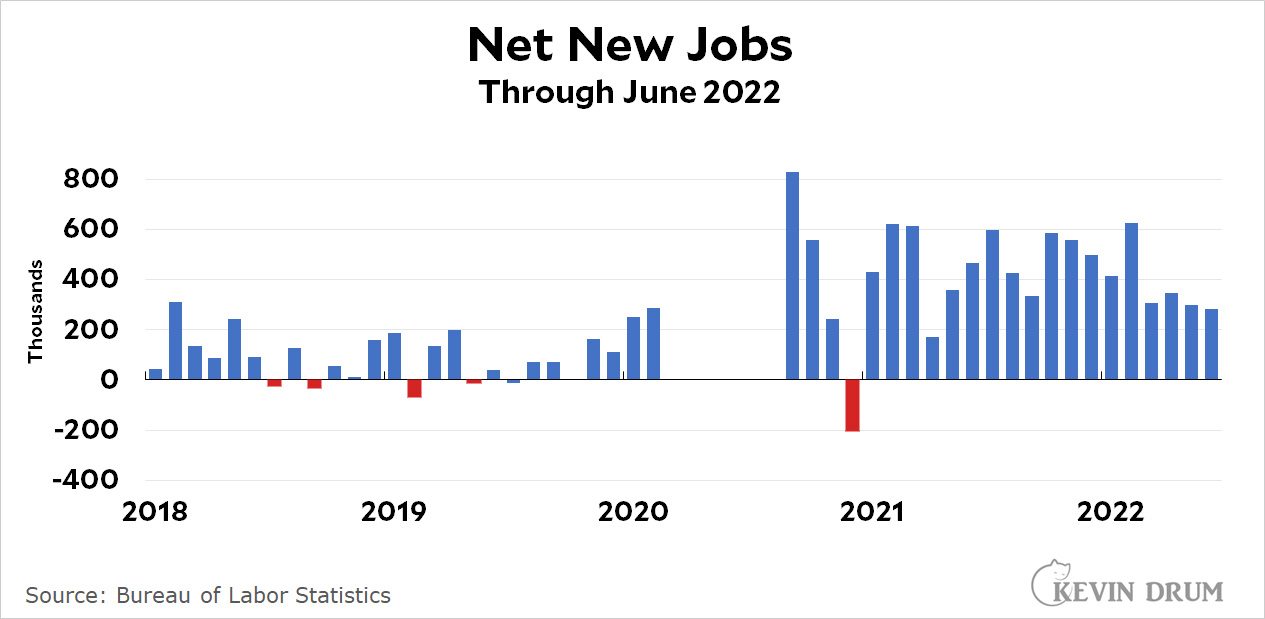

The American economy gained 372,000 jobs last month. We need 90,000 new jobs just to keep up with population growth, which means that net job growth clocked in at 282,000 jobs. The headline unemployment rate remained flat at 3.6%.

This month's report is something of a statistical mirage. The size of the civilian labor force declined by 353,000 and the number of employed people declined by 315,000. Not so good! However, the number of unemployed workers declined by 38,000 while the number of underemployed workers (those who had to settle for part-time jobs) declined by 707,000. Not so bad! Meanwhile, more than half a million people dropped out of the labor force, which is . . . something. I'm not sure.

This somehow gets mathified into 372,000 new jobs, but I'm not feeling super happy about it. Both the Labor Force Participation Rate and the Employment-Population Ratio were weaker than last month.

Earnings of blue-collar workers were up at an annualized rate of 5.9% over May, which comes to -5.7% adjusted for inflation. That's a volatile number and probably doesn't mean much. However, the yearly number is more reliable, and for the past year wages were up only 5.4%, which comes to -3.2% adjusted for inflation.

(Note that the New York Times says wages "continued to climb rapidly" last month, which is only true—both for June and for the past year—if you don't account for inflation. Why don't they?)

So . . . the number of employed people was down and blue-collar wages were down. On the bright side, a lot of part-time workers apparently got more work thanks to strong business conditions. I'm not quite sure what to make of all this, but for now I'd call it a fairly so-so jobs report.

If new jobs are higher than expected, it's an indication that the economy is running too hot. This is producing a demand-driven inflationary spiral that needs to be stomped on.

If new jobs are lower than expected, it's an indication that workers are holding out for higher wages. We are in danger of another '70s-style wage-price inflationary spiral that needs to be stomped on.

If new jobs come in exactly as expected, it's an indication of stagflation. The flation part of that needs to be immediately stomped on.

FYI: The consensus for the June report is 250,000 new jobs.

Buckle up, I've got an exciting post for you today!

As you know, Gross Domestic Product is the size of the economy. It's calculated by adding up the value of all the goods and services produced in the United States.

But you can calculate the same number by adding up all the income needed to produce this stuff. That's called Gross Domestic Income, or GDI.

