I overslept today, so I asked GPT-4 to write a limerick about oversleeping:

There once was a fellow who'd doze,

He set his alarm but he chose,

To hit snooze a few times,

And waste precious chimes,

Now his blog is a void and that blows.

I modified the final line, but the rest is all GPT. Here's a haiku:

Dreams lingered too long,

Sunrise passed, clock unaware,

Late for the day's start.

Meh. But I cranked out half a dozen versions in two minutes.

I've set this video from Microsoft to start at 7:54. Go ahead and watch about 30 seconds of it.

As a former high-tech marketing VP, I can confirm that marketing writing is generally pretty undistinguished. You don't have to be Shakespeare to put together a brochure or a PowerPoint presentation about a new product.

In other words, marketing is ideal for the kind of things GPT-4 is capable of. All that's necessary is that it somehow gets trained on facts and features about the new gizmo. And since this is marketing, even GPT-4's propensity for exaggeration is a feature, not a bug.

So what's the future of marketing communications when Microsoft Office can create data sheets, press releases, product slicks, websites, and so forth in about two minutes?

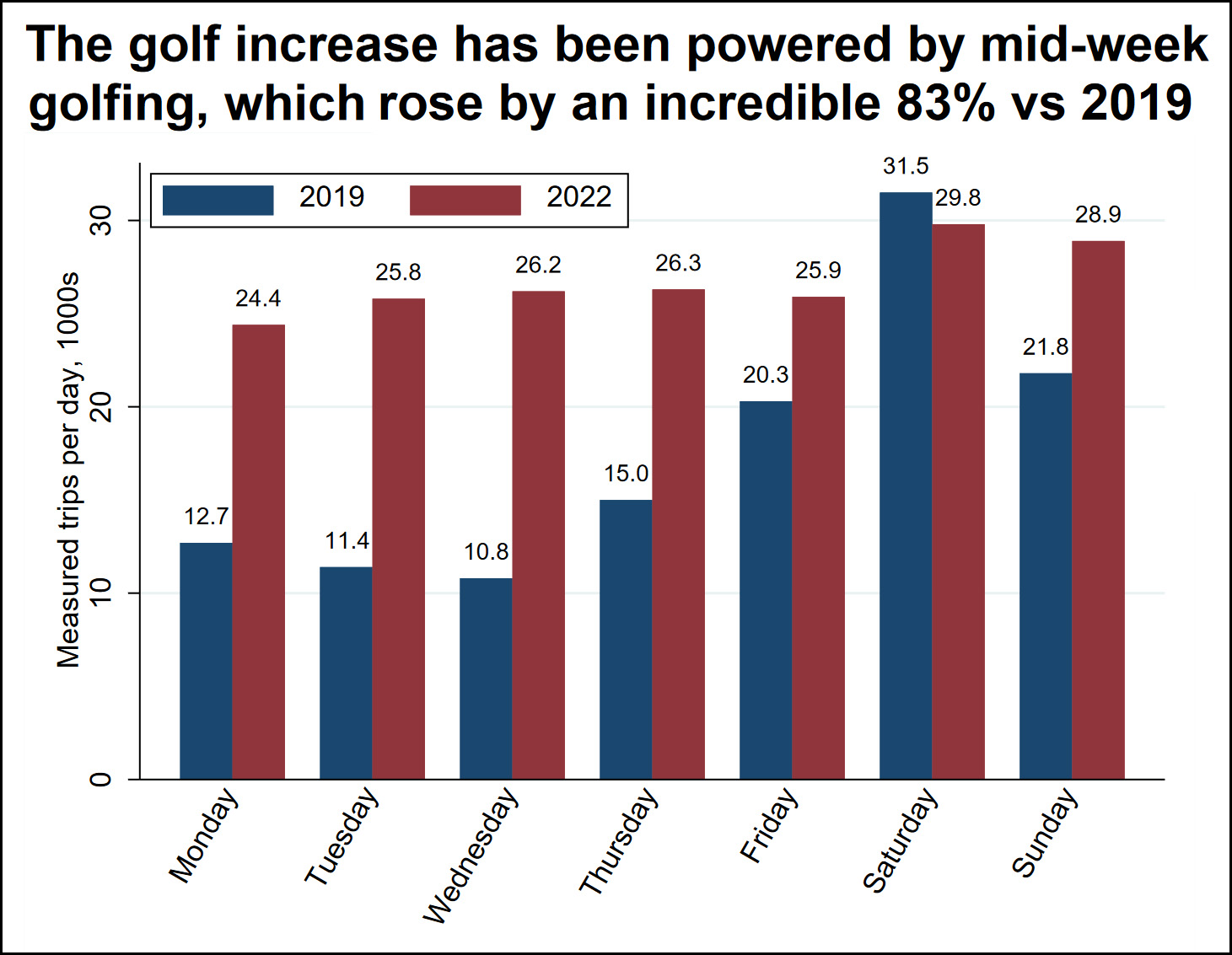

The New York Times reports that people who work at home are taking off lots of time in the afternoon. Golf has boomed:

