Over the past few days, a million pundits have become instant experts on the finances of Silicon Valley Bank. They are outraged that no one before now noticed the bleeding obvious: SVB was a reckless and fragile bank, a literal time bomb on the edge of collapsing thanks to foolish business practices.

Now, 20/20 hindsight is great, but I've been digging into this for days and I just don't buy the narrative. I'm not saying SVB is faultless, but I am saying it was basically a sound bank facing some modest headwinds. Which they were addressing.

I have receipts for all this. They are mostly based on three documents:

Let's dive into the big issues surrounding the collapse of SVB.

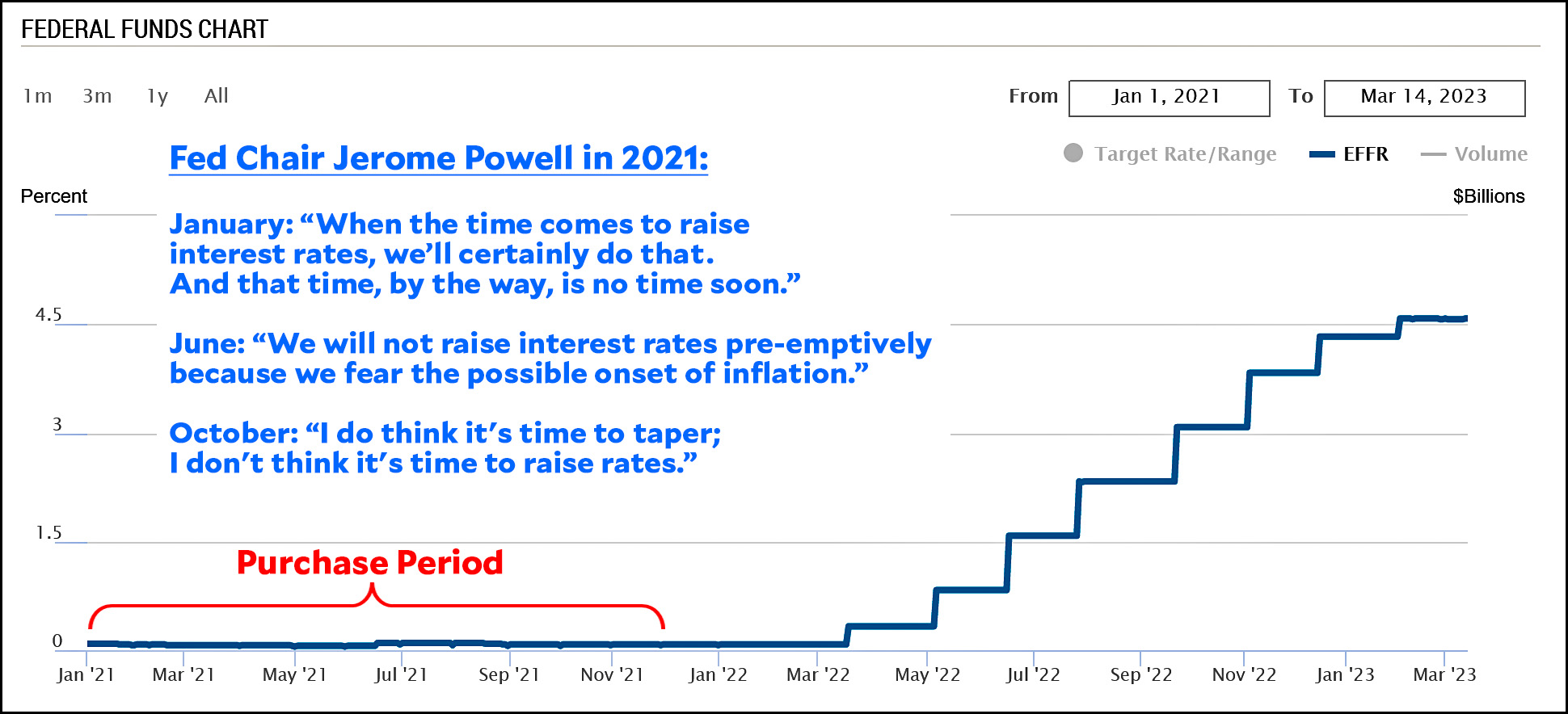

The bond portfolio. SVB had about $90 billion invested in long-dated treasury and mortgage bonds. This portfolio was vulnerable to interest rate risk, and SVB probably should have hedged that. However, keep in mind that nearly the entire portfolio was purchased in 2021:

At the time, there was little reason to think interest rate risk was high. There was certainly no reason to think that Jerome Powell would turn on a dime and not only raise rates, but raise them at an astronomical rate. And anyway, all of the bonds were marked as Hold to Maturity, which meant their losses never showed up on SVB's books and probably never would have.