Here's a table that shows the main components of GDP and GDI:

GDP

GDI

Personal consumption expenditures

Wages

Fixed residential investment

Taxes

Fixed nonresidential investment

Subsidies

Inventory change

Interest

Exports

Net business transfer payments

Imports

Proprietors' income

Government expenditure and investment

Rental income

Corporate profits

Government surplus

Consumption of fixed capital

Total for Q1 of 2022

$24.4 trillion

$25.2 trillion

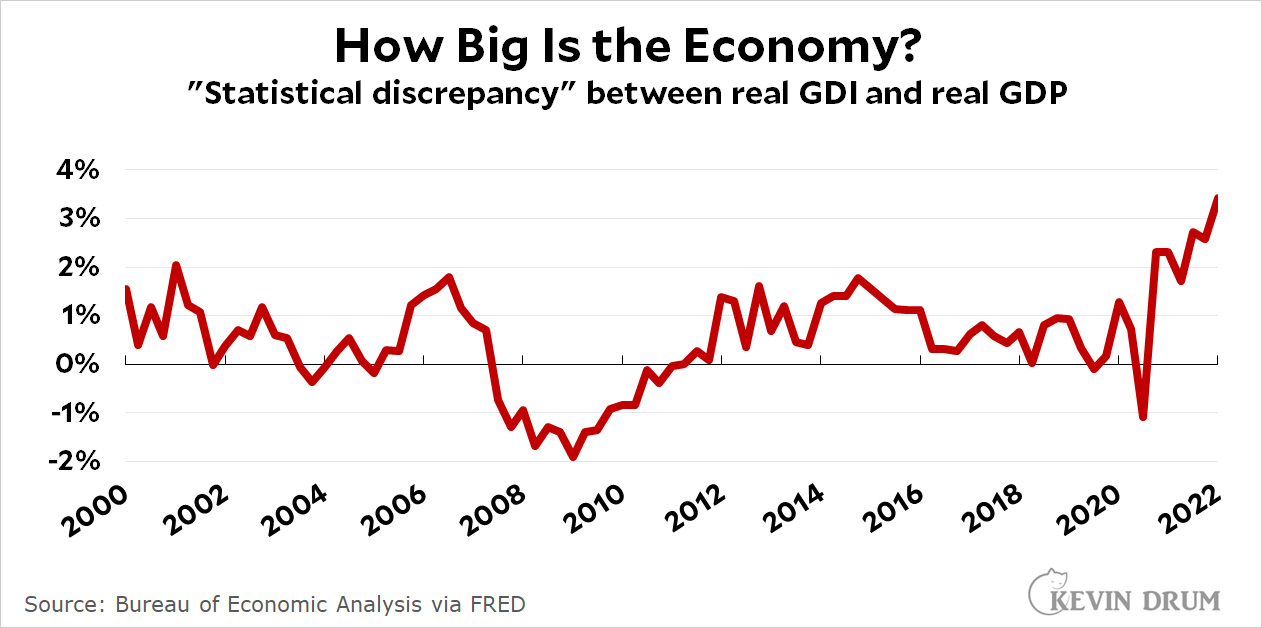

Hmmm. If these are supposed to be the same thing, why is GDP only $24.4 trillion compared to GDI at $25.2 trillion? As you'd guess, it's impossible to measure all the components of GDP and GDI precisely, so there's always a statistical discrepancy. Here's what that looks like over the past few years:

The statistical discrepancy is usually on the order of 1-2%, but for the past year it's been rising well above its norm. In Q1 of 2022, it hit 3.4%. In other words, GDI was 3.4% bigger than GDP.

