E.J. Dionne writes today about inflation. But I would like to dissent in part and concur in part. Here's what he says:

I was among those who did underestimate the immediate threat of inflation in early 2021, so I salute those (notably former treasury secretary Lawrence H. Summers) who warned us about what was coming....[But] at the risk of oversimplifying, inflation hawks examine our situation and see something approaching the situation of the 1970s: inflation roaring out of control and in danger of becoming embedded in the economy.

....But it’s not the 1970s anymore. Jared Bernstein, a longtime adviser to President Biden and a member of the White House Council of Economic Advisers, points to three big differences. First, the inflation of the ’70s was driven by big oil price shocks....Second, unlike now, unions were still strong in the 1970s.

....The third difference: The Federal Reserve has a much better understanding than in earlier years of the “underlying mechanisms of inflation.”

I concur with Dionne's basic thesis: Inflation hawks have spent the past 40 years warning over and over that liberal policies would send inflation spiraling, just like the 1970s, and for 40 years they've been wrong. But eventually we were bound to get a bout of inflation. Even if they were right this time, they're more like a stopped clock than a Swiss watch.

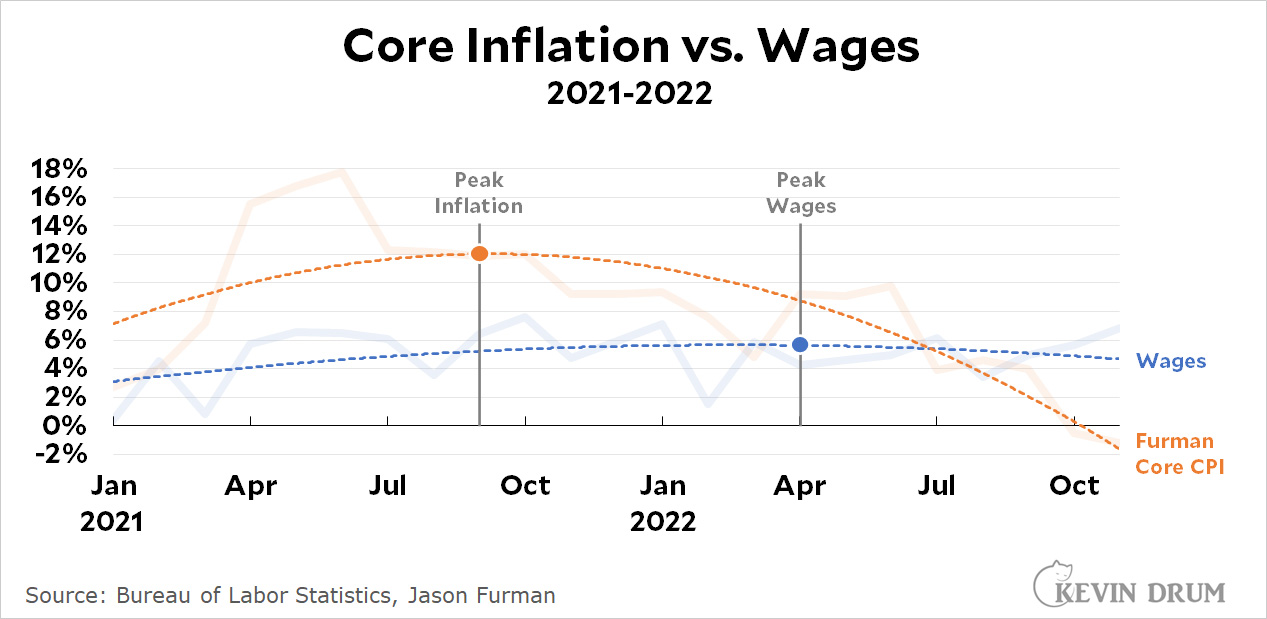

But I dissent from the rest. They weren't right. As time goes by and we get more data and a better sense of what that data means, inflation has started to look very different than we thought. Take a look at this chart:

It's a little complicated. Sorry about that. But the orange line shows Jason Furman's revised measurement of core inflation using actual rents instead of official BLS rent measurements that are six months out of date. What we now know is that rents skyrocketed in mid-2021 and core inflation was even higher than we thought. It hit 18% month-over-month in June of 2021!

It's a little complicated. Sorry about that. But the orange line shows Jason Furman's revised measurement of core inflation using actual rents instead of official BLS rent measurements that are six months out of date. What we now know is that rents skyrocketed in mid-2021 and core inflation was even higher than we thought. It hit 18% month-over-month in June of 2021!