At the time, there was little reason to think interest rate risk was high. There was certainly no reason to think that Jerome Powell would turn on a dime and not only raise rates, but raise them at an astronomical rate. And anyway, all of the bonds were marked as Hold to Maturity, which meant their losses never showed up on SVB's books and probably never would have.

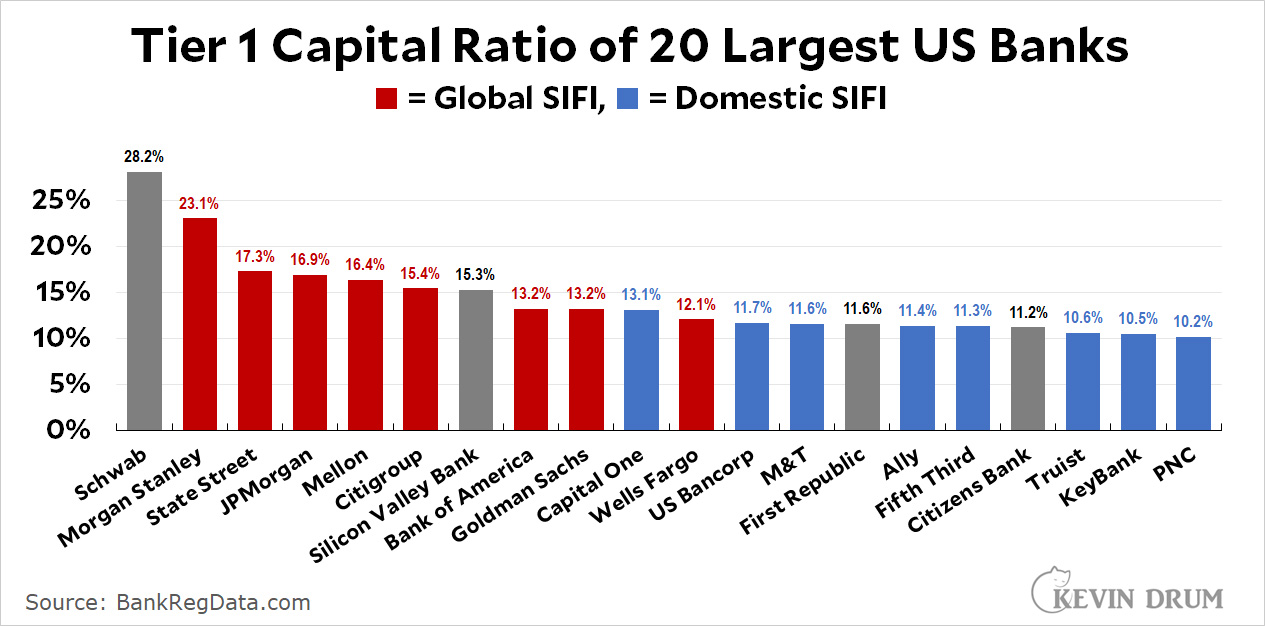

The 2018 deregulation. As best as I can tell, this had no effect at all on SVB. Most of the loosened regulations didn't apply to SVB, and the ones that did would have had no effect because SVB was already capitalized as strongly as a global SIFI and had plenty of liquidity. Their Tier 1 capital ratio was 15.3%; their CET1 capital ratio was 12.2%; and their leverage ratio was 8%. Those are way above anything required by regulators both before and after the 2018 law was passed.