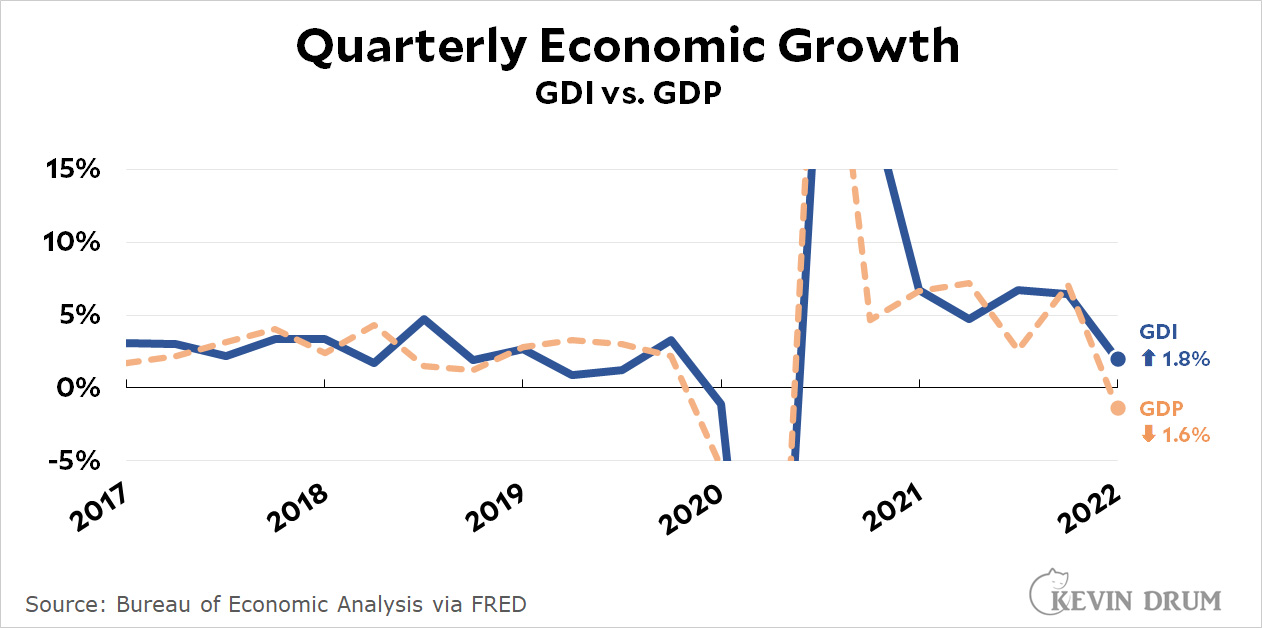

So which one is right? GDP is normally considered the more reliable measure because its components are easier to measure. Still, a discrepancy of 3.4% is a lot, and it affects what we think of economic growth. Take a look:

According to GDP, the economy shrank last quarter at an annual rate of 1.6%. According to GDI, it grew at an annual rate of 1.8%.

So why did I go through all this? Just to give you the background to a recent set of remarks from James Bullard, president of the St. Louis Fed. He believes that GDI is more consistent with other economic indicators at the moment, which means the economy isn't slowing down all by itself. It's growing at a normal rate.

And that, in turn, means that we can't count on a slowing economy to rein in inflation. We need to take more aggressive action, like the big rate increase the Fed announced a few weeks ago.

Is he right? That's above my pay grade, and only future revisions of GDI and GDP will tell us which one was actually more accurate. I'm just passing it along to help us all understand some of the thinking that goes on in the Eccles Building these days.

Every week I try to post at least one picture in the categories Animal, Vegetable, and Mineral. I've always wondered if anyone noticed that.

I've already done animals and minerals this week, so that leaves vegetables, which are typically either flowers or gardens. So here's a picture of the Coulée Verte in Paris, an old elevated train line that's been converted into a public park. It's three miles long and was completed in 1993.

Unlike the similar Highline in New York City, the Coulée Verte is indeed verte, full of plants and flowers and ponds and shady benches to enjoy it all. On the day we visited, Marian and I grabbed a couple of sandwiches and some fruit and ate lunch, then walked to the other end and caught a metro home. It's worth a visit.

But still, stuff happens. Except in this case it happened again. In 2018 Trump fired Comey's assistant, Andrew McCabe, 26 hours before he qualified for his full pension. Two years later, McCabe was also chosen for a rectal probe audit.

What a coincidence! Needless to say, everyone denies everything. But if you believe that, I have a swamp and a bridge and some cryptocurrency you might be interested in. It sure sounds like the good old days of Richard Nixon made a comeback in the Trump era, doesn't it?

POSTSCRIPT: Even if the IRS finds nothing, these kinds of audits are expensive and time consuming. The New York Times reports that Comey had to spend $5,000 on accountants' fees to eventually learn that he had overpaid his taxes by $347. McCabe ended up paying a "small amount" of money.

In comments last night, skeptonomist accused me of rarely being interested in showing income inequality. This cut me to the core, but there's truth to it and it's worth showing you why.

