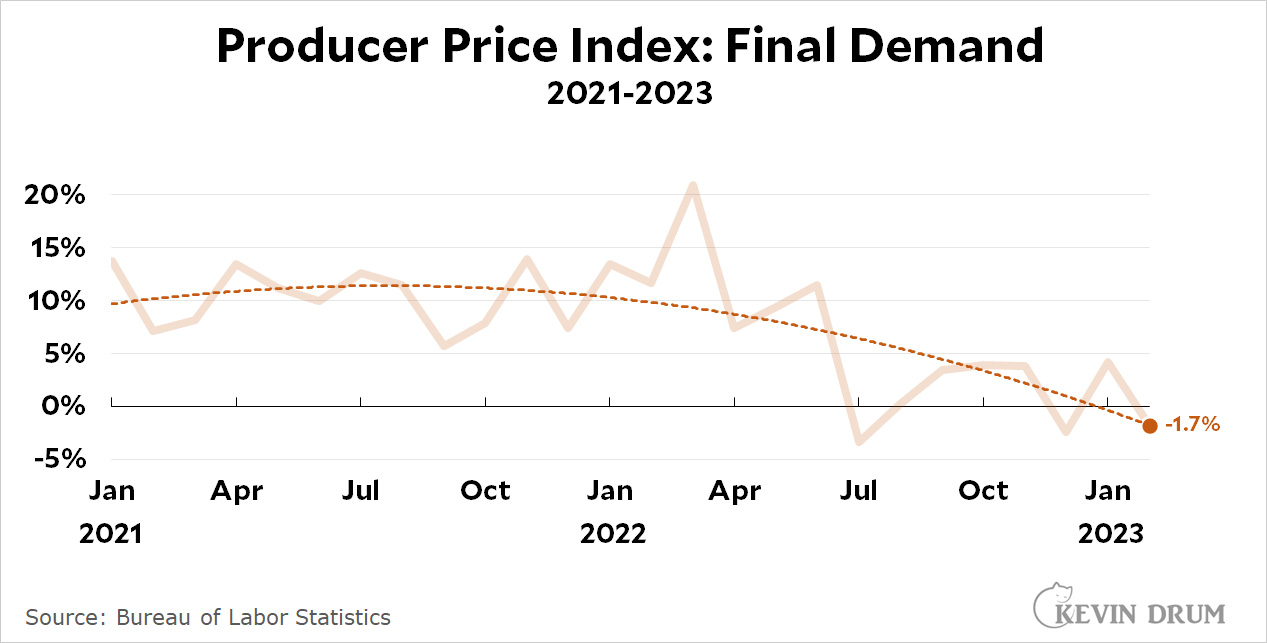

We have good news and bad news today. The good news is that producer-level inflation was negative in February:

This doesn't tell us anything about inflation in services, so it's limited good news. Still, good is good.

