Brad DeLong has a new book out called Slouching Towards Utopia, an economic history of the "long 20th century" from 1870 to 2010.

Brad DeLong has a new book out called Slouching Towards Utopia, an economic history of the "long 20th century" from 1870 to 2010.

Why 1870? Because Brad says that despite earlier progress stemming from the Industrial Revolution, it was only in 1870 that growth surged upward enough to affect the incomes of the common man. This created a whole new world. The causes of this surge in growth were globalization, industrial research labs, and modern corporations.

Fine. But why 2010? This is a little less clear, but Brad mostly puts it down to the failure of neoliberalism—made plain by the Great Recession—and the failure of American politics with the election of Donald Trump.

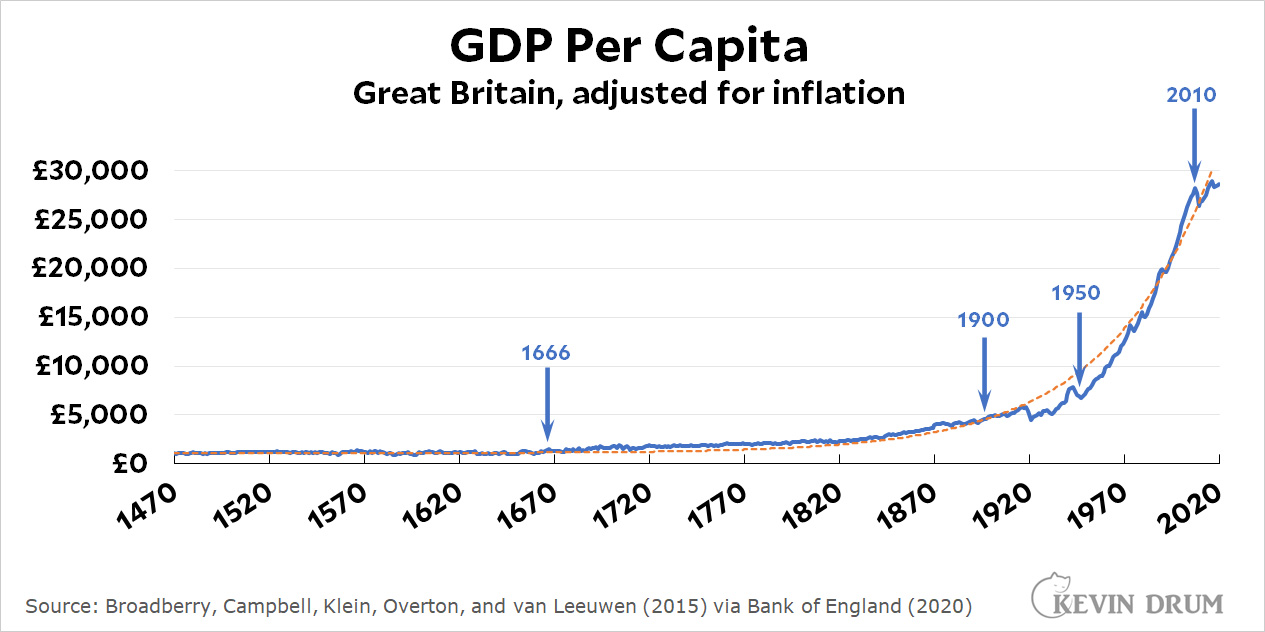

But I have a problem with this. The Industrial Revolution began in Great Britain, so that's the country it's most important to look at. Let's do that. Here is per capita GDP in Great Britain:

The blue line is actual GDP. The dashed orange line is a simple exponential curve that fits Britain's growth closely for the past 500 years.¹ To my mind, it means this: as long as Great Britain is on the orange curve, it's just being Great Britain. For whatever reason, this is the level of growth they produce just by doing their thing.

The blue line is actual GDP. The dashed orange line is a simple exponential curve that fits Britain's growth closely for the past 500 years.¹ To my mind, it means this: as long as Great Britain is on the orange curve, it's just being Great Britain. For whatever reason, this is the level of growth they produce just by doing their thing.