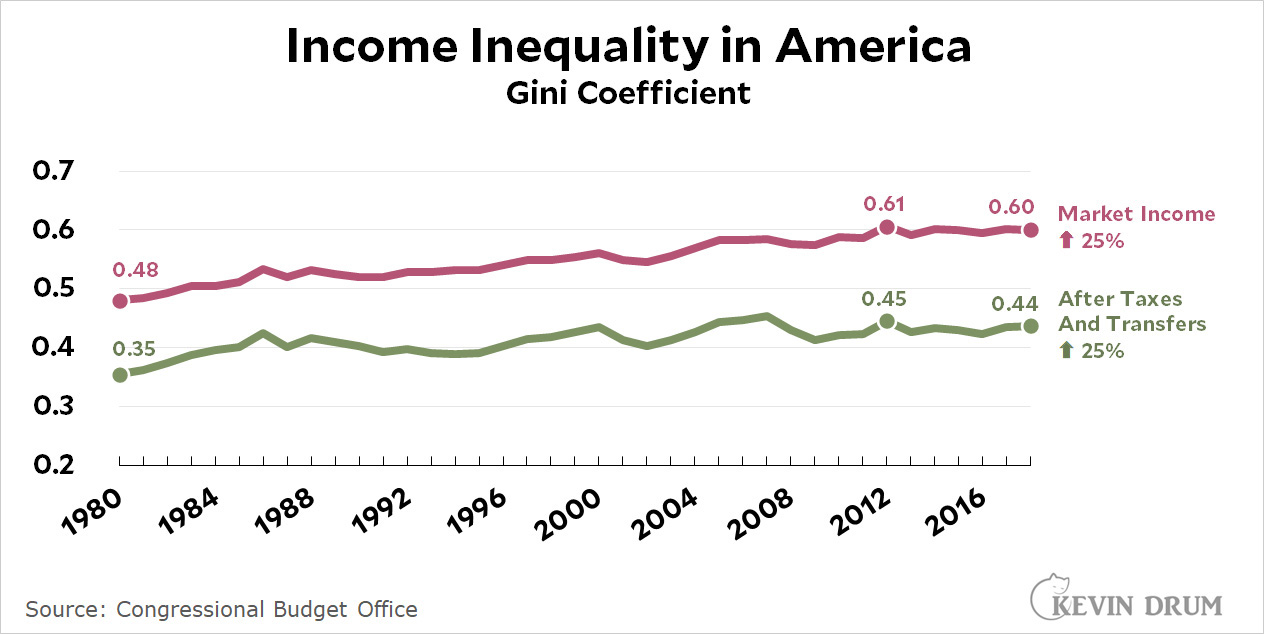

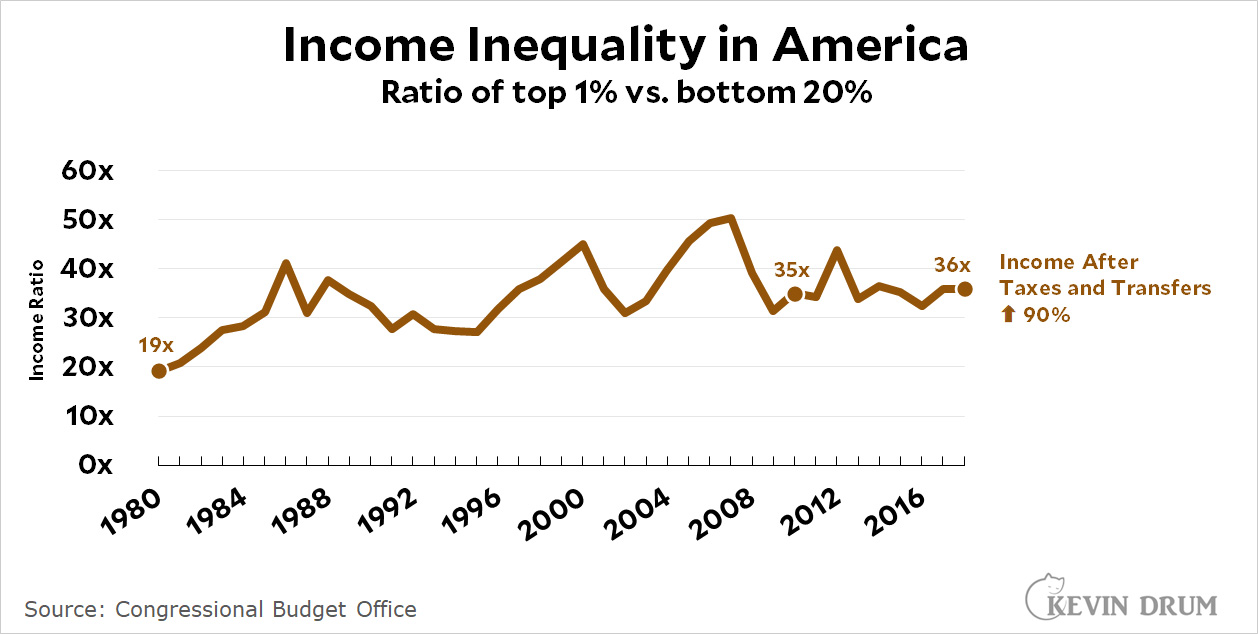

The single best set of numbers for income inequality come from the CBO. There are two reasons: (a) they collect a broad set of income figures, including capital gains and means-tested benefits, and (b) they include figures for the top 1%, which is where inequality has risen the most. So without further ado, here are two charts based on CBO income figures:

The top chart shows the GINI coefficient, which is the most common measure of income inequality. It's much lower (i.e., better) when you include taxes and transfers, which is just what you'd expect, but it's been rising steadily since the Reagan era either way.

GINI is a little abstract for most people, so the bottom chart is a simple comparison of income between the top 1% and the bottom 20%. It shows much the same thing as the GINI chart but with even stronger growth.

But now take a closer look at these charts. They show income inequality growing strongly starting with Reagan and then peaking during the housing boom of the aughts. Then income inequality declines during the Great Recession and hasn't changed much since. In 2010, at the end of the recession, the average top one-percenter had an income 35x higher than the average bottom quintiler. By 2018 that had gone up only to 36x. Likewise, since 2012 GINI hasn't budged.

I'm not here to tell you that growing income inequality is no longer a problem, but it's certainly calmed down over the past decade or so. This is probably why you don't hear as much about it as you did during the Occupy Wall Street days at Zuccotti Park.

This is a surprisingly tricky question, but with a twist at the end. When you talk about earnings you have to account for at least three different things:

Mean or median? Mean (aka "average" or "per capita") income is usually not a great measure because the ultra-wealthy skew it. If you have ten people making $50,000 and one person making $1 million, the mean income is a very misleading $136,000. Median is better: it records the halfway point of income and isn't heavily skewed by high incomes.