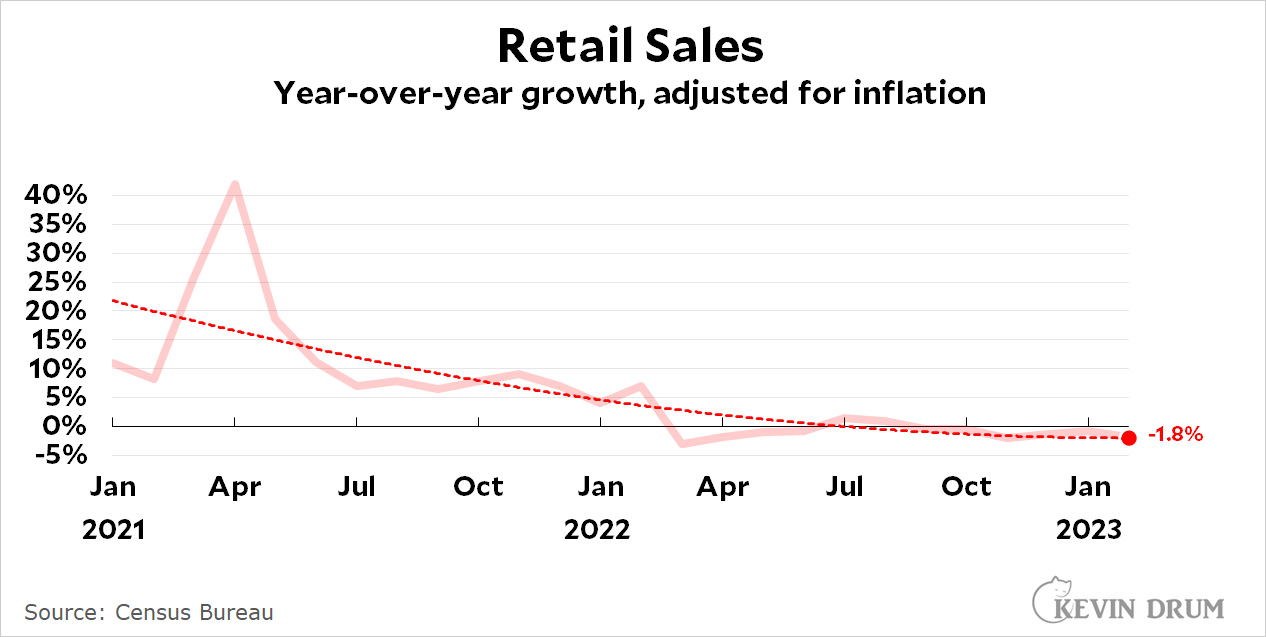

The bad news is that retail sales fell for the sixth straight month:

Of course, this is good news insofar as it suggests the economy is slowing and the Fed doesn't need to raise interest rates to slow it even more. Take your pick.

It's time for some serious geekery. This post will (once again) address the question of whether the 2018 bank deregulation law had any effect on the collapse of Silicon Valley Bank.

Yesterday I looked at SVB's capital ratios and concluded that they were higher than required either with or without the law. If deregulation had never passed and SVB had been more tightly regulated, they still would have passed every test easily.

But David Dayen suggests I look specifically at the Liquidity Coverage Ratio (LCR). What if SVB had been required to meet the LCR requirement for medium-sized banks?

The idea behind LCR is simple: During a period of stress, does a bank have enough liquid assets to cover 30 days of cash outflows? The equation for medium-sized banks is:

My horseback guess puts HQLA at about $40 billion and net cash outflow at $30 billion or so. Luckily, though, we don't have to take my word for it. Bill Nelson of the Bank Policy Institute takes a deeper dive and comes up with this estimate:

HQLA = $52.8 billion

Cash outflow = $50.3 billion

Thus, LCR was about 105%, well above the 70% requirement. Hell, it was above the 100% requirement imposed on large banks. So even if the strict old law had been in existence, SVB still would have passed with flying colors.

POSTSCRIPT 1: The primary motivation for regulating LCR is to ensure that banks have a leverage ratio above 3% (minimum Basel III requirement), 5% (Fed requirement for normal banks), or 6% (Fed requirement for big banks). SVB had a leverage ratio of about 8%, well above all of these requirements.

POSTSCRIPT 2: I should note that the Bank Policy Institute has a dog in this fight since it supported the 2018 deregulation. Nonetheless, its estimate of LCR looks reasonable to me. Needless to say, I'm wide open to other estimates if anyone has done them.

It's hummingbird season again, and I have several who buzz around my window these days. The top picture is (I think) a mature Allen's hummingbird, while the bottom picture is a young 'un.

I realize that I posted a picture of a hummingbird just about a month ago, but what can I say? I like hummingbirds.