A new study from Stanford shines a light on the rise of afternoon leisure. Using geolocation data near golf courses in the United States, the study found there was 278 percent more people playing golf at 4 p.m. on a Wednesday in August 2022 than in August 2019. And there were 83 percent more golf games being played on a weekday in August 2022 than in August 2019, according to the researchers, Nick Bloom and Alex Finan, who studied data, from the company Inrix, at more than 3,400 golf courses.

According to the Times, this trend means that workers "can now extend their leisure time into the afternoon, and tack on extra hours of work after dark."

Sure, you betcha. That's what they're doing.

But there's an interesting macroeconomic angle to all this. Golf is part of the service sector, and in normal times golf courses were fairly inefficient. There was lots of golf in the late afternoon and weekends, but the rest of the time things were slow. In other words, productivity was fairly low.

But now, with golf spread more evenly throughout the week, golf courses are more productive. Nick Bloom, one of the authors of the Stanford study, points out that when you multiply this by millions of service industry jobs the entire sector is more productive:

“This is an amazing potential reversal,” Mr. Bloom added. “You can have a huge increase in productivity using leisure resources throughout the week. It’s an odd unexpected boost from post-pandemic working from home.”

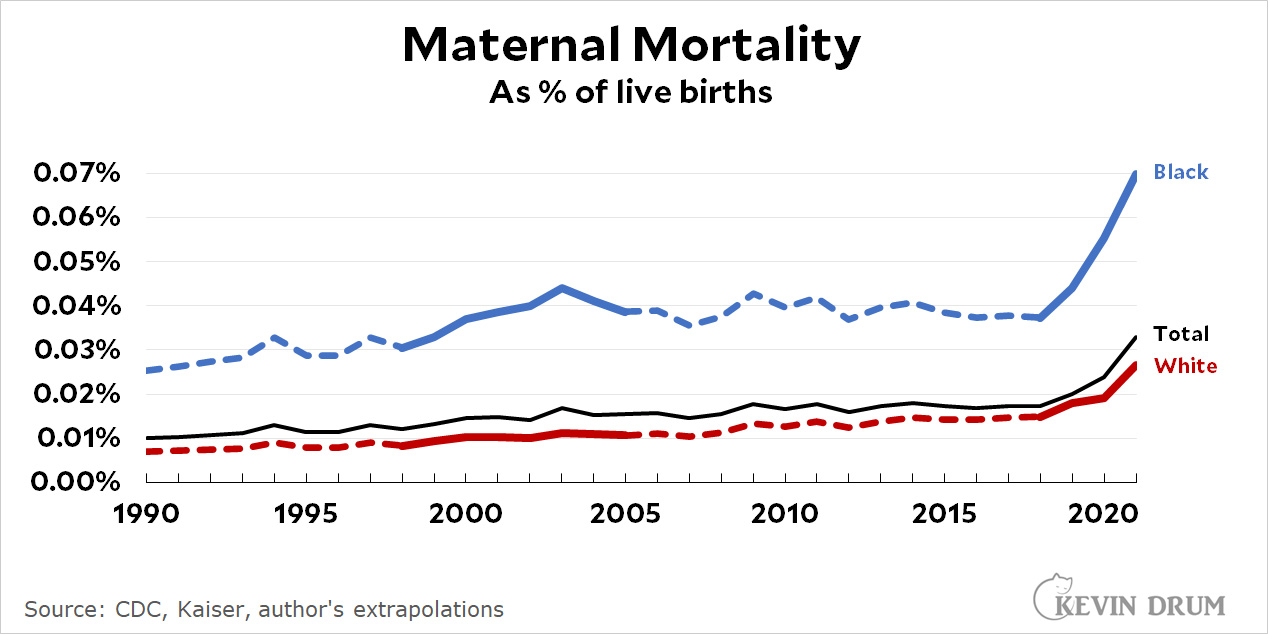

It's insane that maternal mortality has gone up 3x since 1990. It's insane that it increased 40% in 2021 according to the latest data from the CDC. 40%! It's insane that Black women have a maternal mortality rate 170% higher than white women.