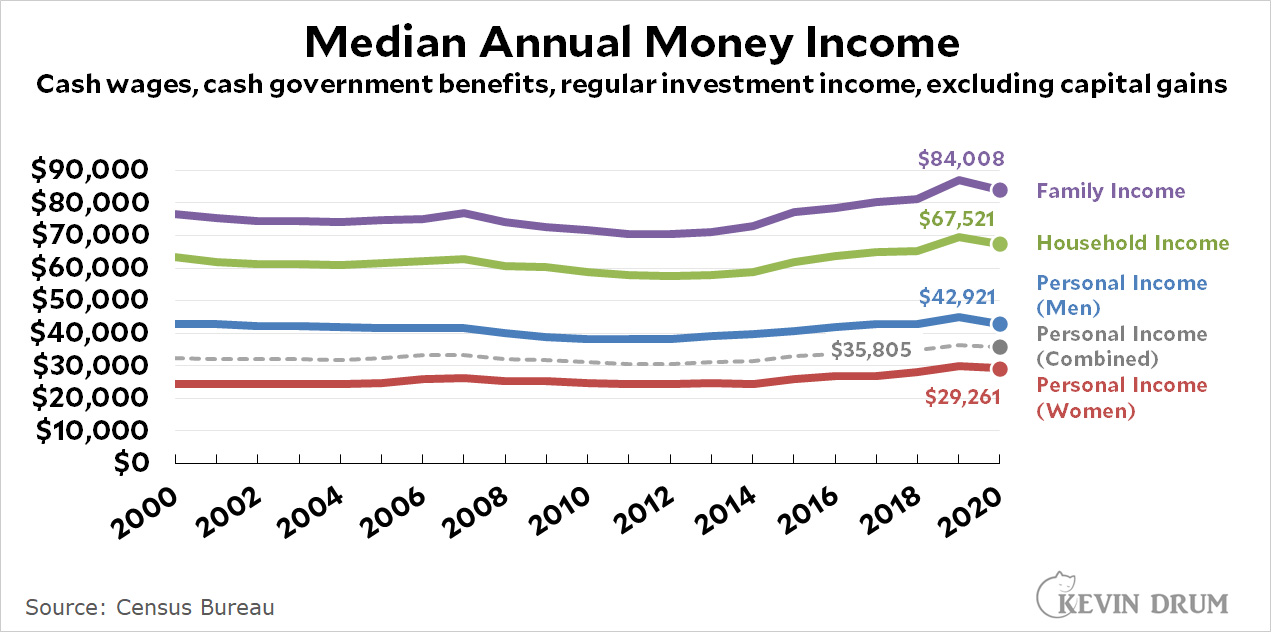

Personal, family, or household? Personal is a single individual. A family is a group related by birth and marriage. A household includes everyone who lives in a particular housing unit.

What income? There are lots of kinds of income. Cash income vs. benefits (like employer health care). Wages vs. investment income. Taxes (negative income) vs. government transfer payments. And capital gains are usually an entirely separate category.

Needless to say, there's also the distinction between nominal income and real income. Real income is adjusted for inflation and it's almost always what you should use. All of the charts in this post show real income.