But don't look at that. Look at the trendline. It's just a simple least-squares regression, so it's not rocket science. But it does a good job of smoothing the monthly data, and we now have figures for nearly two years to look at. Here's what it shows us: the trendline for modified core inflation peaked in September 2021 and then started declining.

Team Transitory was right all along. When you look at a better measure of core inflation, it peaked higher than we thought and sooner than we thought. It's been declining pretty steadily for the past 15 months.

As for wages, the blue line shows nominal hourly wage growth over the past two years. As you'd expect, it took a while for inflation to sink in and motivate people to demand higher wages. Its peak is seven months after the inflation peak. Wages are also more stable than inflation, so they're probably going to stay a little high for several more months, especially as workers want to make up for their losses of the past couple of years. But the trendline is still downward, and before very long it will follow the inflation numbers and drop even more.

So I dissent from the view that the inflation hawks were right. Thanks to the pandemic and its artificial rent controls, rents were a way bigger deal in our current bout of inflation than they were in the past.

By deliberately ignoring this—Larry Summers knew the rent data was wrong but pretended it meant the opposite of what it did¹—and by focusing on dumb metrics like year-over-year inflation that are practically designed to mislead in situations like this, we've spent the past year panicking over a delusive view of what's going on.

By deliberately ignoring this—Larry Summers knew the rent data was wrong but pretended it meant the opposite of what it did¹—and by focusing on dumb metrics like year-over-year inflation that are practically designed to mislead in situations like this, we've spent the past year panicking over a delusive view of what's going on.

And in case you think I forgot, there's a second phrase I highlighted from Dionne's column: namely that the modern Fed has a better understanding of "the underlying mechanisms of inflation." Am I permitted a small guffaw? As near as I can tell, literally nobody seems to understand the underlying mechanisms of inflation right now. Oh, there's lots of vague talk about supply chains and government spending and so forth, but nobody can supply a firm explanation of what really happened. So I will:

- Yes, the pandemic artificially reduced supply.

- Rents dropped at the start of the pandemic and eviction moratoriums were put in place. Rental markets overreacted to this, and in 2021 rents spiked enormously for six months before subsiding.

- Artificial fiscal stimulus kept consumers solvent and able to buy at normal levels. However, this was a minor part of core inflation (the best estimates range around two percentage points) and its influence ended quickly when the stimulus ran out.

- Savings also accumulated thanks to the stimulus. Inflation was always bound to decline as those savings were used up.

- Outside of core inflation, the Ukraine war caused energy prices to spike.

- Also outside of core inflation, food prices went up for entirely prosaic reasons: bad harvests, higher fertilizer prices, the Ukraine war, droughts overseas, and pandemic driven labor shortages. It was mostly just an unfortunate coincidence that this happened at the same time as everything else.

The bottom line is that practically everything about this inflationary episode was caused by an unprecedented pandemic that we reacted to quickly. And good for us! It's what we should have done even if we couldn't quite tune it perfectly and we ended up with perhaps a year of heightened inflation.

But it also means that it was all artificial. It wasn't due to underlying monetary policy or out-of-control spending or unions demanding higher wages. It has no analogs in the past and no lessons for the future—unless we encounter another huge pandemic. In that case it does provide a lesson: we mostly did everything right. We'll do a bit better in the future if we respond faster and more competently to the pandemic itself; adopt the same enormous fiscal response we did this time with possibly some tweaks; and maybe go easier on the eviction moratoriums, which aren't really necessary as long as we get the stimulus stuff right. That's probably about it, though I'm open to other suggestions.

MORAL OF THE STORY: We have been fooled all along because we surrendered to fears of the past and didn't look at the inflation data properly. Perhaps that was inevitable early on when data was thin, but today we have plenty of data and we know how to look at it. So now we need to do what John Maynard Keynes allegedly recommended, and change our minds when the facts change. Or, in this case, when the facts become clearer.

Our current bout of inflation was (a) completely artificial, (b) fairly short, and (c) will be completely gone within half a year. Unfortunately, monetary policy has lags, and we're still likely to pay a price next year for the higher interest rates of this year. We can only hope the damage isn't too great.

MY BIG CAVEAT: I don't know what's going to happen in China now that they've eased their COVID rules. In the worst case, they will have massive outbreaks and business shutdowns, which will either raise inflation by causing supply shortages or spur a massive recession that might reduce inflation. Or maybe neither. I have no idea.

¹Earlier this year Summers warned that the BLS rent figures were out of date, which meant official inflation figures for rent and housing were likely to go up this year because they were measuring year-old rents that had already gone up.

Think about this. He was explicitly telling us that inflation figures were going to rise because they were based partly on defective data. This should be a reason to tell us that we should calm down a bit because the official BLS figures were artificially and wrongly too high. Instead he simply said that because of the defect the official figures were going to rise and left it at that.