Something seriously doesn't make sense about these numbers. Why would the overall number increase 3x during a period of improving health care? Why would the rate for Black women be stable for 15 years and then suddenly skyrocket starting in 2019? Why is the Black/white discrepancy so stubbornly high?

It's not because nobody cares about this. It's getting more study now, but researchers have been trying to puzzle it out for a long time. Nor is the racial gap due to racism—not entirely, anyway. Nor is this upward trend happening in other rich countries. Only in the US. And we've been pulling away from other countries only since 1999.

There are lots of theories about this, but none seem to match the data very well. And none of them come close to explaining the explosion of maternal mortality starting in 2019. Even the 2021 increase is mysterious. Sure, it's COVID, but there has to be more. Young women contracted COVID at high rates,¹ but not that high.

What the hell?

¹The mortality rate for young people was very low, but the case rate was upwards of 25-30%.

The federal judge who could upend access to a key abortion medication seemed open on Wednesday to the argument that the drug had not been properly vetted and could be unsafe — claims the Food and Drug Administration and leading health organizations strongly contest.

While the antiabortion group challenging the drug acknowledged there is no precedent for a court to order the suspension of a long-approved medication, U.S. District Judge Matthew Kacsmaryk questioned whether mifepristone has met the rigorous federal standard necessary to be prescribed to patients in the United States.

It's all such horseshit. Everyone knows mifepristone is safe. Everyone knows the FDA approval process in 2000 was fine. Everyone knows there's more than 20 years of real-world data to demonstrate mifepristone's safety. Everyone knows it's been approved for use throughout the entire world. Everyone knows why an obscure judge in a tiny jurisdiction in Texas is hearing this case. And everyone knows the case has nothing to do with safety anyway. It's just a way to make it harder to get an abortion.

But we're all forced to play make believe and pretend there's a real case here. And conservatives are all fine with this because, despite their incessant whining about "judicial wokeness" or whatever their latest complaint is, they don't care one whit about judicial process. They just want the result they want.

None of that matters, though. This Kacsmaryk dude is probably going to (a) ban mifepristone, (b) refuse to stay his ban while the case is appealed, and (c) get upheld by the 5th Circuit because they don't care about the law either. As for the Supreme Court, who knows anymore? Sam Alito promised us that courts couldn't interfere with abortion on a national basis, but he'll stroke his chin and solemnly pretend to believe this is really a question of whether the FDA overstepped its authority. And of course he'll agree that it did.

This business of fanatical Texas judges making policy for the whole country needs to stop. I don't know how to do that. But it's insane.