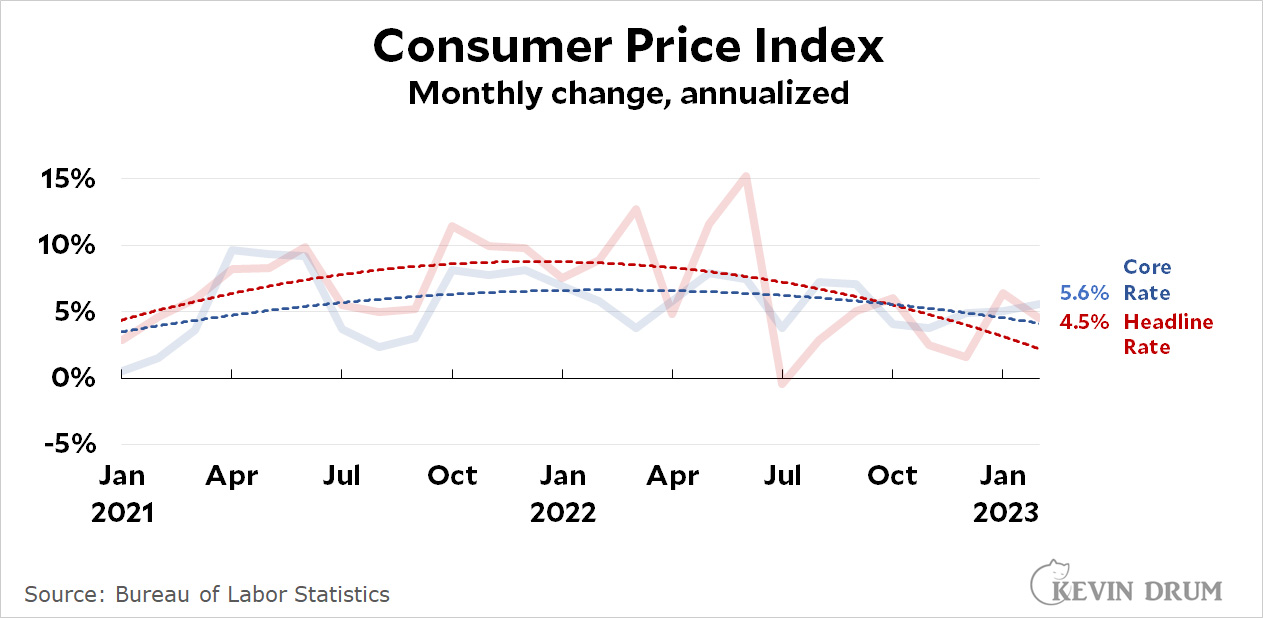

Headline CPI dropped from January's high reading, but core CPI moved up a bit. This makes three months in a row that core CPI has been creeping upward.

(In case you care—which you shouldn't—the year-over year rate that news outlets highlight was 6.0% for CPI and 5.5% for core CPI.)

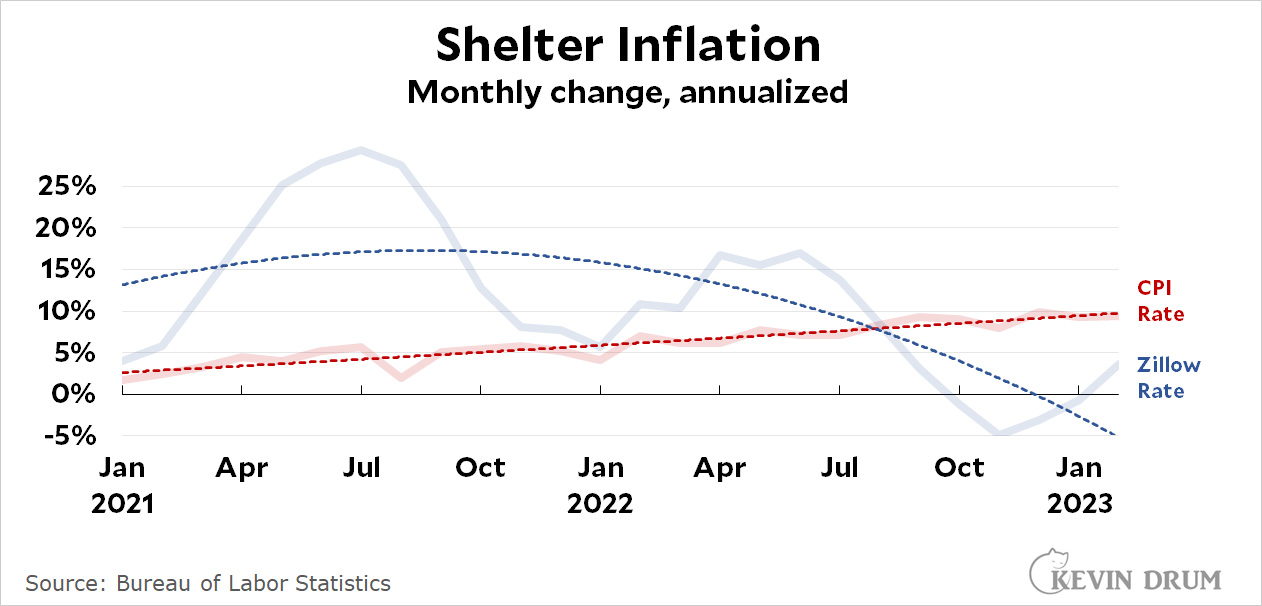

But inflation is actually not as bad as it looks. According to the BLS, shelter accounted for more than 70% of the increase in the headline rate. This is kind of crazy. We all know that shelter CPI lags the actual market, but is it ever going to catch up?