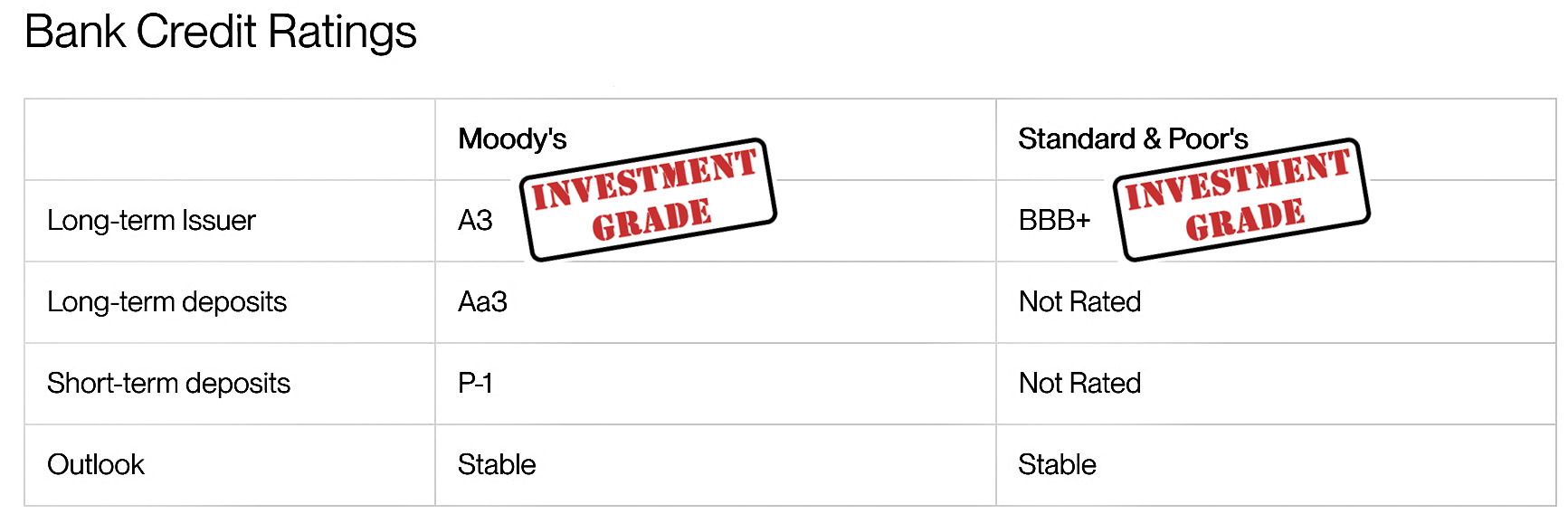

SVB's situation was absolutely not a secret. Maybe you and I didn't know about it because we didn't care, but it was well known to everyone who followed SVB. Their unrecorded losses produced a slight amount of nervousness, but that was all. Investors had no worries: after a big fall in 2022 when the tech boom slowed, SVB's stock was up nearly 40% since the start of the year. Analysts had no worries: they almost unanimously recommended SVB as a buy. Rating agencies had a bit of worry, but nonetheless rated SVB as investment grade.

SVB's situation was absolutely not a secret. Maybe you and I didn't know about it because we didn't care, but it was well known to everyone who followed SVB. Their unrecorded losses produced a slight amount of nervousness, but that was all. Investors had no worries: after a big fall in 2022 when the tech boom slowed, SVB's stock was up nearly 40% since the start of the year. Analysts had no worries: they almost unanimously recommended SVB as a buy. Rating agencies had a bit of worry, but nonetheless rated SVB as investment grade.

SVB responded properly. In response to concern from Moody's about the worsening outlook for the tech sector, SVB consulted with Goldman Sachs and then announced that it would sell $20 billion of its assets at a $2 billion loss and then do a $2 billion capital raise to make up for the loss. This was perfectly prudent. It gave SVB plenty of cash to handle deposit outflows, while diluting its stockholders a bit in order to keep its capital buffers high. Moody's downgraded SVB in response, but this was actually a vote of confidence. They had intended to downgrade SVB two notches, but after the restructuring plan was announced they limited the downgrade to one notch.

SVB responded properly. In response to concern from Moody's about the worsening outlook for the tech sector, SVB consulted with Goldman Sachs and then announced that it would sell $20 billion of its assets at a $2 billion loss and then do a $2 billion capital raise to make up for the loss. This was perfectly prudent. It gave SVB plenty of cash to handle deposit outflows, while diluting its stockholders a bit in order to keep its capital buffers high. Moody's downgraded SVB in response, but this was actually a vote of confidence. They had intended to downgrade SVB two notches, but after the restructuring plan was announced they limited the downgrade to one notch.

On the morning of Thursday, March 9, SVB was solvent and perfectly capable of servicing its customers. It had some long-term challenges, but nothing life threatening. It was fine.