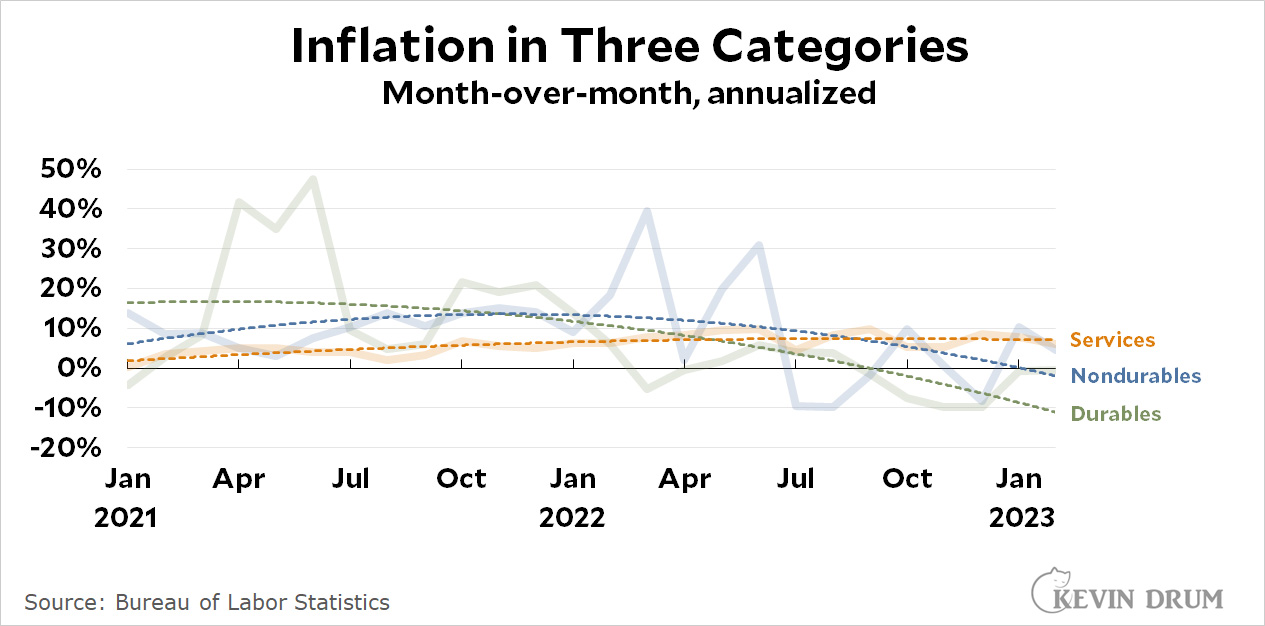

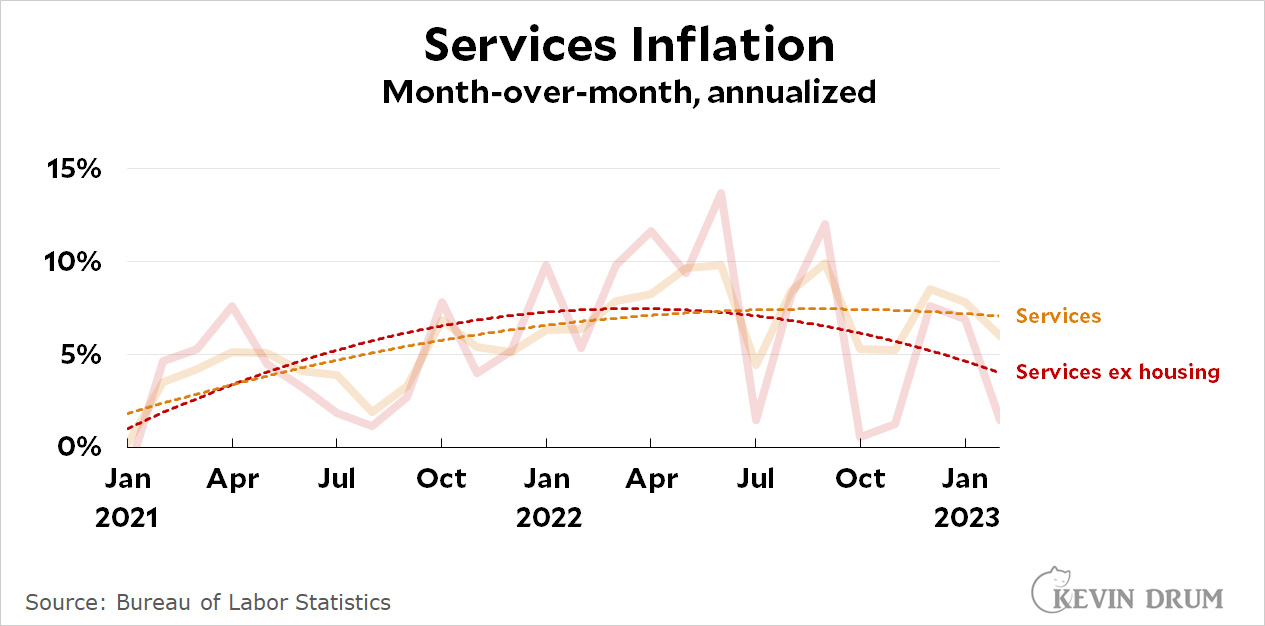

The latest hotness in inflation studies is to focus on inflation in the services sector. Why? Because that's what's highest right now, so it allows you to make a plausible argument that inflation is still a big problem and we need a nice, big recession to finally get it under control. For some reason this appeals to a lot of people.

So here is inflation broken up into its three most basic categories:

Sure enough, inflation in durable goods looks great. Nondurables had a weird spike in January but is on the right path. Inflation in services, by contrast, is both high and still rising. It clocked in at 6.0% in February.

In fairness, services make up about 70% of the economy, so they should be taken pretty seriously. Inflation in the service sector needs to start coming down if we want overall inflation to ever get back to 2%.

But wait! As we all know, the BLS is still recording big increases in shelter inflation because their numbers lag behind reality. So what does inflation in the service sector look like if we remove housing?

