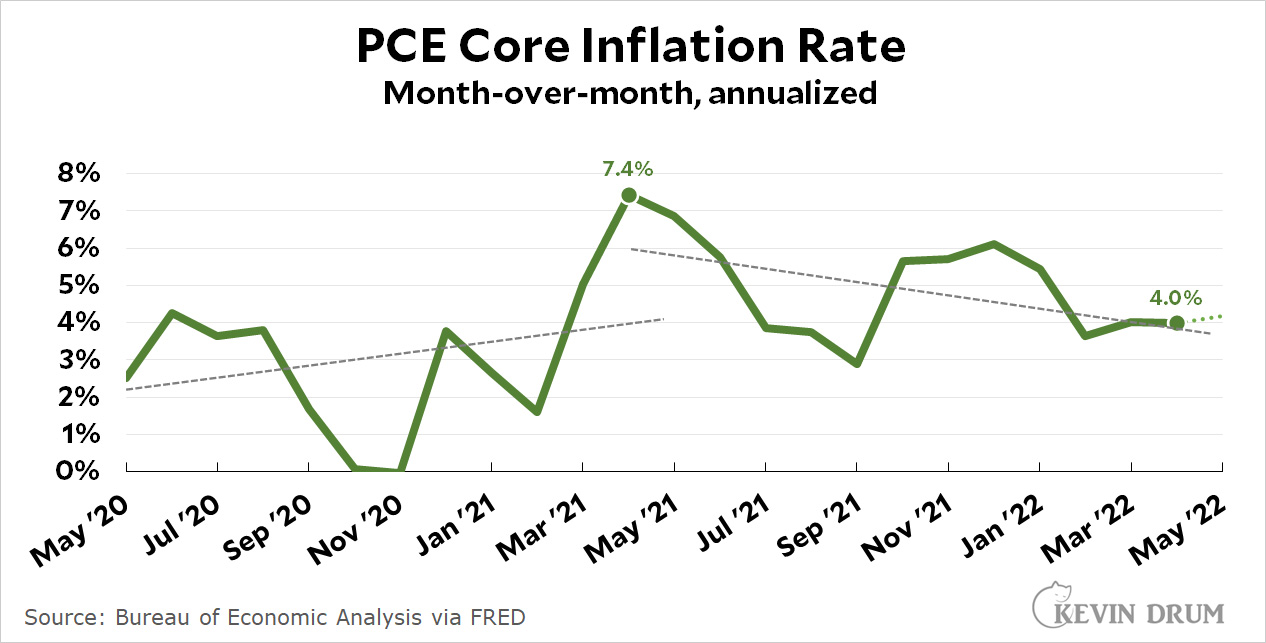

And then there's the momentum of the month-over-month rate, which looked like this:

The April figures were the latest the Fed had available at their meeting, but the trend was clear regardless: since its peak a year ago it had been dropping steadily, going from 7.4% to 4.0%. That's a big and sustained downward movement.¹

The April figures were the latest the Fed had available at their meeting, but the trend was clear regardless: since its peak a year ago it had been dropping steadily, going from 7.4% to 4.0%. That's a big and sustained downward movement.¹

You can always find something worrisome if you look hard enough. But there's a whole lot of evidence that inflationary pressures are abating. You have to look pretty hard to find something contradictory—like, say, a single month of headline, non-seasonally-adjusted CPI. The stuff that counts—trends, core inflation, PCE—all show declines.

IANAE and I might be all wet on this. But the evidence sure looks awfully clear to me. Just about every relevant measure is showing some welcome softening in inflation. And looking beyond the core, gasoline is now in its third week of declining prices (down yet another ten cents last week). This leaves food as our biggest remaining problem, but that's largely due to bad crops, war in Ukraine, and natural gas prices causing a big spike last year in fertilizer costs (but which have been softening since March). That will all work itself out eventually, and in the meantime there's nothing the Fed can do to speed it along.

¹When the May result was released it came in at 4.2%. But this is a volatile measurement and a small change in a single month doesn't mean much.