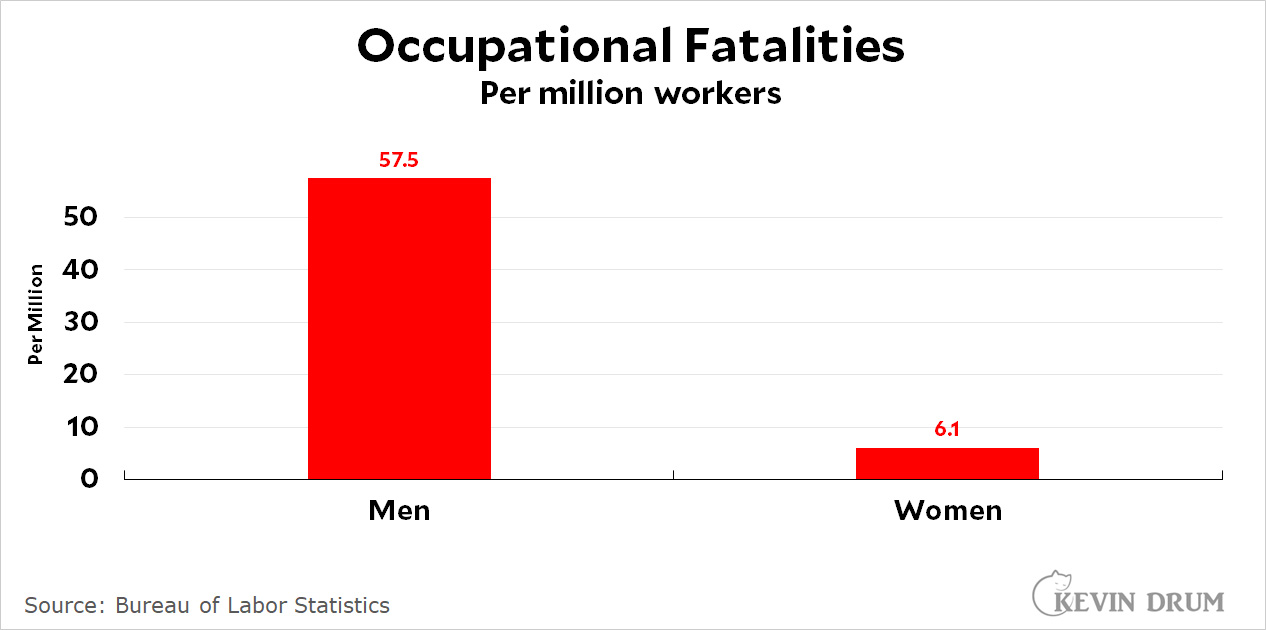

That's a 6% increase between 2020 and 2021, but 2020 was an outlier. Aside from that, occupational fatalities have been flat for the past five years.