If you exclude housing, services inflation came in at 1.5% in February—though if you ignore the spike and just look at the trendline it came in at about 4%. When the BLS finally catches up and starts recording falling shelter inflation, services inflation will come down mechanically to 3% or so. Combine that with falling goods inflation and overall CPI will be in the ballpark of 2%.

Over the past few days, a million pundits have become instant experts on the finances of Silicon Valley Bank. They are outraged that no one before now noticed the bleeding obvious: SVB was a reckless and fragile bank, a literal time bomb on the edge of collapsing thanks to foolish business practices.

Now, 20/20 hindsight is great, but I've been digging into this for days and I just don't buy the narrative. I'm not saying SVB is faultless, but I am saying it was basically a sound bank facing some modest headwinds. Which they were addressing.

I have receipts for all this. They are mostly based on three documents:

Let's dive into the big issues surrounding the collapse of SVB.

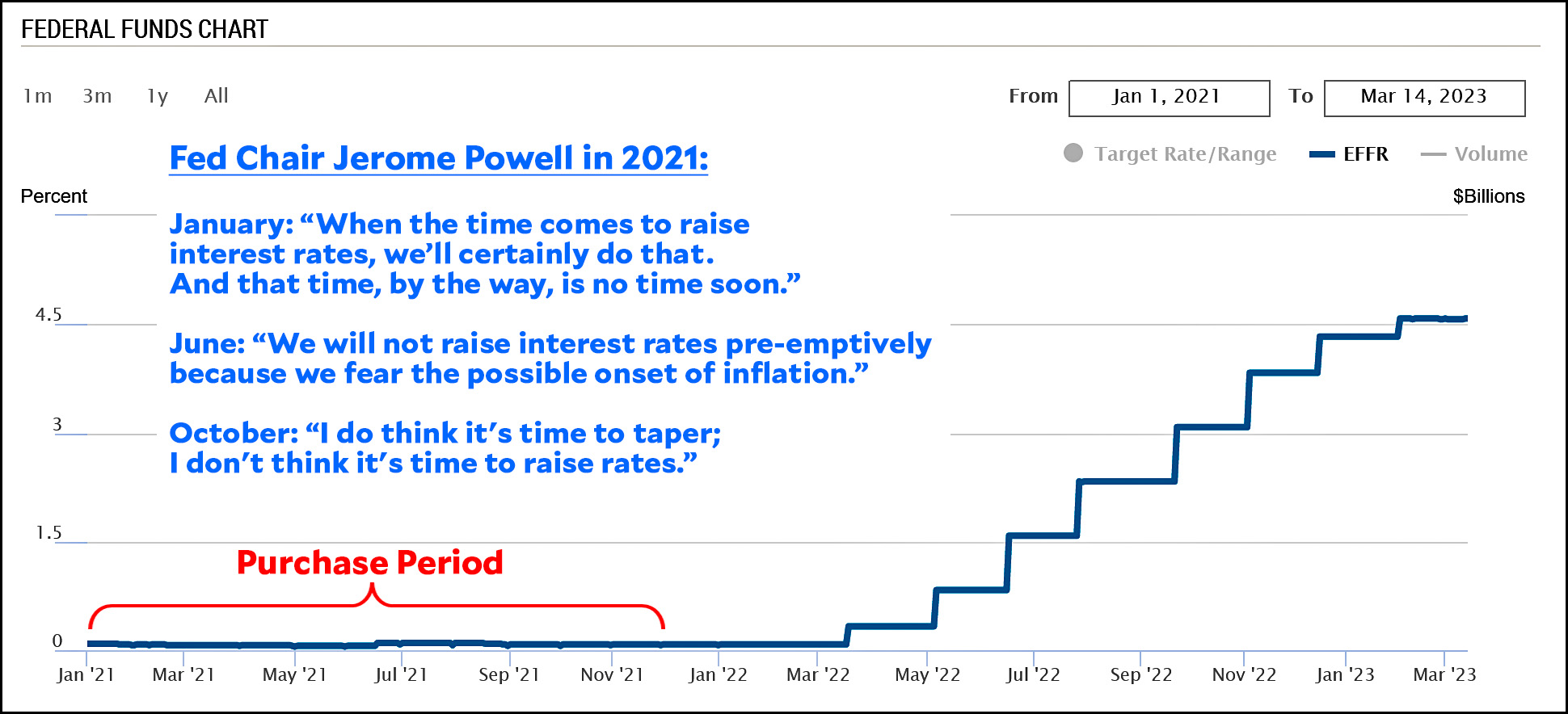

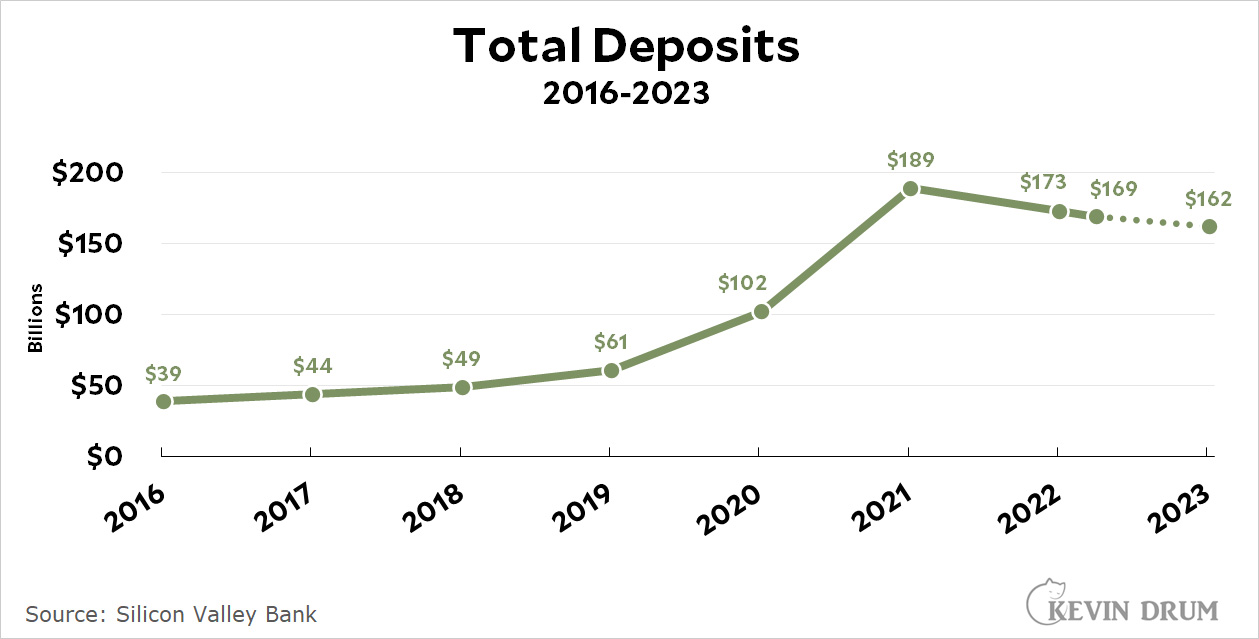

The bond portfolio. SVB had about $90 billion invested in long-dated treasury and mortgage bonds. This portfolio was vulnerable to interest rate risk, and SVB probably should have hedged that. However, keep in mind that nearly the entire portfolio was purchased in 2021:

At the time, there was little reason to think interest rate risk was high. There was certainly no reason to think that Jerome Powell would turn on a dime and not only raise rates, but raise them at an astronomical rate. And anyway, all of the bonds were marked as Hold to Maturity, which meant their losses never showed up on SVB's books and probably never would have.