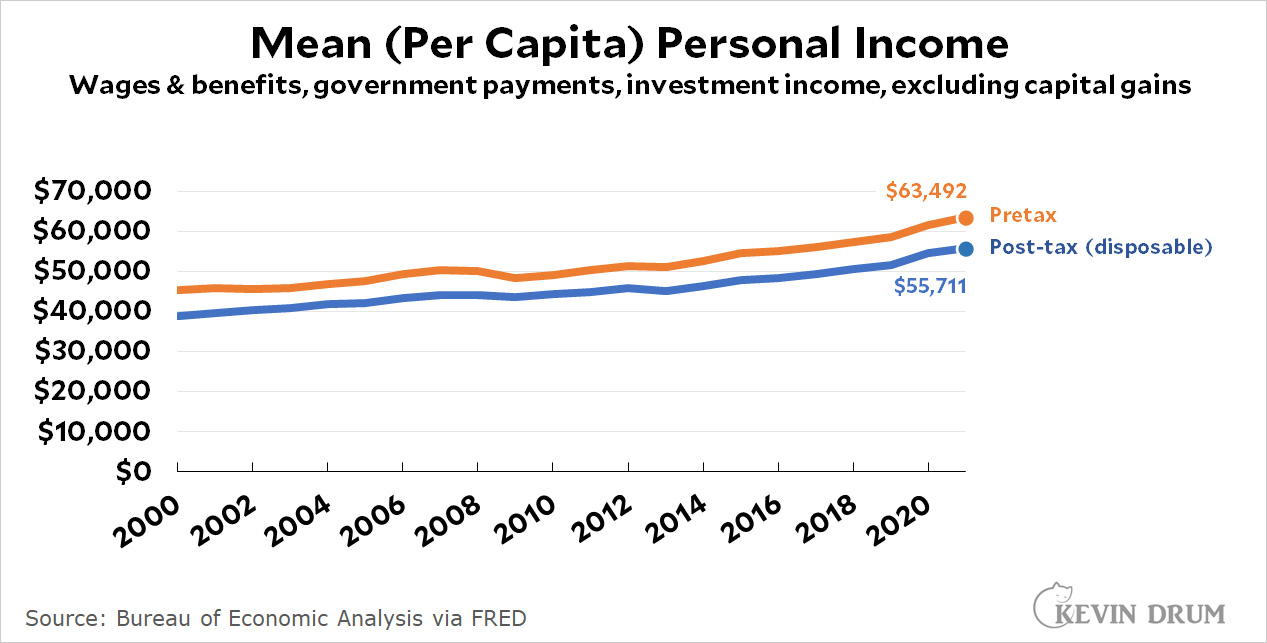

These figures are basically fine and are widely cited. They're really all you need for most purposes and they contain a wealth of breakdowns (gender, race, education, etc.). But if you want more, here's the personal income series from the Bureau of Economic Analysis:

BEA income includes more items than the Census Bureau, and the BEA also provides a figure for disposable (after tax) income. But its big difference with the Census Bureau is that BEA uses mean instead of median income, which makes it much less valuable. The huge difference between the two is almost entirely due to this.

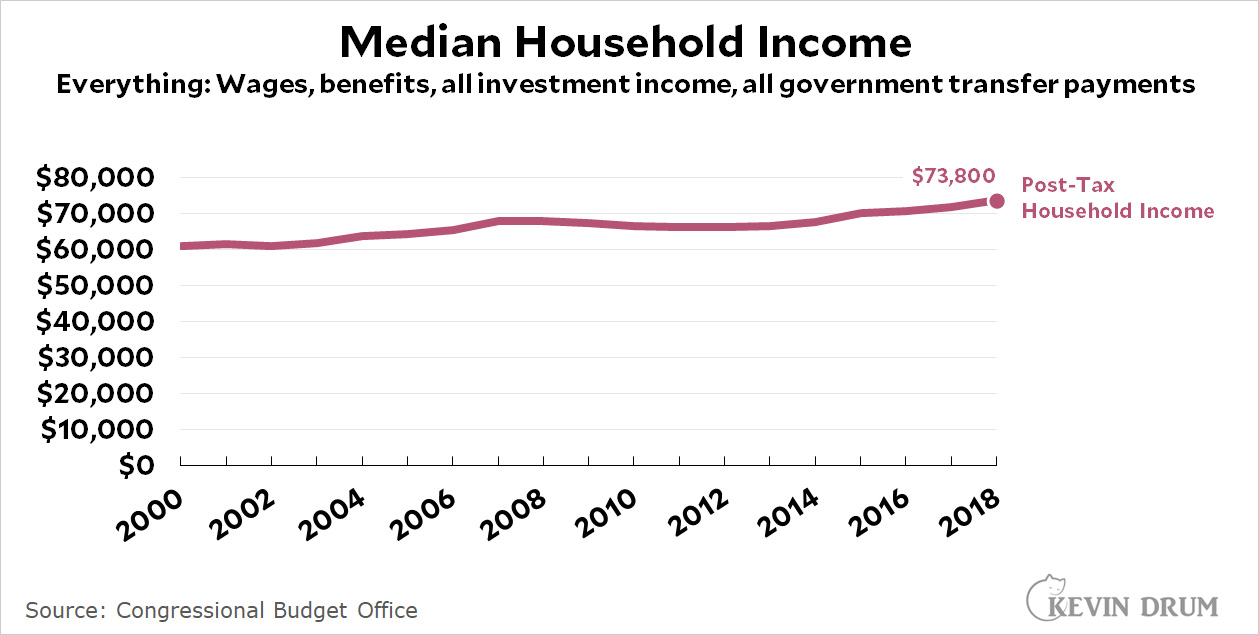

Next up we have an attempt by the Congressional Budget Office to account for everything, including means-tested government benefits and capital gains:

This is a good estimate of honest-to-God total income and taxes, and it's available as a median, so it's not skewed by the rich. Its big drawback is that it's not a regularly updated series. The last report to publish this information is from 2018 and there's no telling when they'll do it again.