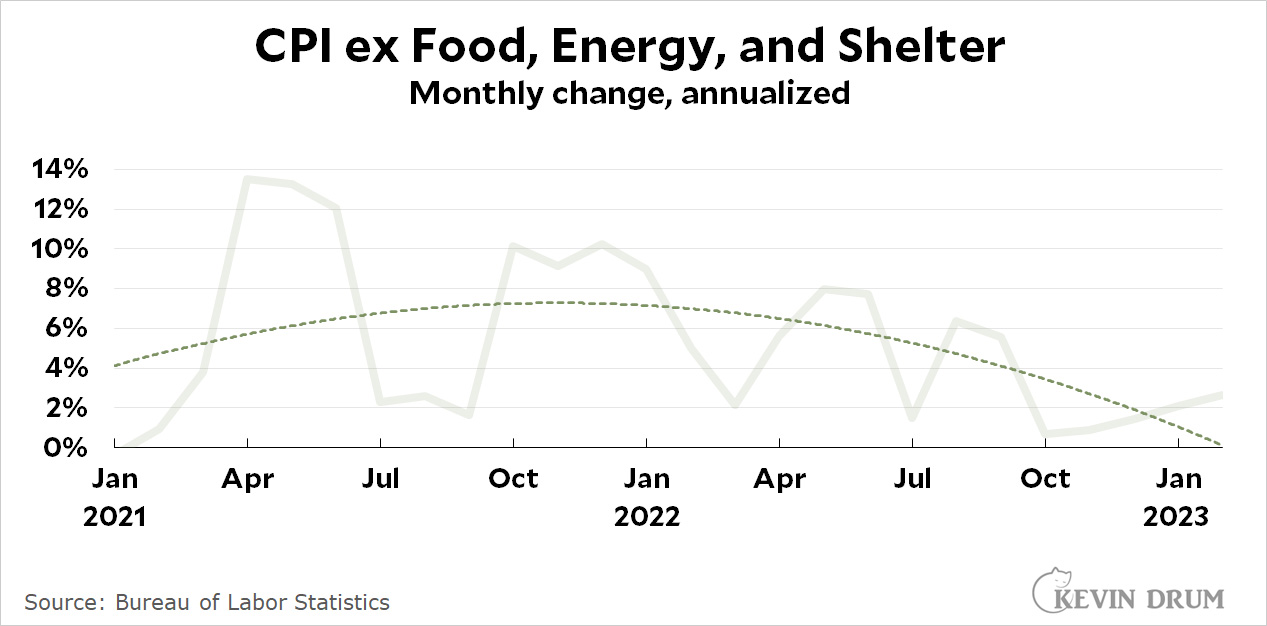

Shelter inflation measured by CPI is still rising steadily and clocked in at 9.5% in February. Zillow, by contrast, shows rents falling since last June. Their figure for February is 3.7%. Here's what core CPI looks like if you remove shelter:

That's . . . not bad. It's disconcerting that it's increased for four consecutive months, but it's still at only 2.7%.

Policywise, none of this may matter. Given the wobbliness in the banking sector right now, the Fed is unlikely to want to raise interest rates much, if at all. The latest CPI numbers could be better, but they're good enough to allow a pause.

I keep asking that question and getting no answers. There’s a lot of activity going on in what is called artificial intelligence, but it is more accurately called machine learning. The chatbots now amazing the credulous simply predict, on the basis of a training set, which word will follow the previous one.

....But there has to be a reason that Big Tech is putting money into the enterprise, and presumably they believe they will make money out of it. They gloss this with Benefits To The User. Better search! Automated letter writing! They leave out things like automated facial recognition to help arrest people and yet another way to separate the customer from the seller.

This is a tricky question. I happen to think that things like ChatGPT already have some usefulness, including—yes—better search and help with letter writing, among other things. But I also agree that the current version of ChatGPT isn't anywhere close to artificial intelligence.

Ric and Zooey. Or is it Zooey and Ric?

But! Even though I think true AI is still ten or fifteen years in the future, the software we build along the way will become increasingly useful even if it isn't truly our cognitive equal. I've suggested, for example, that in a couple of years ChatGPT might very well be good enough to replace lots of lawyers. Probably some doctors, too. Maybe even teachers, though that's more speculative.

Those are just tidbits, though. The real usefulness of current machine learning software is that it's a (necessary) step along the way to AGI—artificial general intelligence. AGI will be able to do pretty much anything humans can do, and shortly after that it will be able to do more than humans can do.

Now, if you don't believe that we'll ever be able to produce AGI, or that it's hundreds of years away, then there's nothing to talk about. We'll just have to wait a decade or two and see what happens.