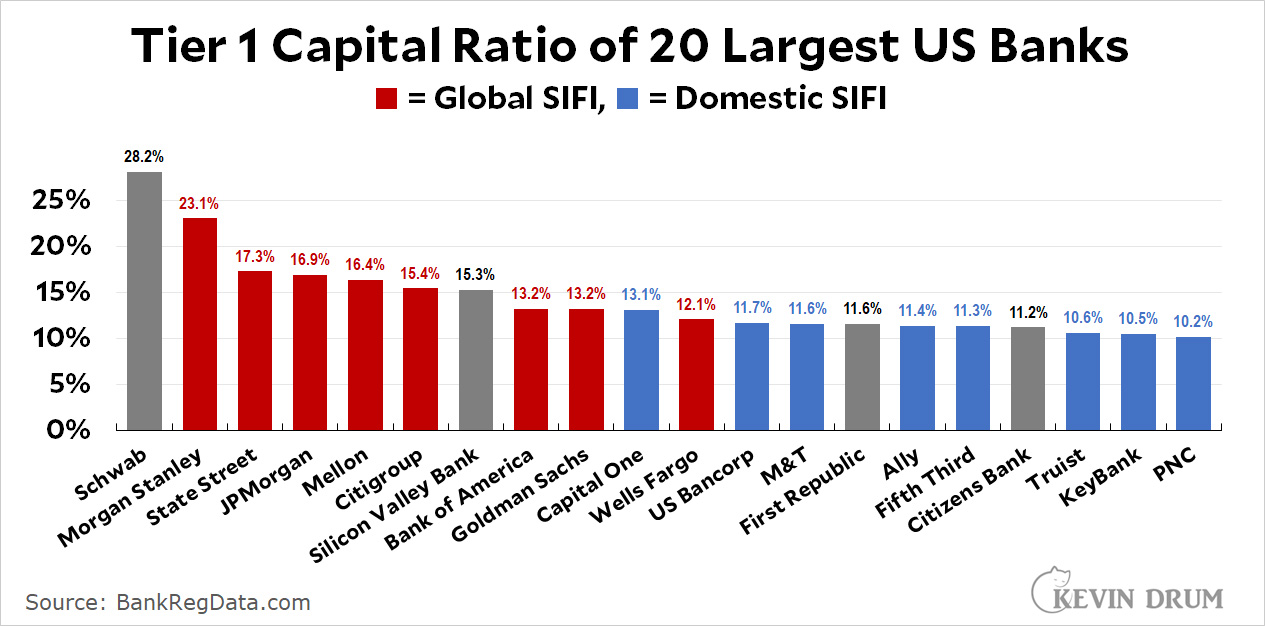

The 2018 deregulation. As best as I can tell, this had no effect at all on SVB. Most of the loosened regulations didn't apply to SVB, and the ones that did would have had no effect because SVB was already capitalized as strongly as a global SIFI and had plenty of liquidity. Their Tier 1 capital ratio was 15.3%; their CET1 capital ratio was 12.2%; and their leverage ratio was 8%. Those are way above anything required by regulators both before and after the 2018 law was passed.

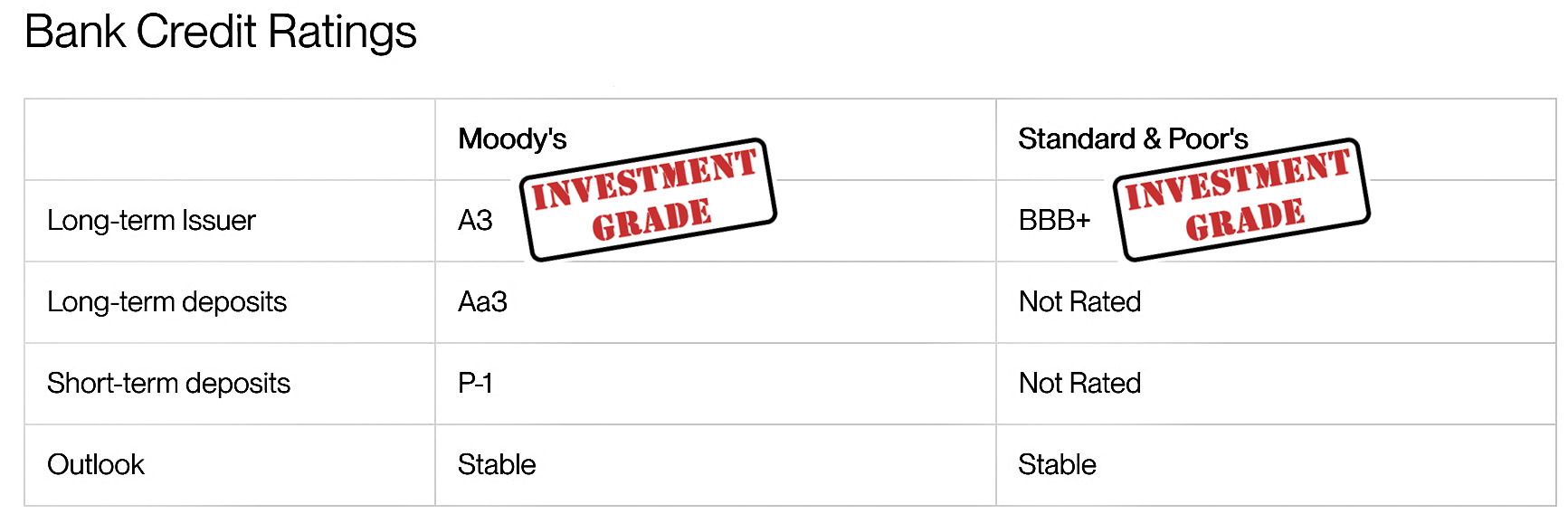

SVB's situation was absolutely not a secret. Maybe you and I didn't know about it because we didn't care, but it was well known to everyone who followed SVB. Their unrecorded losses produced a slight amount of nervousness, but that was all. Investors had no worries: after a big fall in 2022 when the tech boom slowed, SVB's stock was up nearly 40% since the start of the year. Analysts had no worries: they almost unanimously recommended SVB as a buy. Rating agencies had a bit of worry, but nonetheless rated SVB as investment grade.