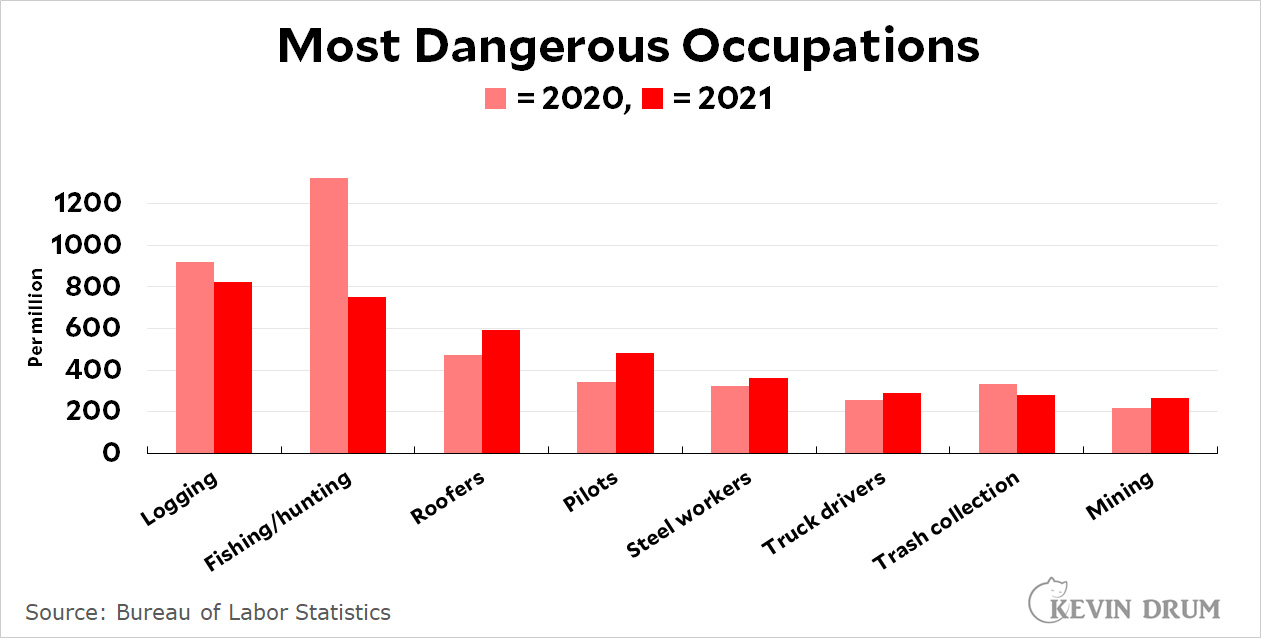

That's a 6% increase between 2020 and 2021, but 2020 was an outlier. Aside from that, occupational fatalities have been flat for the past five years. Here are the eight most dangerous occupations:

Here are the eight most dangerous occupations: Hunting and fishing lost its #1 spot to logging. Note that both of these occupations have fatality rates around 800 per million, which makes them 20+ times more dangerous than the average occupation. I was a little surprised to see trash collection on this chart. It's a more dangerous occupation than I realized.

Hunting and fishing lost its #1 spot to logging. Note that both of these occupations have fatality rates around 800 per million, which makes them 20+ times more dangerous than the average occupation. I was a little surprised to see trash collection on this chart. It's a more dangerous occupation than I realized. ¹This is because, for whatever reason, BLS doesn't report it that way. I'm too lazy to look up employment numbers for each category, and I'm not sure I could match the categories perfectly anyway. This is the best we can do.

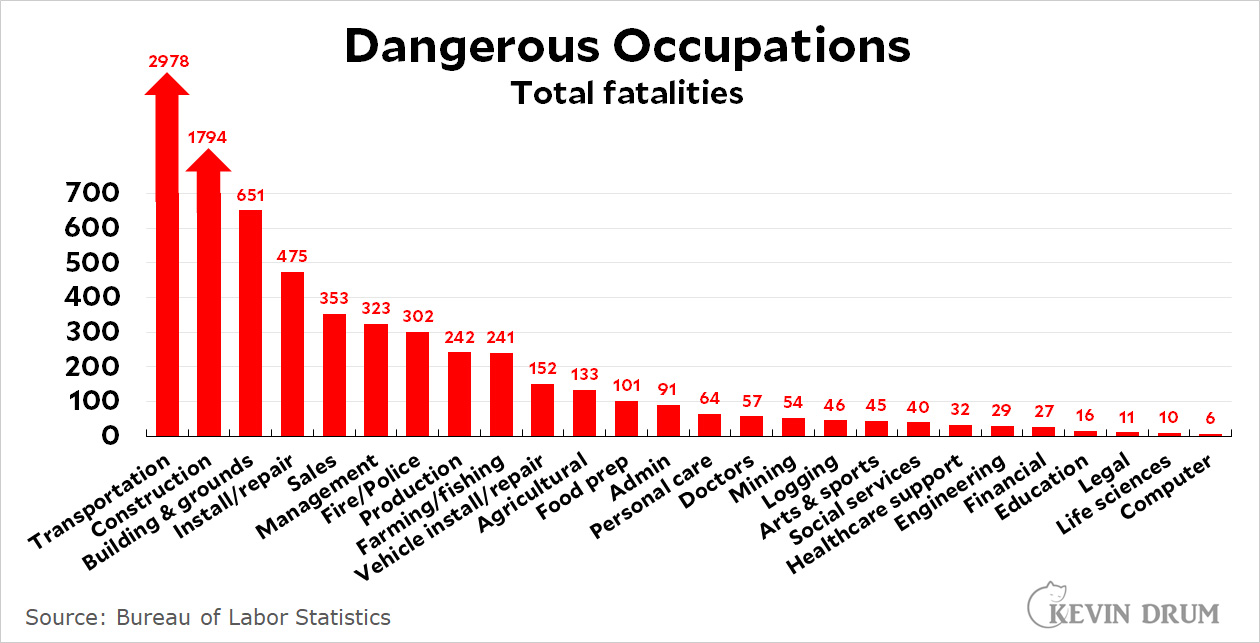

¹This is because, for whatever reason, BLS doesn't report it that way. I'm too lazy to look up employment numbers for each category, and I'm not sure I could match the categories perfectly anyway. This is the best we can do.