But if you agree with me that we'll have it fairly soon, then Cheryl's question becomes: What do I think is the usefulness of a machine version of human intelligence? And there, I assume the answer is fairly obvious:

Since I'm positing that AGI-powered robots will be the cognitive equal of humans, then by definition they'll be able to perform every conceivable human job.

But better than humans! In addition to our raw smarts, they'll work 24 hours a day, have instant access to all human knowledge, and never ask for a raise.

As teachers, they'll be personalized to every student. It won't matter if you have a visual learning style. It won't matter if you're on the spectrum. It won't matter if you're dyslexic or ADHD. They'll adapt to whatever works best.

As caregivers they'll be completely reliable, infinitely patient, and willing to talk endlessly about anything that we olds want to natter on about.

If we haven't done so already, superhuman AGI will solve both our energy problems and global warming.

I'll confess that I've never understood why anyone would ask what AGI is good for. It just seems so obviously world-changing. But maybe I'm missing something.

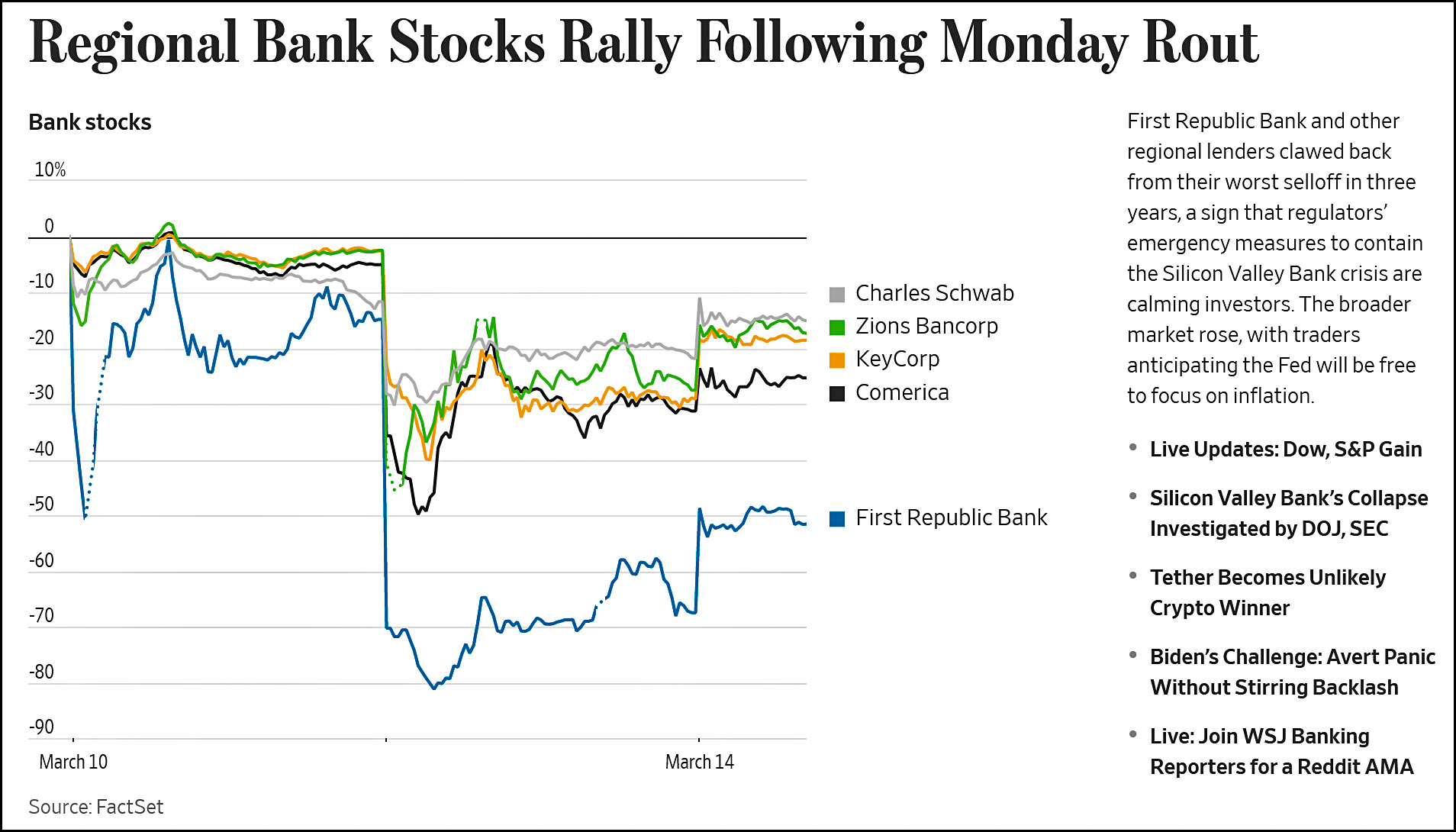

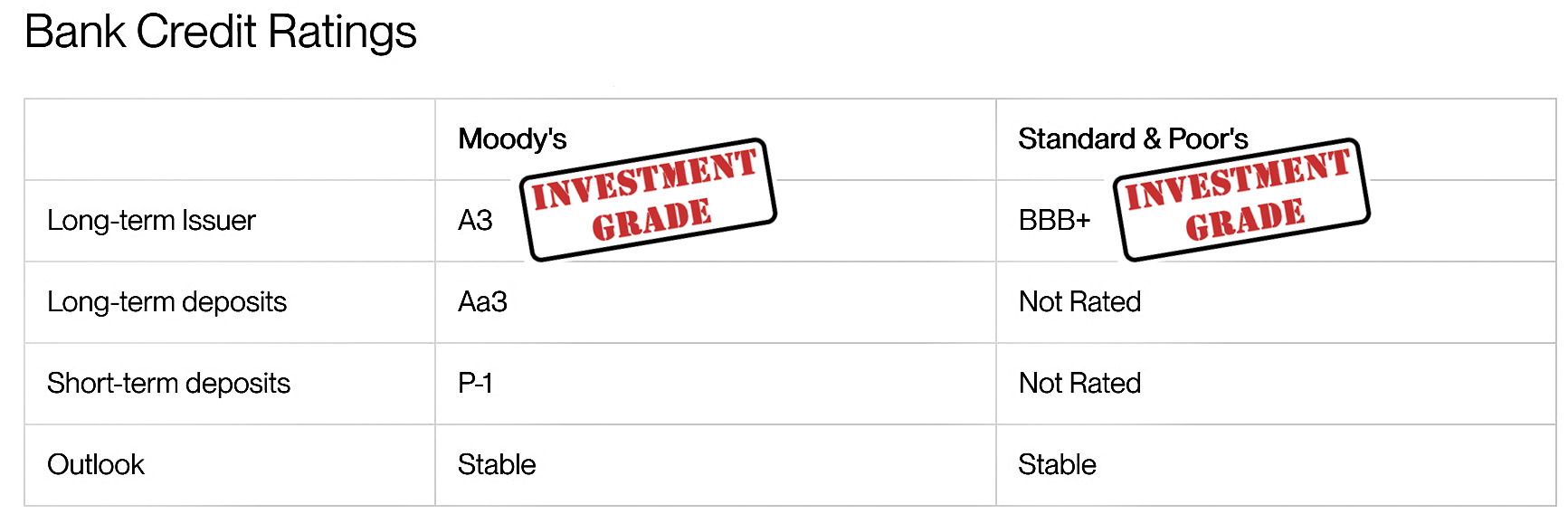

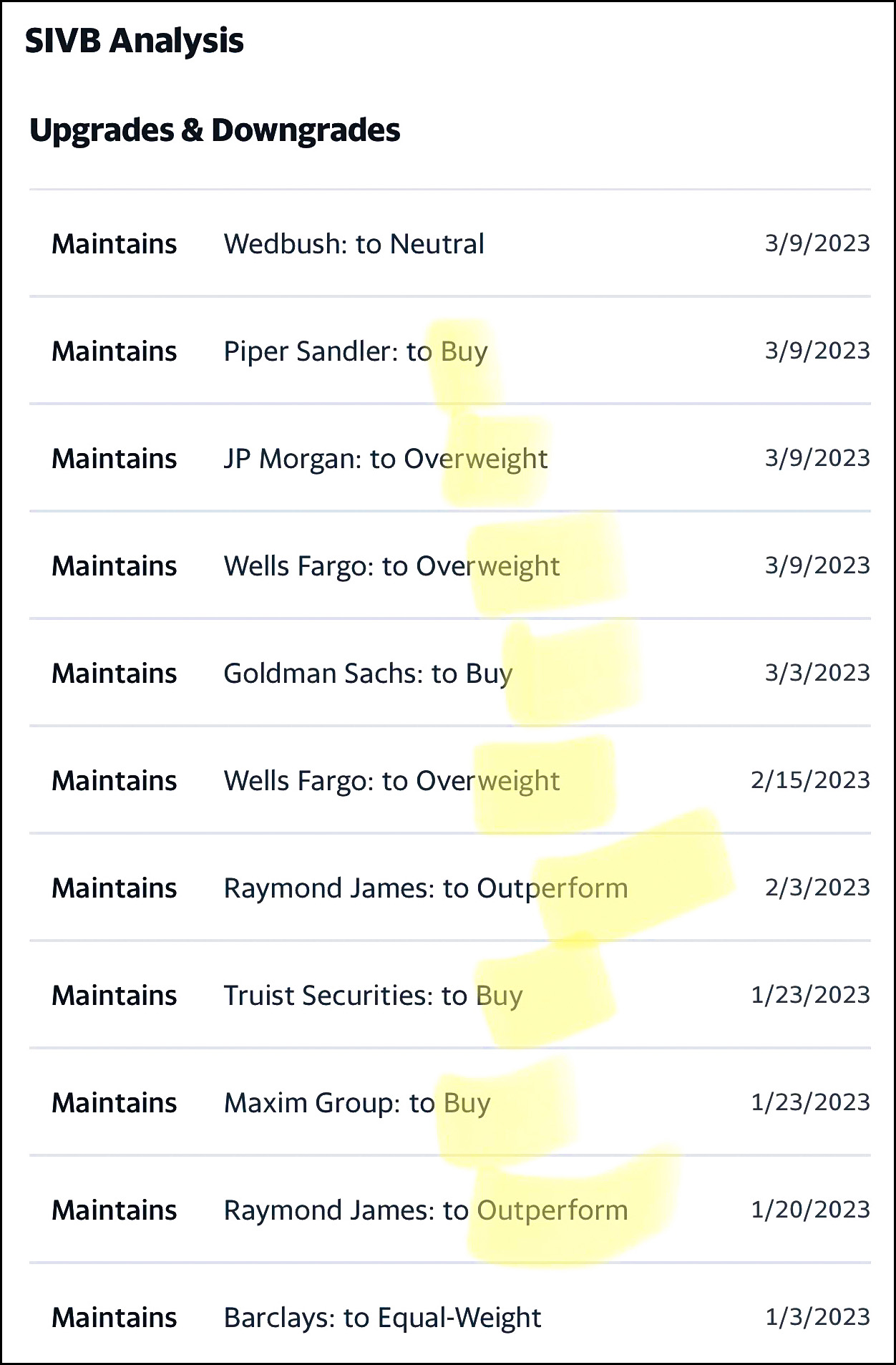

Was Silicon Valley Bank in good shape before it was put out of business by a bank run? As of Tuesday, March 7, here's what the rating agencies said about them:

Buy! Overweight! Outperform! The analysts who followed SVB and were intimately familiar with its balance sheet remained enthusiastic until literally the very last minute.

I'd also show you what the regulators said, but there's nothing to show. Like the rating agencies and the analysts, they saw no problems.

Even on Wednesday, March 8, after SVB had issued its mid-quarter review, nothing happened. Moody's downgraded them slightly to Baa1, which is still solidly investment grade, and that was about it. None of the pros who understood SVB best had anything bad to say about them.

By close of business the next day there was nothing left but ashes.

Earlier today I asked if the 2018 bank deregulation bill had any effect on the collapse of Silicon Valley Bank. The consensus in comments was that deregulation allowed SVB to avoid Fed stress tests that might have uncovered its liquidity problems.

(As a brief aside, it's common to say that SVB bet on interest rates staying low and then took big losses when the Fed hiked interest rates. That's true as far as it goes, but SVB's bond portfolio was marked as Hold to Maturity, which means the losses never showed up on their books. In other words, the problem wasn't interest rates per se because SVB never intended to sell those bonds in the near term. The problem was that the bonds in this portfolio were illiquid because they couldn't be sold without recording a big loss all at once. This isn't an interest rate problem so much as a classic, time-honored liquidity problem.)