SVB responded properly. In response to concern from Moody's about the worsening outlook for the tech sector, SVB consulted with Goldman Sachs and then announced that it would sell $20 billion of its assets at a $2 billion loss and then do a $2 billion capital raise to make up for the loss. This was perfectly prudent. It gave SVB plenty of cash to handle deposit outflows, while diluting its stockholders a bit in order to keep its capital buffers high. Moody's downgraded SVB in response, but this was actually a vote of confidence. They had intended to downgrade SVB two notches, but after the restructuring plan was announced they limited the downgrade to one notch.

On the morning of Thursday, March 9, SVB was solvent and perfectly capable of servicing its customers. It had some long-term challenges, but nothing life threatening. It was fine.

So what happened?

SVB really had only one problem: the pandemic had created a tech boom that saw the formation of hundreds of new startups. VC financing for all these startups flowed into SVB and spiked their deposit level from $61 billion to $189 billion.

In 2022, the tech boom went sour, and that meant no more startups and no more VC financing. As a result, existing startups had to pull money out of their SVB accounts to fund ongoing operations, and that led to a drop in deposits from $189 billion to $169 billion (as of March 8).

This was obviously concerning since SVB was heavily reliant on startup money. However, there was no reason to think that deposits would shrink anywhere near enough to actually jeopardize their solvency.

So what happened?

Nobody knows. Founders Fund, the venture capital fund co-founded by Peter Thiel, advised its companies on the morning of March 9 to withdraw their money from SVB. Why? We don't know for sure because neither FF's management nor Thiel are talking about what motivated them. Maybe they misread the Moody's downgrade. Maybe the capital raise spooked them. Maybe they heard some gossip that alarmed them. Or maybe it was nothing other than an excess of caution because they figured no harm would be done.

But Founders Fund is well known and influential, and news of what they had done spread around the Valley at light speed. Within a few hours, a $42 billion run had left SVB in ruins and the FDIC had taken over.

And now for a prediction: As more information unfolds and panic subsides, the FDIC will find out that SVB was not only solvent before the run, but even after it. Everyone will be paid in full and there will be money left over. The FDIC did the right thing regardless, since there's no stopping a run once it gets started, but there was never any good reason for it in the first place.

This is the altar of the Church of Sainte-Marie-Madeleine, a few minutes walk from our apartment in Paris last year. The building was begun as a church; interrupted by the French Revolution; redesignated as a monument to the Grande Armée by Napoleon; and eventually finished as a church. It was designed in the neoclassical style and looks like the Parthenon, but bigger.

Here's an odd thing. I asked GPT-4 to write a poem about the Ides of March and it produced one with rhyming couplets. I asked it to try again without rhymes, but it just produced a poem with different rhymes. So I asked it a third time, and then a fourth:

I apologize for the error. Here's another version without rhymes:

Beware the ides of March, a fateful time,

When fate and history may intertwine,

A day of warning, when omens may appear,

And change the course of all that we hold dear.

In ancient Rome, a leader met his end,

A cycle of power, betrayal, and descend,

A lesson taught through ages, to understand,

That change and growth are at life's very command.

For though the ides of March may bring us fear,

They also hold the power to make things clear,

A time of reflection, a chance to restart,

And shape the future with a stronger heart.

So let us honor those who've gone before,

And learn from them the lessons to explore,

For in this cycle of life, death, and rebirth,

We find the beauty of our time on earth.

I tried a few more times, and the same thing happened every time. Does GPT-4 not understand the concept of rhyme?

POSTSCRIPT: On the other hand, it produced 16 lines of rhyming iambic pentameter in a few seconds. My quickie take is that this poem is roughly at the level of, say, a college sophomore. Not bad, I guess.

Another interesting thing is that the first poem it wrote was very literally tied to Julius Caesar and his assassination. The second one was a little more abstract and third even more so. The fourth one, above, has one line that alludes to Caesar and that's it. I'm not sure what to make of this, but it seems to have a fairly specific trajectory when you ask it to repeat something over and over.