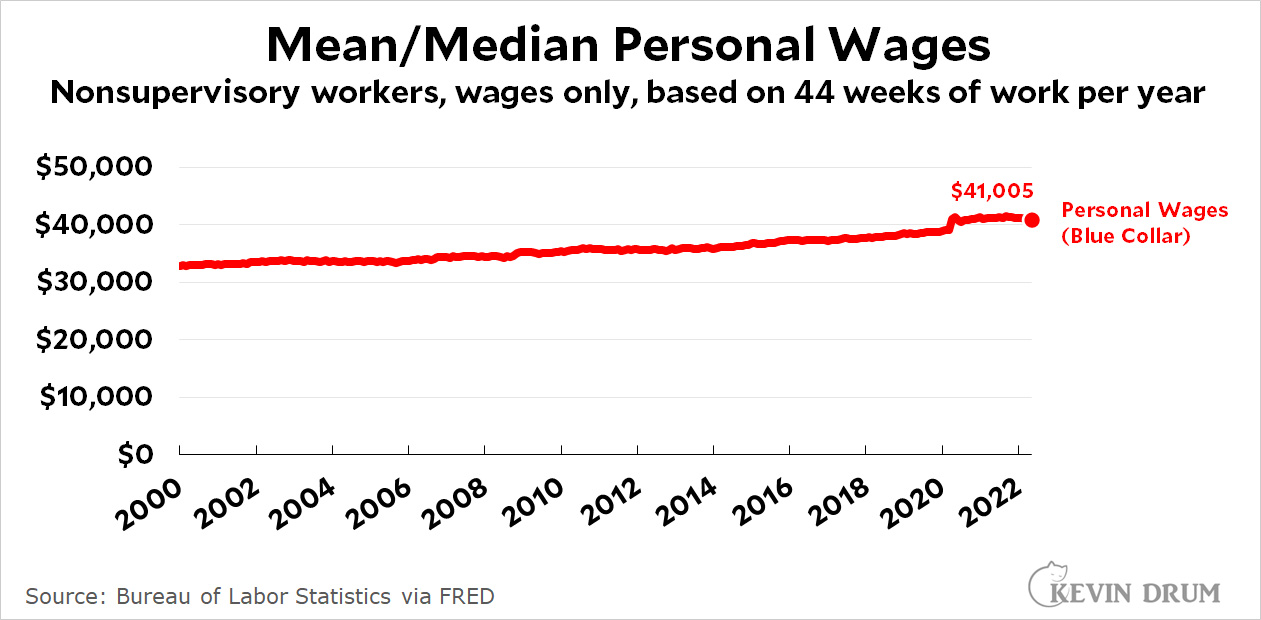

This chart shows wages solely for production and nonsupervisory workers, and it's extracted by multiplying average weekly wages with average weeks worked per year. No managers or CEOs or Elon Musks are in here. Just blue-collar, salt-of-the-earth American workers.

The downside of this series is that it includes only regular cash wages and nothing else. The upside is that it's updated monthly for you impatient types. And while it's technically a mean, the fact that it lops off the top 20% means that it's effectively a median. The meh-side—could be good, could be bad, depending on what you're interested in—is that it measures income solely for the 80% of the country that's nonsupervisory.

And now for the twist: there's really not much difference between all these measures. If you compare the BEA's mean income to the Census Bureau's mean income, they're pretty close. If you compare Census personal income to nonsupervisory personal income, they're pretty close. If you compare Census household income to CBO household income, the difference is noticeable but not huge.

In other words, all of these estimates use a slightly different combination of income and taxes but they mostly wash out at the end. Roughly speaking, I usually stick with simple Census figures. If you want post-tax income, use the BEA figures to figure out tax payments and then subtract them from the Census figures.

NOTE: Some of these figures are available in both nominal and real versions. Some aren't, and you'll have to do the inflation adjustment yourself.

“The near-term inflation outlook had deteriorated since the time of the May meeting,” the minutes said. “Participants were concerned that the May CPI release indicated that inflation pressures had yet to show signs of abating, and a number of them saw it as solidifying the view that inflation would be more persistent than they had previously anticipated.”

This was all because four days earlier the BLS announced that CPI had clocked in at 8.6% in May. This was splashed across front pages everywhere as "the biggest increase since 1981."

But guess what? The media freakout was based on a CPI figure of 8.58% compared to 8.54% two months earlier. Some record. And that was for headline CPI using the non-seasonally adjusted figures. Using the more normal seasonally-adjusted figure, it wasn't a record at all. (March was.) And using the even more relevant core CPI figures, May represented the second month in a row of declining inflation.

And of course that's CPI, which the Fed claims not to care much about. They care about the core PCE rate. At the time of their meeting, the core year-over-year PCE rate had declined since February from 5.3% to 5.2% to 4.9%. And although they didn't know it, a few days later it would decline again to 4.7%.