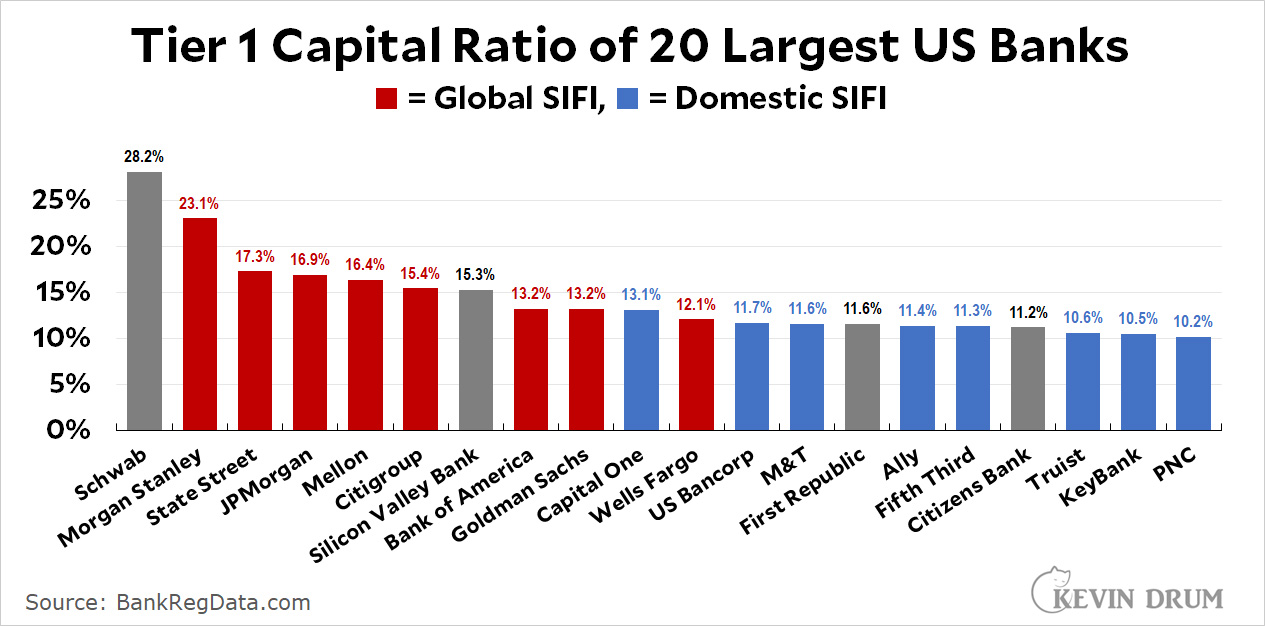

The question is whether this would have been flagged in a Fed stress test. For reference, here are the 20 biggest US banks sorted by Tier 1 capital ratio:

There are a couple of things to take away from this. First, SVB should have been designated a SIFI—a Systemically Important Financial Institution. It wasn't big enough to qualify as a global SIFI, but it was certainly big enough to qualify as a domestic SIFI.

That said, its capital adequacy was excellent, higher than practically every domestic SIFI in the country—and higher than even the new capital ratios imposed on the three biggest US banks last year. Given that, would a liquidity stress test have demanded an even higher capital ratio? I have my doubts, and in any case SVB would have been given time to beef up its reserves.

None of this is meant to imply that SVB's management didn't make mistakes. Their unrecorded losses in long-dated bonds, along with the outflow of deposits caused by the tech crash, had been a widely recognized problem for at least a year. On the flip side, they really did have plenty of high-quality capital and plenty of cash available from selling other assets. They clearly recognized that the outflow of deposits was likely to last longer than they had thought, and they addressed this by (a) selling assets, (b) trying to sell shares, and (c) looking for a buyer. I don't have the banking chops to know if this was sufficiently prudent behavior, but certainly SVB would have been OK in the near term if it hadn't suffered a huge, almost instantaneous run coordinated over social media. The lesson, I guess, is that if you live by tech, you run the risk of dying by tech.

I'm already tired of Silicon Valley Bank, but I have a question: If the 2018 deregulation bill hadn't passed, how precisely would this have affected SVB? And I do mean precisely. Would they have been required to diversify their deposit base? Would they have been required to hold more capital? Would they have been forbidden from loading up on long-dated Treasurys? Would they have been subjected to stress tests that included huge spikes in interest rates?

What exactly would have been different under the old rules?

This doesn't tell us anything about inflation in services, so it's limited good news. Still, good is good.

This doesn't tell us anything about inflation in services, so it's limited good news. Still, good is good. Of course, this is good news insofar as it suggests the economy is slowing and the Fed doesn't need to raise interest rates to slow it even more. Take your pick.

Of course, this is good news insofar as it suggests the economy is slowing and the Fed doesn't need to raise interest rates to slow it even more. Take your pick.