So what happened?

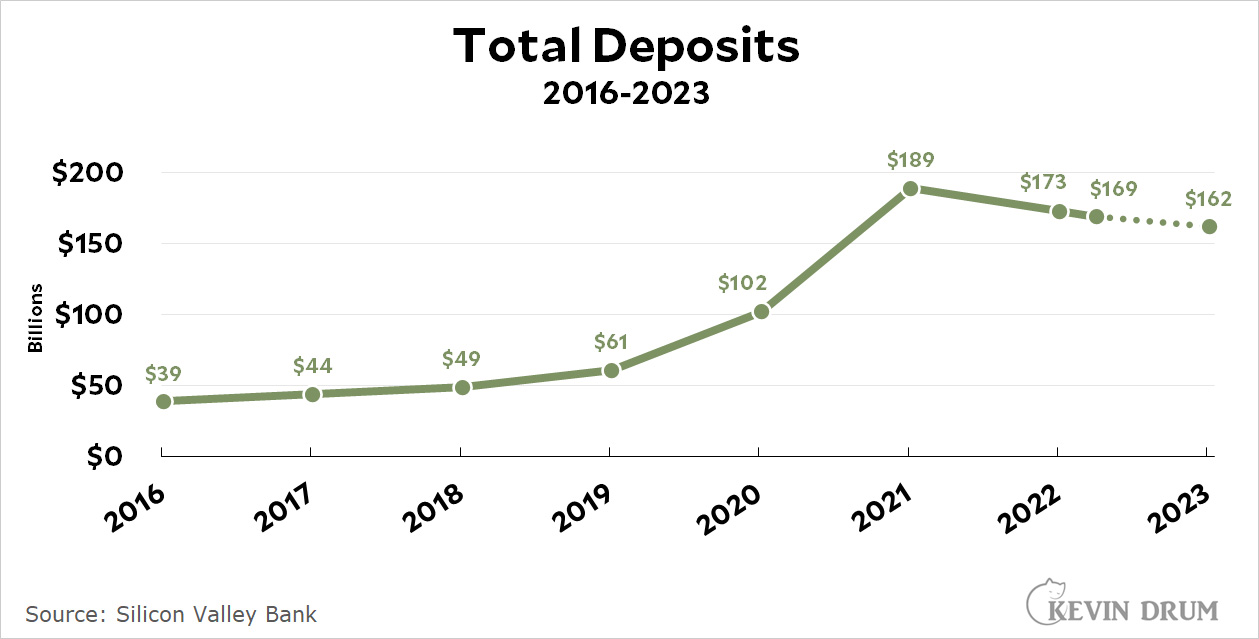

SVB really had only one problem: the pandemic had created a tech boom that saw the formation of hundreds of new startups. VC financing for all these startups flowed into SVB and spiked their deposit level from $61 billion to $189 billion.

In 2022, the tech boom went sour, and that meant no more startups and no more VC financing. As a result, existing startups had to pull money out of their SVB accounts to fund ongoing operations, and that led to a drop in deposits from $189 billion to $169 billion (as of March 8).

This was obviously concerning since SVB was heavily reliant on startup money. However, there was no reason to think that deposits would shrink anywhere near enough to actually jeopardize their solvency.

This was obviously concerning since SVB was heavily reliant on startup money. However, there was no reason to think that deposits would shrink anywhere near enough to actually jeopardize their solvency.

So what happened?

Nobody knows. Founders Fund, the venture capital fund co-founded by Peter Thiel, advised its companies on the morning of March 9 to withdraw their money from SVB. Why? We don't know for sure because neither FF's management nor Thiel are talking about what motivated them. Maybe they misread the Moody's downgrade. Maybe the capital raise spooked them. Maybe they heard some gossip that alarmed them. Or maybe it was nothing other than an excess of caution because they figured no harm would be done.

But Founders Fund is well known and influential, and news of what they had done spread around the Valley at light speed. Within a few hours, a $42 billion run had left SVB in ruins and the FDIC had taken over.

And now for a prediction: As more information unfolds and panic subsides, the FDIC will find out that SVB was not only solvent before the run, but even after it. Everyone will be paid in full and there will be money left over. The FDIC did the right thing regardless, since there's no stopping a run once it gets started, but there was never any good reason for it in the first place.

Mark that to market.