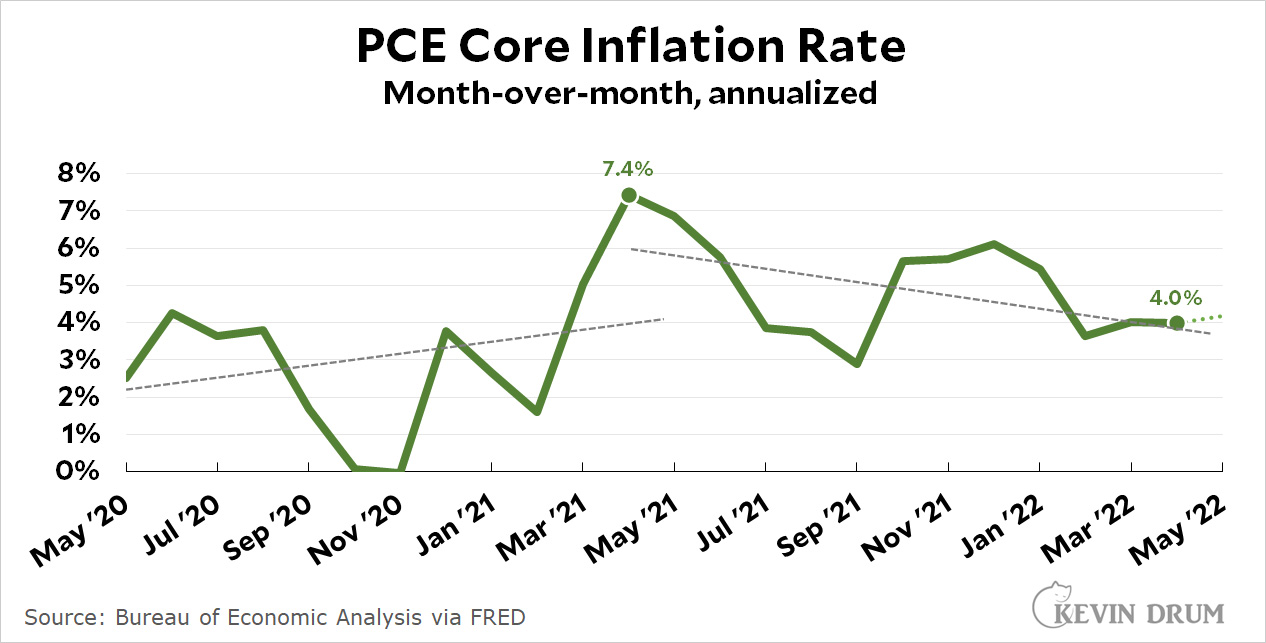

And then there's the momentum of the month-over-month rate, which looked like this:

The April figures were the latest the Fed had available at their meeting, but the trend was clear regardless: since its peak a year ago it had been dropping steadily, going from 7.4% to 4.0%. That's a big and sustained downward movement.¹

You can always find something worrisome if you look hard enough. But there's a whole lot of evidence that inflationary pressures are abating. You have to look pretty hard to find something contradictory—like, say, a single month of headline, non-seasonally-adjusted CPI. The stuff that counts—trends, core inflation, PCE—all show declines.

IANAE and I might be all wet on this. But the evidence sure looks awfully clear to me. Just about every relevant measure is showing some welcome softening in inflation. And looking beyond the core, gasoline is now in its third week of declining prices (down yet another ten cents last week). This leaves food as our biggest remaining problem, but that's largely due to bad crops, war in Ukraine, and natural gas prices causing a big spike last year in fertilizer costs (but which have been softening since March). That will all work itself out eventually, and in the meantime there's nothing the Fed can do to speed it along.

¹When the May result was released it came in at 4.2%. But this is a volatile measurement and a small change in a single month doesn't mean much.

Every year I spend a few days taking pictures of hummingbirds in our garden. Here is our 2022 hummingbird posing in front of a Rose of Sharon. Such a beautiful little creature.

Over in England, there's been a long-running case involving an international development researcher who was let go for tweeting about transgender women. In particular, she repeatedly expressed skepticism that trans women are really women and the tribunal ruled that this was largely the reason her employment contract wasn't renewed.

I had never heard of this case before, but thanks to Twitter I heard about it today because the researcher, Maya Forstater, won her case on appeal to Britain's highest employment tribunal. They ruled that all her tweets were reasonable enough to be protected under current law, and therefore she had been sacked unfairly.¹

I don't especially agree with Forstater's views except possibly in a few narrow ways,² but I don't like to see people fired in response to mobs who are upset that someone feels differently than they do. That's regardless of the specific laws in question, which are harsher toward free speech in Britain than they are here.

I would like to see more people calm down about transgender issues, but there are real concerns at stake on both sides and people routinely write and act passionately about their political views. That's OK—even good—as long as it doesn't veer into active harassment. The court ruled that Forstater's tweets didn't do that, so now it's time to figure out what compensation she deserves. Good.

Short version of the ruling: Say what you want but stay away from deliberate harassment. As long as you do that, you shouldn't be the victim of woke mobs demanding you be fired.

¹Forstater has collected a full set of her tweets here. The appellate tribunal responsible for today's decision ruled unanimously that all of her tweets were "fairly mild" with one exception: a tweet about a Credit Suisse executive who identified as a woman for part of the week. Forstater described him as a “part-time cross dresser.” The panel also absolved her on that one, but the vote was 2-1, not unanimous.

²I'd have to study her beliefs in more detail to know.

This month's report is something of a statistical mirage. The size of the civilian labor force declined by 353,000 and the number of employed people declined by 315,000. Not so good! However, the number of unemployed workers declined by 38,000 while the number of underemployed workers (those who had to settle for part-time jobs) declined by 707,000. Not so bad! Meanwhile, more than half a million people dropped out of the labor force, which is . . . something. I'm not sure.

This month's report is something of a statistical mirage. The size of the civilian labor force declined by 353,000 and the number of employed people declined by 315,000. Not so good! However, the number of unemployed workers declined by 38,000 while the number of underemployed workers (those who had to settle for part-time jobs) declined by 707,000. Not so bad! Meanwhile, more than half a million people dropped out of the labor force, which is . . . something. I'm not sure.