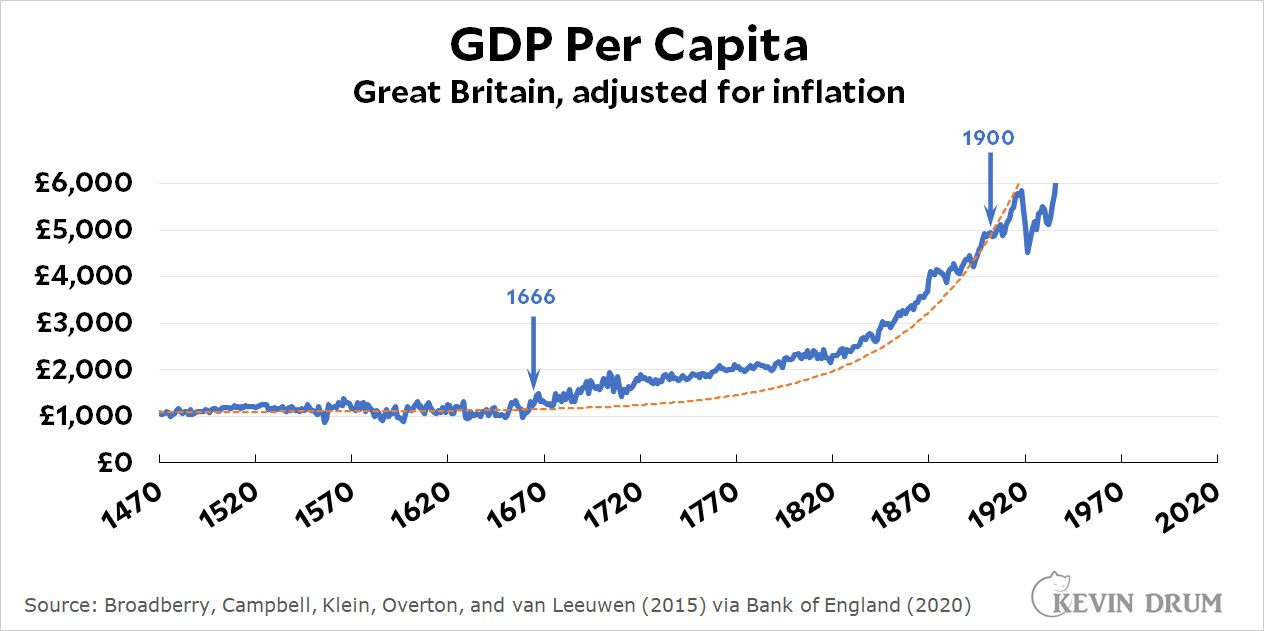

Now here's a closer look at the period from 1470-1900:

Between about 1666 and 1900, growth was higher than the orange curve. And even within that period, there are two sub-periods that stand out: 1666-1720 and 1820-1870. Then, looking at the top chart, there's another period of strong growth from about 1950-2010. Those were the real periods of super-strong growth.

Between about 1666 and 1900, growth was higher than the orange curve. And even within that period, there are two sub-periods that stand out: 1666-1720 and 1820-1870. Then, looking at the top chart, there's another period of strong growth from about 1950-2010. Those were the real periods of super-strong growth.

Here's how I interpret this: Nothing unique happened in 1870. Great Britain was just following its normal growth path year after year—with a few smallish deviations here and there. In the 17th century this produced GDP high enough to support a growing urban craft class but did little for ordinary workers. By the late 19th century GDP finally reached a point where (a) workers started demanding a bigger share of the pie and (b) capitalists were rich enough that they could afford to meet workers' demands without any real hardship.

In any exponential growth curve there's always a knee in the curve where it suddenly seems like things have changed. This is because an absolute increase from £1,000 to £1,100 is not nearly as impressive as an increase from £4,000 to £8,000 even if they represent exactly the same level of growth. And in this case they do: the growth of per capita GDP in Great Britain was largely the same for 500 years with the exception of only a few short periods. There was nothing special about 1870, and without that the thesis of the whole book becomes rickety.

Apologies if I've bored you with this, but it's a necessary technical preface to some more substantial thoughts about the book. I'll have more about that later.

¹In case you're curious, the equation of the curve is 1.018(Year -1440) + 1100. For example, for the year 2000 this comes out to 1.018560 +1100 = £21,815 + 1100 = £22,915. Actual GDP per capita for that year was £24,402.